We have been looking at Friedrich Hayek’s monetary writings, compiled by Stephen Kresge in Good Money, in two volumes.

January 13, 2019: Good Money, Part I: The New World, by Friedrich Hayek

February 10, 2019: Good Money Part I #2: Hayek’s Early Enthusiasms

February 16, 2019: Good Money Part I #3: The Depression Years

March 3, 2019: Good Money Part I #4: Nothing To Say About The “Business Cycle” In The Middle Of The Great Depression

March 10, 2019: Good Money Part II: The Standard, by Friedrich Hayek

April 21, 2019: Good Money Part II #2: Currency Choice

Today, we will finish up with two short papers at the end of Part II. The first is “Toward a Free Market Monetary System,” which is actually from 1977, which is before the two papers we looked at last time, which were from 1978. However, it appears that the previous two papers have some prior history; the first appeared as a speech and pamphlet in 1976.

Hayek began with some good points:

Under the Gold Standard, or any other metallic standard, the value of the money is not really derived from gold. The fact is that the necessity of redeeming the money they issue in gold places upon the issuers a discipline which forces them to control the quantity of money in an appropriate manner … (p. 230)

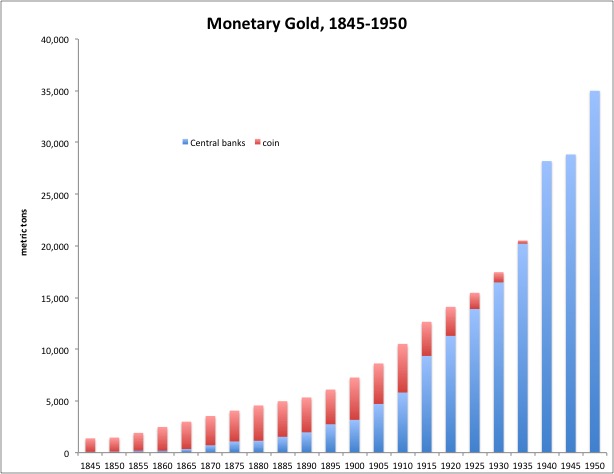

I think this is a valid criticism of the all-too-common “a pile of gold in a vault will magically manage the value of a currency for you” mode of thought, which was unfortunately very common then, and was also (arguably) a chief reason for the failure of the Bretton Woods system in 1971. The U.S. had an enormous amount of gold in its vaults at the beginning of the system, in the late 1940s — roughly 40% of all the aboveground gold in the world — and yet the system blew up in only 27 years. In fact it still had an enormous amount of gold even in 1971; and European central banks had three times as much. While there have always been those who understood these principles properly (Hayek among them; perhaps Edwin Kemmerer before then; people like Steve Hanke today), these have always been few in number, and it seemed that others could not learn from them. The principles did not propagate. This was one motivation for me to write Gold: The Monetary Polaris. Remember, the world monetary system blew up because people didn’t understand this, and currencies (Turkey, Argentina) continue to blow up for this reason today, so it was not a minor matter.

My conviction is that the hope of returning to the kind of gold standard systems which has worked fairly well over a long period is absoutely vain. Even if, by some international treaty, the gold standard were reintroduced, there is not the slightest hope that governments will play the game according to the rules. And the gold standard is not a thing which you can restore by an act of legislation. The gold standard requires a constant observation by government [i.e., central banks or other currency issuers] of certain rules which include an occasional restriction of the total circulation which will cause local or national recession, and no government can nowadays do it when both the public and, I am afraid, all those Keynesian economists who have been trained in the last thirty years, will argue that it is more important to increase the quantity of money than to maintain the gold standard. (p. 231)

These laments certainly apply to 1977. And yet, every gold standard system — he uses the term “gold standard system,” which I also adopted (without Hayek’s influence) in Gold: The Monetary Polaris, to emphasize that it is indeed a system — has been established or at least maintained (that is, allowed to exist unmolested if privately managed, as was usually the case before 1940), by governments. Governments have sustained gold standard systems for many centuries. The Athenian drachma’s value in terms of silver was unchanged for about six centuries. The Byzantine solidus’ gold content was unchanged for over seven centuries. The British pound’s value in silver (and then gold) was unchanged for over 300 years. The Spanish silver dollar’s value in silver was essentially unchanged (there were minor adjustments) from the late 15th century up through the 1930s. So, while the situation in 1977 was perhaps unpromising, nevertheless humans have had some success in these matters.

Hayek did not mention much that all such criticisms which apply to the gold standard must also apply to his pet commodity basket standard, or any other “fixed value” system — with additional complications, such as the inability to hold meaningful “reserves” in commodities, difficulties with providing convertibility, and issues such as the statistical composition of the commodity basket, which could be gamed for political purposes, while gold always maintains an unchanging 79 protons. They also apply to all systems which use a floating fiat international currency as a standard of value, such as the floating dollar or euro, which include over 50% of all currencies today, and a similar portion in 1977 as well.

The last sentence in Hayek’s quote above is informative, as it describes common monetary thinking at that time, and also today. This is the idea that any “restriction” (reduction in base money supply) must cause a recession, or be recessionary. The natural conclusion, if one is to avoid any meaningful reduction in base money “to avoid a recession,” is that base money must continuously grow; and from this we soon come to the conclusion that base money should grow at some modest rate roughly equivalent to the (hoped-for) growth of the economy as a whole. This is, basically, Milton Friedman’s argument from the mid-1960s, which we have earlier described as error and fallacy.

March 6, 2014: Bitcoin Proves Friedman’s Big Plan Was A Joke

It is a trivial exercise to show that indeed base money, under a gold standard system, did indeed have some periods of “restriction,” and that no recession resulted.

June 7, 2015: The Bank of England, 1696-1914

This also applies to any currency-board system today. But we find, since 1919, many examples where central banks, when faced with a crisis (weak currency value vs. parity), refuse to reduce the base money supply, even in the face of large gold outflows. The large gold outflows themselves would have reduced the base money supply (the base money received in conversion is removed from circulation), in the absence of any other action; and this was, in the past, one of the main mechanisms by which gold standard systems were maintained. The same applies today with sales of foreign reserves. So, this lack-of-action does not actually represent negligence, but rather intentional activity to keep base money from contracting (commonly known as “sterilization”), when that is what would have happened automatically due to the gold/foreign exchange sales.

September 4, 2016: What Is “Sterilization”? 2: The Complexity of Central Bank Activity

Even in a crisis situation, a contraction of base money to support the value of a currency will not have a recessionary effect. The contraction of supply corresponds to a reduction in demand; the reduction in demand (“selling”) which is causing the value of the currency to decline. So, we are in effect eliminating “excess” base money. The 20% reduction in Russian ruble base money in 2008 did not cause a recession. Instead, it halted the collapse of the ruble, which was of course a good thing, and was followed by a nice recovery.

October 16, 2014: Russia’s Currency Crisis: This Is So 2008!

However, I think I will add a caveat: the contraction of base money supply to maintain a gold (or other value target) parity will not be recessionary if there is no change in the value of the currency — in other words, if the currency’s value remains at the value parity. Sometimes, a currency will sag quite a bit from the parity; and the process of returning the currency to the parity, which involves a rise in currency value, will be somewhat recessionary. However, against this is matched an end to the crisis atmosphere, which is a good thing; so the actual economic outcome depends on specific conditions. For example, the dollar’s value sank to about $42/oz. in 1968. The process of returning this to $35/oz. in 1970 involved some meaningful rise in dollar value, with some recessionary consequences.

The same applies, naturally, to more serious situations where a currency that has been floating in value for a long time is returned to some gold parity at a higher level, as was the case in Britain in 1925 and the U.S. in 1879. This involved some contraction in base money supply, and also, some recessionary influences. But this too arose because the currency was being pressed higher in value, not because it was being maintained at an unchanging value vs. its parity.

In any case, we have to wonder: why do people insist on maintaining an unchanging or growing base money supply, when the values of their currencies are sagging below what they would like? This outcome cannot be easily explained by simple negligence. I think it is this idea that a reduction in base money supply is inherently recessionary. This line of thinking played a part also in the devaluation of the British pound in 1931.

May 22, 2016: The Devaluation of the British Pound, September 21, 1931

Obviously, it will have to be completely abandoned if we are going to make any progress in these matters. But, countries that use currency boards today have indeed abandoned it, so this is not very hard to do.

Hayek included three (actually, two) interesting examples of currencies that were maintained at a gold parity through direct management of the supply of currency, apparently without gold conversion. These were the silver coinages of Austria and India. After the decline in silver vs. gold in the 1870s, it was decided that the value of the currencies would be based on gold, not silver, although the coins were made of silver. The supply of coinage (and, presumably, other base money) was restricted when their value was below a gold parity, and expanded when it was above; and in this way, an effective gold standard was maintained without gold conversion. The coins became token coins, like coins today, which operate on the principle of banknotes. (Hayek’s final example, Sweden during World War I, did not involve currencies’ value being maintained at a gold parity, or any other parity, but rather floating in value.)

Hayek argued that, if a gold standard were reintroduced, the value (the real value) of gold would certainly go up by a very large degree; and this would make gold unusable as a monetary standard. In an environment of “currency choice” as Hayek imagined:

In the first instance indeed, as you all would expect, people would from their own experience be led to rush for the only thing they know and understand, and start using gold. But this very fact would, after a while make it very doubtful whether gold was for the purpose of money really a good standard. It would turn out to be a very good investment, for the reason that because of the increased demand for gold the value of gold would go up; but that very fact would make it unsuitable for money. (p. 233-234)

Oh really. It is worth noting that at this very same time, and continuing on to the present, people made exactly the opposite argument: that, with the reintroduction of gold standard monetary systems worldwide, the value of gold would decline by a large amount. The rational argument was something like this: during a gold standard era, holding gold in a vault is not very productive. Instead, you could own British consol bonds, or something else, and make some interest return without very much risk. It was only because of the environment of currency unreliability (in the late 1970s, and perhaps today) that people feel the need to hold gold bullion directly. These people point to commodity prices vs. gold, and note that commodity prices seem to have fallen quite a lot vs. gold since 1970. The implication is either that commodity values have fallen; or gold’s value has risen. (I think it is the former; they think the latter.) So, against Hayek’s conviction that so-and-so would definitely happen, we also have quite a few people that say the opposite-of-so-and-so would happen. You might think that Hayek, since his youth convinced that a commodity basket represents a measure of “purchasing power” and consequently “stable value,” would prefer the latter argument. This is what it looks like when people make stuff up out of thin air, and then tell others that it is definitely so. Do you see one single argument — history, statistics, etc. — in support of Hayek’s assertions? We do not. That is what I mean by “making stuff up out of thin air.”

For example, we could say that World War I provided a historical example of virtually the whole world going off the gold standard — and also physically blowing itself up. And yet, the world returned to the gold standard in the 1920s, without any apparent difficulties related to the value of gold going either up or down. Much the same happened again in WWII, and there was again some handwringing that going back on gold would cause this, that, or the other problem; but it was basically fine.

January 29, 2017: The Triumph of Gold (1952), by Charles Rist, #2

It’s worth noting that a return to a gold standard system does not imply widespread use of gold coinage. Gold coinage has a rather high value, typically in excess of $300 of today’s dollars per coin, and would not be used much in transactions. Already by 1930, use of gold coinage worldwide had a pretty big falloff although it remained a regular part of monetary systems worldwide.

In the 1980s, we did not return to a gold standard system, but the dollar’s value was nevertheless stabilized against gold. Again, this worked: the result was the economic boom of the 1980s and 1990s, just as the return to gold in the 1920s also led to an economic boom.

Let’s move on to the last paper (whew!): “The Future Unit of Value,” from 1980. One guess as to what “the future unit of value” is not. Hayek again conflated the idea of “purchasing power” and “stable value” — which the better economists, including Adam Smith, David Ricardo and Ludwig von Mises, explicitly rejected.

Therefore, the basic contention, on which the validity of my further argument rests, is that, if people were wholly free to choose which money they wished to use in their daily transactions, it would soon appear that those did best who preferred a money with a stable purchasing power. This aspect of liquidity which is usually indicated with the term stability of value is normally expressed as an index number of prices. It is often taken for granted that a good money should be approximately constant in purchasing power. That means that it should be approximately constant in terms of its average prices. (p. 242)

Leaving aside commodities for now, we have seen that this assertion is blatantly false in terms of something like the Consumer Price Index, as it is commonly calculated — and which is generally considered a better representative of “purchasing power” and “prices” than a commodity basket. The Consumer Price Index in Japan rose by 70% (5.5% annualized) during the 1960s, while the yen’s value in terms of gold (and also commodities) was unchanged. This rise was basically a result of economic growth, not monetary distortion.

July 20, 2018: This Is Why We Want 5% “Inflation”

The rest of the paper consists of what the world might look like using Hayek’s commodity basket standard. And so we wrap up this little exploration of Hayek’s brain, and I find it a rather odd place, given Hayek’s reputation. Naturally I disagree with his conclusions; but also, I disagree with his methods, which rely upon empty assertion and definition rather than any real argument, which was conspicuously absent, apparently through his whole career. The nice thing about real “currency choice” is that you can indeed let the market decide. I am pretty sure I know which one would win; because it has always been the winner, the Final Standard, over millennia of history. And the reason for that is: it always worked.