The Federal Reserve in the 1920s 2: Interest Rates

November 25, 2012

We have been looking at what the Federal Reserve was doing during the 1920s.

November 18, 2012: The Federal Reserve in the 1920s

Today, we will look at interest rates during the 1920s. Remember, there was a bit of fuss at the beginning of the 1920s, because the dollar had slipped from its gold parity during World War I. This was remedied in the 1919-1921 period. So, that time is a bit anomalous. From 1922 or so, things had been more-or-less normalized.

March 25, 2012: The U.S. Dollar During WWI and the Recession of 1920

Here’s the source of our data:

http://fraser.stlouisfed.org/publication/?pid=38&tid=21

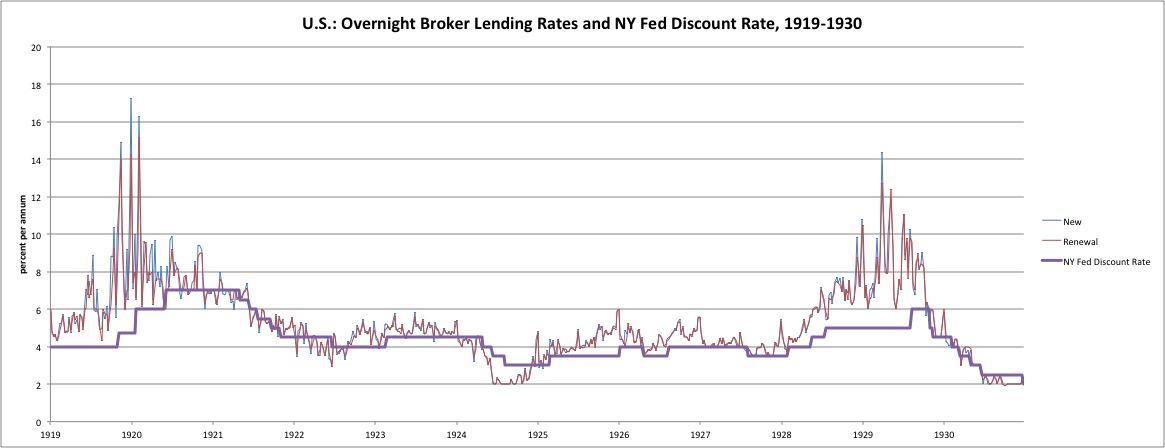

And there it is. What do we see here?

What we today call the “Fed funds rate” is actually the overnight lending rate between financial institutions, in New York. It is the rate at which one bank loans money to another, with a maturity of one day. In practice, this was often rolled over into multiple days, but the lending bank could ask for its money back at any time. Thus, it is also known as “call money.” In those days, commercial banks apparently didn’t borrow much on an overnight basis. They had much larger reserves in those days, more than enough for short-term obligations.

March 13, 2011: Bank Reserves 2: Reserves Out the Wazoo

March 6, 2011: Bank Reserves

Thus, the main borrowers for overnight loans were stock brokers. These loans were made on the floor of the New York Stock Exchange, so they are also known as “Stock Exchange loans.” There was apparently one rate for newly-initiated loans and another for rollovers.

In the midst of this was the Federal Reserve, which also made loans from its discount window. The rate of those loans was the discount rate.

As we can see, the Fed’s discount rate was generally below the overnight rate. This was not really as it was intended when the Federal Reserve was being set up. The idea was that the discount rate would be set well above the prevailing rate. In practice, this might be about 10%. Thus, nobody would borrow from the Fed during normal times. However, if there was a liquidity shortage crisis like 1907, the rate on overnight loans would rise above the discount rate, and the Fed would make loans. These Fed loans would increase the monetary base, thus “adding liquidity” and resolving the liquidity shortage.

However, by the early 1920s, the Fed had already gotten into the habit of being involved in the lending market on a day-to-day basis. During WWI, the Fed had been pressured by the Treasury to keep a lid on short-term and long-term interest rates to allow the Federal government to more easily finance its big wartime deficits. This of course required daily action. The Treasury stopped telling the Fed what to do after the war, but by then the Fed had become accustomed to being regularly involved. Bureaucratic expansion itself would have prevented any migration to the kind of largely dormant institution as the Fed was originally envisioned.

These interest rates are not necessarily comparable. The discount rate was primarily for commercial banks, not brokers. Also, these overnight loans might have had different conditions, such as being uncollateralized, while the Fed’s lending was apparently collateralized.

The Fed’s discount rate was kept at a level that made the Fed competitive with other potential lenders in the market. This was actually quite similar to the regular operating conditions of the Bank of England at the time. The Bank of England was also a private profit-making commercial bank, and thus made loans regularly. The Bank of England was not at all a dormant institution that only leapt into action during a once-a-decade crises. The Bank of England thus also had to keep its discount rate in line with other banks’ lending rates to stay competitive. In practice, the amount of actual loans made by the Fed or Bank of England was somewhat up to the discretion of the bank managers. If their rates were competitive and there was regular demand for borrowing, the Fed or the BoE could decide how much it actually wanted to lend.

Another thing we can see from this graph is that the Fed certainly did not manage the overnight lending rate (“Fed funds rate”) as it does today. That rate is highly volatile. Thus, although there was a Fed discount rate, just as any bank at the time had some official rate that it made loans at for prime borrowers, there was no interest rate target. The Fed was on a gold standard system, and thus interest rates at the short- and long-term ends of the market were left to free market forces.

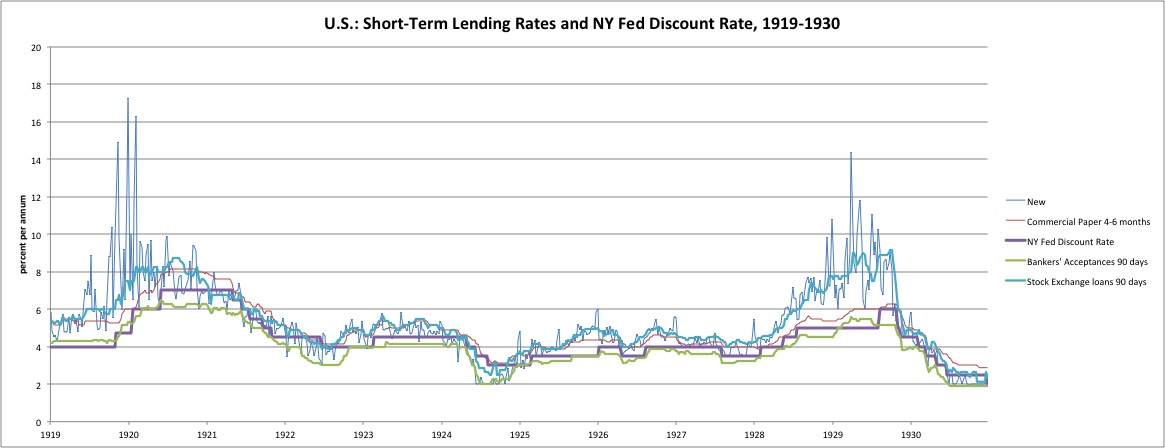

Here’s a little different look at the same thing, which includes more short-term interest rates of the time.

Now we have added Stock Exchange loans with a 90 day maturity, not just overnight lending. Also, we have commercial paper (could include banks) for a 4-6 month maturity, and Bankers’ Acceptances for 90 days. A bankers’ acceptance was a bank’s guarantee on commercial borrowing, apparently used primarily for international trade.

Note that the volatility of the overnight rate is smoothed considerably once we get to a 90 day maturity. Some people might expect that the highly volatile overnight rate — what we now call the Fed funds rate — might translate into increased volatility throughout the lending sphere, as it does today when the Federal Reserve changes its Fed funds rate target. However, this was not the case. Most of the volatility is gone by the time we get to a 90 day maturity. The Fed’s discount rate doesn’t look so low when compared to prime commercial paper with a 4-6 month maturity, which could have included commercial paper issued by banks. (Commercial paper is a short-term corporate bond.) The discount rate represents the Fed’s short-term lending rate, but that doesn’t necessarily mean overnight. Rather, these loans could have been for 90 days or longer, and often were.

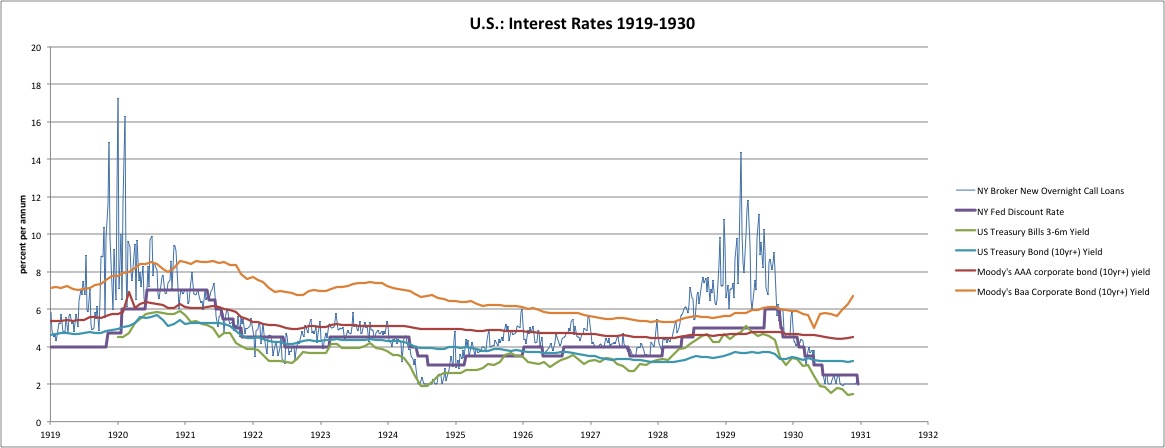

Now we are looking at some longer maturities, including long-term government and corporate yields. The Fed’s discount rate was consistently above the yield on 3-6 month Treasury bills. Note how the volatility of the overnight broker lending rate is completely absent from the long-term (over ten years) Treasury bond yield, which is quite flat around 3.50%-4.00%. (It was a little higher pre-1922.) This describes the general character of market yields with a gold standard system: quite a lot of volatility on the overnight rate, and very stable as maturities increase. This is the opposite of today, when the Fed’s interest rate target means that the overnight rate is very stable, but there is a lot more volatility on the long end, which is the part that counts for most commerce.

All in all, what I see here is a rather nice example of what the lending market looks like with a gold standard system, when the Federal Reserve is not actively managing interest rates. The Federal Reserve at this time was doing much what the Bank of England did throughout the 19th century, the era of the so-called “Classical Gold Standard,” and what the Bank of England did again after the gold standard was renewed in Britain in 1925. However, the Bank of England’s example included regular activity in the lending market via the discount rate. The Federal Reserve was not intended to be this active, but rather an institution that was mostly dormant — thus resolving the conflict and complications that had been an issue with the Bank of England since its inception. There are actually a number of functions that the Bank of England was serving: as an issuer of currency, as a “lender of last resort” to resolve short-term liquidity needs, as a central clearinghouse for interbank payments, and as a regular, profit-making commercial bank. The fact that all of these roles were somewhat intermingled in the Bank of England’s operations made the whole thing very complicated for outsiders — which was not, perhaps, against the BoE’s interests. The British government themselves tried to sort this out in 1844 by separating the Bank of England’s activities into an Issue Department (to take care of the currency) and a Banking Department that would operate as a regular commercial bank. This didn’t work out quite as well as hoped, because the Issue Department only handled the paper banknotes themselves, not the deposits at the central bank (“bank reserves”) which are also a component of base money, and which was handled by the Banking Department. Thus, the total pound base money supply was divided between two departments. Complicated. The fact that hardly anyone can make head or tail of how this system is supposed to operate is one reason — a major reason — why people don’t really understand how to manage a gold standard system today.

January 29, 2012: Gold Standard Technical Operating Discussions 3: Automaticity Vs. Discretion

January 15, 2012: Gold Standard Technical Operating Discussions 2: More Variations

January 8, 2012: Some Gold Standand Technical Operating Discussions

However, it still worked. The Federal Reserve, it appears to me, was just doing what everyone else in the world was doing at the time, and what they had done in the pre-1914 era as well.