Is this book for real? It smells to me like propaganda — an intentional confusion of historical events, and a load of bad theory, for the purpose of muddying the issue. Did the authors on the cover even write it? We will treat it here as if it is in earnest, but maybe we shouldn’t. The authors come from something like a conservative tradition in economics. Richard Timberlake‘s book Monetary Policy in the United States: An Intellectual and Institutional History (1993) is a reference on this topic, especially for the pre-Fed days. Thomas M. Humphrey wrote a number of interesting books, including The Monetary Approach to the Balance of Payments, Exchange Rates, and World Inflation (1982). He also worked for the Federal Reserve Bank of Richmond for some time, and was the author of a nice paper for the Richmond Fed, “Mercantilists and Classicals: Insights from Doctrinal History,” which I quoted in my first book. I used his “Mercantilists and Classicals” trope extensively in Gold: The Monetary Polaris.

The book is published by the Cato Institute, which a friend of mine long ago called a “Monetarist Hangout.” At the time, I didn’t know what he was talking about. I’ve often thought that much of Monetarism is basically propaganda, and that some of its leading proponents, including Milton Friedman, did not really believe what they said, but were intentionally trying to confuse people. Monetarism is a floating-fiat currency doctrine of macroeconomic manipulation, completely contrary to the Stable Money classical ideals expressed by the gold standard. In other words, Monetarists are Mercantilists, not Classicals.

From the cover, we learn that the authors thought there was “monetary disorder” in the 1930s, arising from the Federal Reserve. Many, many such claims have been made over the years — many different claims, since it seems nobody can agree on exactly what the “disorder” was. Instead, I think that making up new “monetary disorders” basically out of thin air has become a popular career-boosting tool, following the blame-the-Fed model of Milton Friedman long ago. I looked into all the major arguments I could collect, and found nothing to them. Of course there really was monetary disorder during that time, especially the devaluation of the British pound in September 1931, and all the other devaluations (more than twenty) that followed before the end of 1931, including Japan. But, strangely, this is usually the only kind of “disorder” that is not mentioned by these kinds of authors.

October 2, 2016: The Interwar Period, 1914-1944 (contains many links)

August 25, 2017: The Interwar Period #2: It’s Not That Complicated (many more links)

I found that these arguments arose from the theoretic “Price-Interest-Money Box” that economists got themselves into beginning in the late 19th century, in the Marginal Revolution era which mathematized economics. This tended to exclude all forms of economic policy that were not easily quantifiable — taxation and regulation especially — and to concentrate attention on Prices, Interest and Money.

July 10, 2016: The Tyranny of Prices, Interest and Money

November 27, 2016: The Tyranny of Prices, Interest and Money #2: The Old Historicism

Thus, it made sense that, if you were looking for some kind of problem, you would produce some kind of theory involving Prices, Interest or Money. Sometimes there are issues with Prices, with one example being Price Controls. Some have argued that inflexibility of wages, arising from strong unionization, was a major factor of that time, contributing to much higher unemployment. I think this argument is somewhat exaggerated, but there might be something to it. Otherwise, Prices were generally quite flexible, and adjusted downward rather readily. Very high Interest rates would certainly draw attention, but interest rates in those days were low. This leaves Money as the obvious remaining option, if you are stuck in the Price-Interest-Money Box, omitting all other economic factors, as these authors do.

“The trade cycle is a purely monetary phenomenon.”

— economist Ralph Hawtrey, 1922. Italics in the original.

The authors state, with great enthusiasm, that they are card-carrying Monetarists worshipping at the feet of Milton Friedman.

Milton Friedman liked to recall that his experience with the Great Depression as a young man living in New York had a major effect on his decision to study economics. So, we can count at least one good thing that came out of that tragic decade. His and Anna Schwartz’s epic account of the Great Contraction (1929-1933) in their Monetary History tells most of what happened during that unhappy time. Their study is empirical and analytic economics at its best. Those of us who are following in their footsteps have had this superb model of economic research and exposition to guide our further research on that worrisome and, at times, puzzling event. (p. 167)

Neither Friedman’s Monetary History, nor this book, makes any mention of anything that happened outside the doors of the Federal Reserve. The huge trade war that engulfed the world around the passage of the Smoot-Hawley Tariff in 1930? Not a sentence. The explosive increase in taxes in 1932, by Herbert Hoover, which took the top income tax rate from 25% to 63%? Apparently not worth wasting words upon. The devaluation by Britain, and much of the rest of the world, in 1931? Who cares. This is the usual delusion you get with Monetarists. At least Murray Rothbard, in American’s Great Depression, talked about a wide-ranging set of factors, even if he too was stuck in the Austrian-flavored version of the Price-Interest-Money box.

Nope, this is 100% Blame the Fed.

Now, it is OK to look at issues regarding the Federal Reserve exclusively, and set aside all the other things going on the time. You can’t talk about everything all the time. You have to focus. But, the authors make clear that they really are 100% Blaming the Fed.

Had the Fed adhered to this view rather than to the real bills framework, the Great Depression arguably would have been avoided. (p. 60)

But, the authors don’t blame the Gold Standard either.

A dispassionate observer could hardly imagine that a naturally occurring gold money, with a long history of disciplined and orderly acceptance and operation behind it, could suddenly in the few years between 1929 and 1933 have initiated and prolonged a worldwide depression of such magnitude. It simply does not make sense. (p. xvii)

Without question, however, the gold standard was completely innocent of having any responsibility for the Great Contraction. (p. 115)

Even Milton Friedman himself, writing in support of this book, exonerates the gold standard.

It certainly was not adherence to any kind of gold standard that caused the [Great Depression]. If anything, it was the lack of adherence that did. … [Humphrey and Timberlake’s] emphasis of the Real Bills Doctrine complements in an important way Anna [Schwartz] and my analysis of why the Fed was so ‘inept.’ (frontspiece)

About the only thing that you could say about gold itself, as a cause of the Great Depression, is that its value somehow rose dramatically — something unprecedented in the many centuries of the use of gold as money, or a monetary standard. Some people have claimed this, but neither Friedman, nor the authors here, do that.

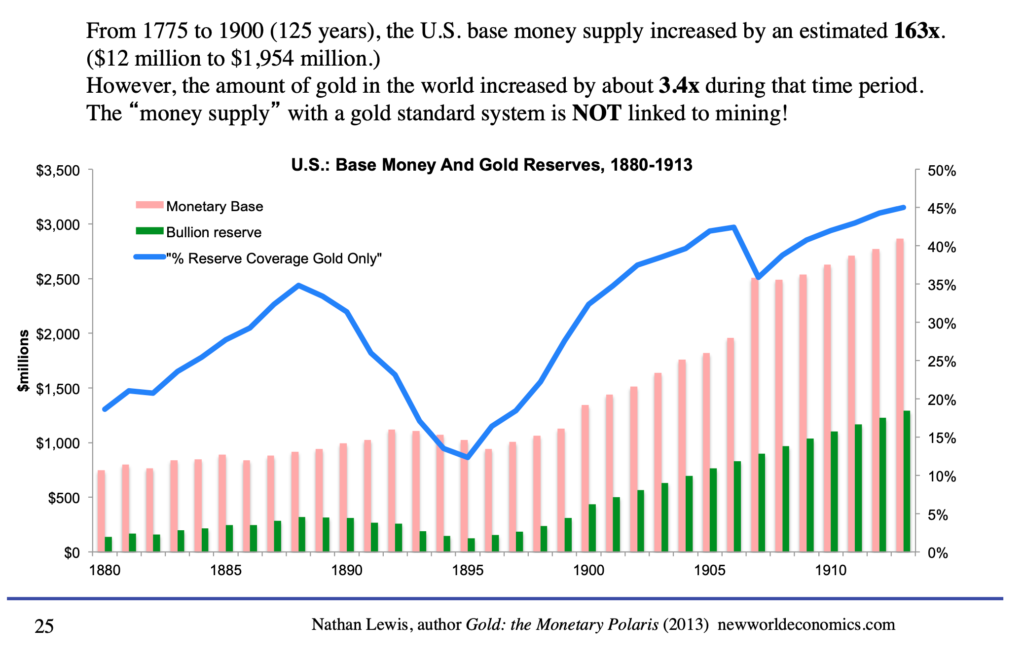

But it is clear that the authors do not have a very good idea of how the gold standard — the monetary policy of the Federal Reserve and most other central banks of the time — worked. They pitch a sort of gold-mining Monetarism. Namely, that it is the stable growth in the quantity of aboveground gold, via mining, that is the key. The roughly 2%-per-year growth of aboveground gold via mining looks a lot like the 4%-per-year increase in base money proposals that Milton Friedman once wanted to make a Constitutional Amendment. This was in a book called A Program For Monetary Stability (1960). In their mind it is the steady increase in supply that creates “monetary stability,” without any reference to the value of the currency. In MV=PT, where is the value of the currency? This is completely dumb, of course, and Bitcoin proved it.

Most understandably, the point of declaring gold (and silver) a necessary base for all money creation was to limit the total amount of common money that banks or governments could create. The gold-silver base was not absolutely fixed; it could grow at the same modest rates as the world’s production of gold and silver. It therefore provided a limited potential for growth in common money to accommodate the growth in real product of the economies that based their monetary systems on it. (p. 120)

March 6, 2014: Bitcoin Proves Friedman’s Big Plan Was A Joke

In a gold standard system, gold provides the “standard of value.” All the money has a fixed value, linked to gold at a specified parity. This does limit money creation, because excess money creation, that leads to a decline in the currency’s value compared to its gold parity, must be curtailed under a gold standard system. But this has nothing to do with mining supply. The quantity of money can vary dramatically, up and down, basically in response to changing demand to hold money. This is a lot like how gold ETFs work, or currency boards today. I went into this in a lot of detail in Gold: The Monetary Polaris (2013).

In 2014, at a presentation that I gave at the Cato Institute, I tried to demolish some of these strange notions. (Obviously, considering that this book was published by Cato five years after that presentation, I was not entirely successful.) I observed that the US base money supply went from about $12 million in coins, to about $1,954 million in coins and banknotes, between 1775 and 1900 — a 163x increase! During this time, the value of the dollar (compared to silver and then gold) was basically unchanged.

February 16, 2014: Event at the Cato Institute

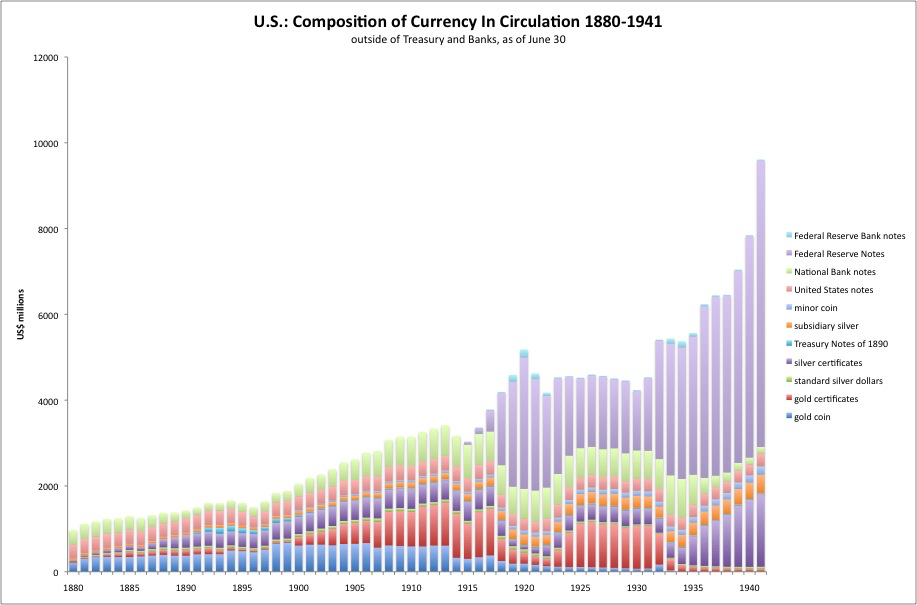

July 15, 2012: Composition of US Currency, 1880-1941

And where did I get these figures?

From Timberlake and Friedman’s books!

I will stop there for now, and continue again soon.