(Note: This was originally written as a Forbes.com item, but it soon got too big for that venue.)

The idea behind a gold standard system is to produce a currency that is perfectly stable in value. Alas, perfection is not really possible in these matters, so we have to strive for as little imperfection as possible. If gold was perceived as being insufficient for this task, and if some better alternative existed, we should expect those who sought the perfect ideal of stability of value to then pursue some other alternative. They never did.

The idea behind floating fiat currencies is completely different. Obviously, floating fiat currencies vary in value, from first principles. Stability of value is not a goal at all. Rather, the goal is to be able to manipulate the currency to produce some other desired outcome. The proximate cause of the implosion of the Bretton Woods world gold standard system, in 1971, was that president Richard Nixon wanted an economic boom that would result in his re-election in 1972. He was successful.

Since “chaotic instability of value” is a hard sell, the Funny Money promoters sometimes like to say that they are pursuing “macroeconomic stability,” which in practical terms might mean the avoidance of recessions. To do so, they perturb the currency as much as they think is necessary to achieve their goals. (They usually fail anyway. Even if they succeed, they often create distortions that lead to the next round of problems.)

Thus, it should be regarded as rather strange, and an example of the Age of Ignorance in which we live today, that the gold standard system should be described as one in which the currency is unstable in value, and that today’s floating fiat currency system — in which everyone is aware that currency values fluctuate unpredictably every day, on the foreign exchange market — is an example of stability!

We looked at one of these supposed episodes of gold-standard instability already – the 1890s – and didn’t find anything very horrible. It was in fact one of the United States’ most prosperous eras. Another supposed horror story that the Keynesian floating fiat promoters like to trot out is some kind of explosion of “inflation” after some major gold discoveries in the 1850s. This “inflation” would be the result of a decline in the real value of gold, due to increased supply.

November 21, 2015: Let’s Resolve the Gold Standard “Deflation” Fallacy

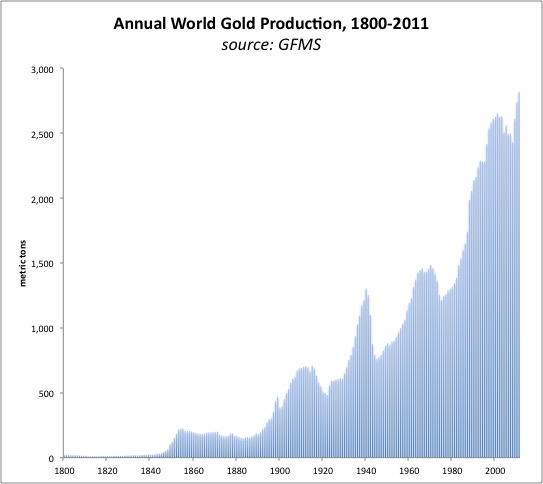

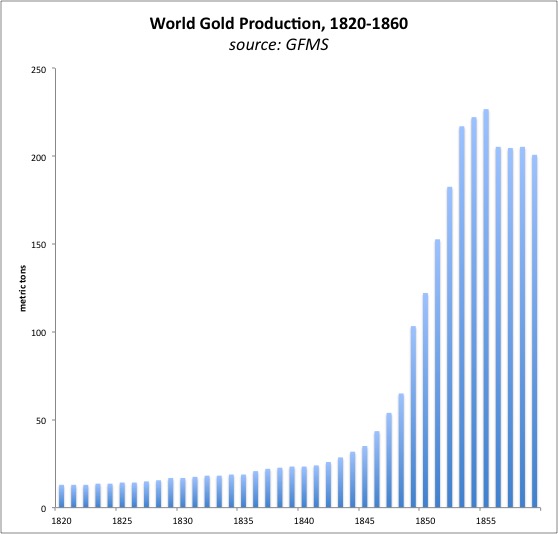

Mining discoveries and development indeed led to a major increase in world gold production. Estimated world production of gold was 17 metric tons in 1830. Some minor discoveries in Russia and elsewhere brought this to 23 tons in 1840, and 54 tons in 1847 – already a big increase. However, the California gold rush, beginning in January 1848, caused a huge expansion in world production. In 1855, world gold production made a minor peak at an estimated at 227 tons, a tenfold expansion from 1840. (Gold production today is about 2,700 tons per year.)

That is a pretty big jump. No doubt about it. If there was ever going to be any kind of major change in gold’s value due to mining supply, this would cause it.

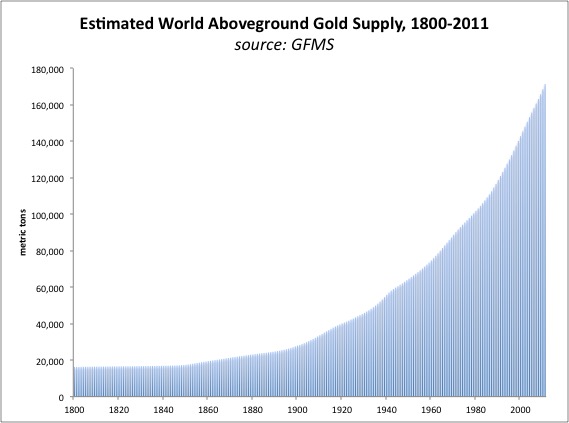

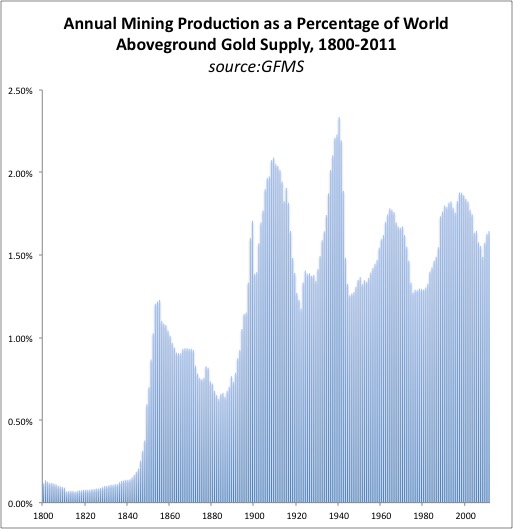

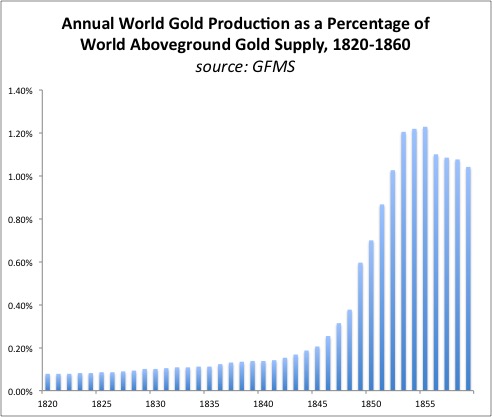

And yet, despite these big numbers, we have to remember that gold is never really “consumed,” but mostly just accumulates over time in the form of bullion, coinage, and jewelry. That 227 tons of production in 1855 was just 1.23% of the estimated 18,461 tons of aboveground gold extant at that time, the accumulation of all mining activity back to the beginnings of human history. Thus, the “supply” of gold hardly changed at all. It went up 1.23% — actually a little less than the 1.40% average production/aboveground supply ratio during the 1850-2011 period.

These estimates of production and aboveground supply come from GFMS, a specialist in precious metals statistics and analysis that is now part of Thompson/Reuters. They differ from some estimates that I used earlier, which I calculated myself based on data from Roy Jastram’s book The Golden Constant (1977). They also differ from some estimates made by James Turk. The primary difference is the amount of gold existing in the world before 1500 AD. The result of a higher estimate of aboveground gold pre-1500 is that production estimates for the 19th century look lower, as a percentage of aboveground gold, than would be the case if the pre-1500 estimates are lower. It doesn’t make much difference for the 20th century, since production post-1850 by then swamps out differences in pre-1800 production. James Turk and Juan Castaneda did an extensive investigation into the aboveground gold stock in 2012, available here:

https://www.goldmoney.com/images/media/Files/Old_GM_WP/theabovegroundgoldstock.pdf

Turk and Castaneda have dramatically different conclusions to GFMS regarding pre-1500 aboveground gold supplies, and explain their reasoning. I personally tend toward a higher number. In The Ages of Gold, Timothy Green estimates Egyptian gold mining production of between 1,000kg and 2,000kg (1.0 and 2.0 metric tons) per year, in the 15th century B.C. Egypt mined gold since the fourth millennium B.C. Between 3000 BC and 1500 AD is 4500 years of gold mining history, including of course the Aztecs and Incas, Indians, Europeans, and many others.

Since mining production was not really so large compared to the aboveground gold stock, we should not be very surprised to find that the apparent “value” of gold didn’t change much at all.

Unfortunately, there is no perfect yardstick of monetary value that we can use to measure gold’s value. If there was, then the Stable Money advocates would simply use that measure, rather than gold, as the basis for their currencies. But, we can begin to get an idea of what was going on by looking at commodity prices during that time.

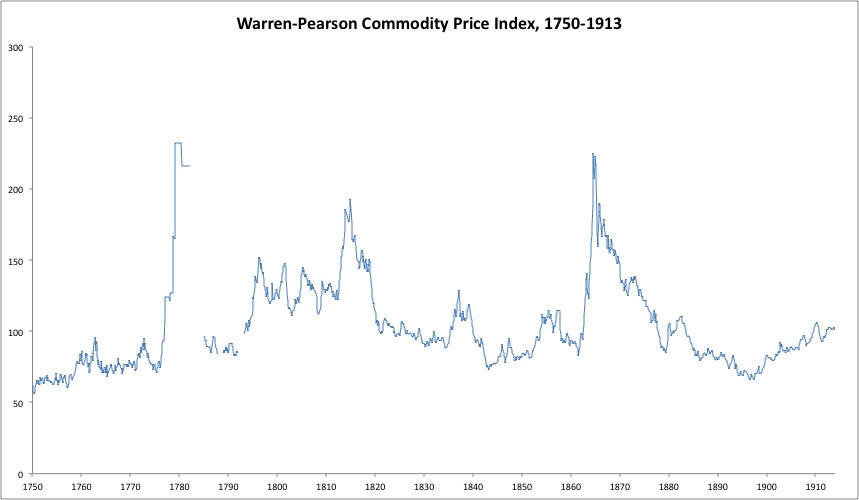

The Warren Pearson index was developed in the early 1930s. It consists mostly of the prices of agricultural products in New York City (not nationwide). Thus, it is similar to today’s CRB spot commodity index – and not at all similar to today’s consumer price index, or CPI.

For now we will use just the WPI until 1913. This is a nominal price index, and reflects the devaluation of the dollar during the Civil War (and Revolutionary War), and also the subsequent rise in dollar value back to the prewar parity in 1879. Most of the big moves in this index are directly attributable to wars, particularly the Revolutionary War, the Napoleonic Wars 1795-1815, the War of 1812, and the Civil War.

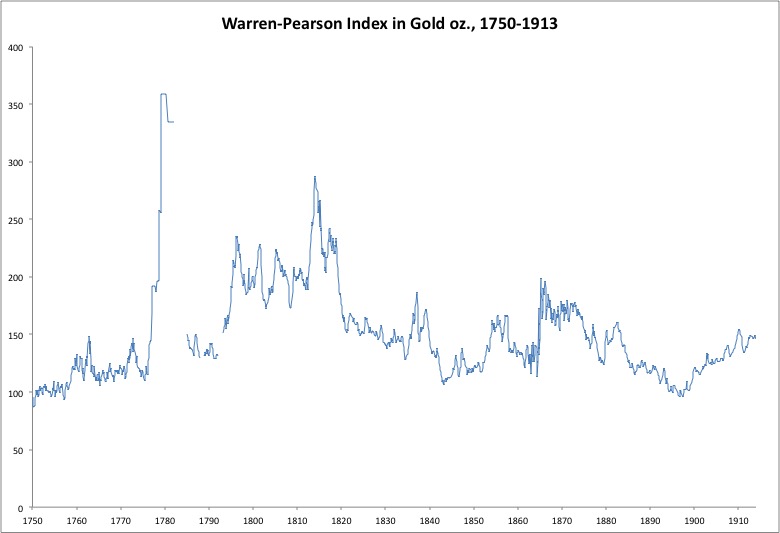

Adjusting for the devaluation and then rise of the dollar 1860-1879, the WPI in terms of ounces of gold looks like this:

No adjustment is made for the Revolutionary War or the War of 1812, however.

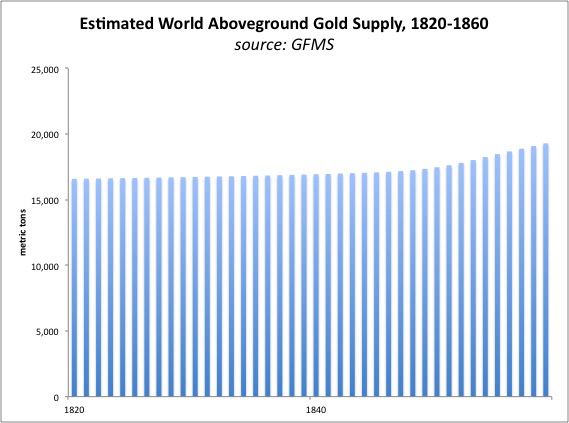

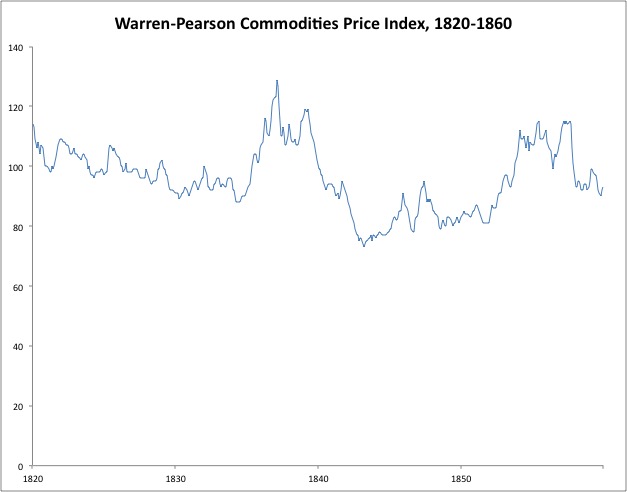

Focusing just on the 1820-1860 period, we have this:

What do we see? There was a little lift in commodity prices after 1850 – meaningful to farmers I am sure, but hardly some kind of inflationary catastrophe. However, there was also a little decline afterwards, such that the index ends at roughly the same level it was at in 1830. Commodity prices were generally depressed in the 1840s, even though gold production had tripled from its 1830 level even before the California gold rush.

Actually, not much happened at all – nothing that couldn’t be just as easily explained as variation in the supply and demand for commodities, rather than some change in the value of money. The rise and decline of commodity prices in the late 1930s was more dramatic, even though gold production was rather flat. There doesn’t seem to be any correlation to gold production at all. This is a picture of stability, not of some kind of gold “supply shock” that sent economies into convulsions.

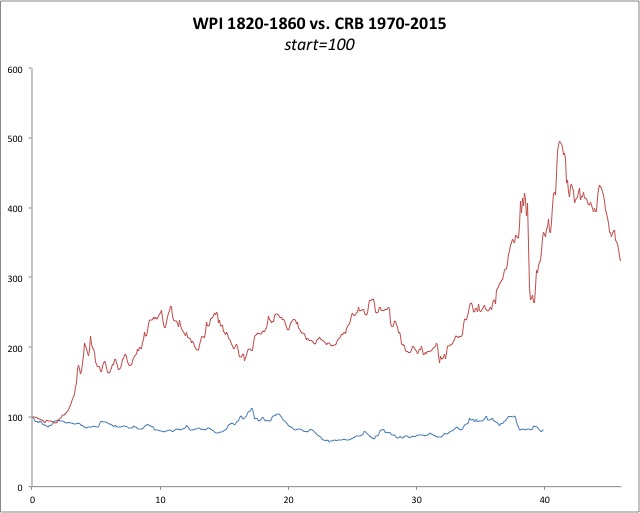

Now, the funny thing is, the people who complain about this non-event the most are the academic Keynesians who are all funny-money fans. They embrace a currency that is unstable in value, from first principles. Not surprisingly, a currency that is unstable in value also results in considerably more commodity price volatility. Here is a look at the Warren-Pearson Index from 1820-1860, a forty-year period, compared to the CRB Spot Commodities Index, a similar index, for 1970-2015, a forty-five year period. They are scaled so that the starting value for each set is 100.

Obviously, there was a lot more volatility during the floating fiat currency era post-1971 than during the gold standard era of 1820-1860, even despite the big mining boom. Statistically, the standard deviation for rolling 12-month periods was 8.18% during the 1820-1860 period, and 14.81% during the 1970-2015 period. But, that only describes a little of the story. The bigger story is that, during the gold standard era, commodity prices tended to fluctuate in the shorter term, but had a strong central tendency in the longer term. During the floating fiat era, prices have had a long-term tendency to rise, which is of course the mirror of the long-term tendency of fiat currency value to fall.

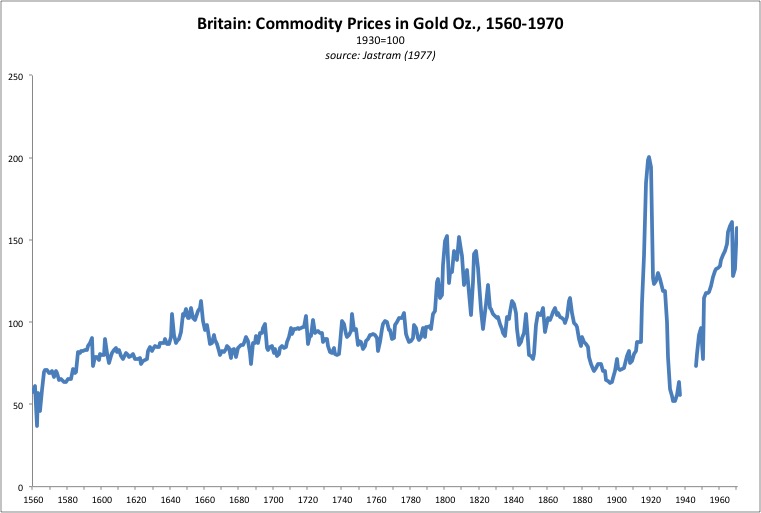

This is a chart of commodity prices in Britain from 1560 to 1970, compared to ounces of gold. There was a similar pattern of a decline of prices into the 1840s, and a rise after 1850. But, it is rather minor, and typical of commodity price variation during this entire period. Commodity prices are supposed to fluctuate, due to changes in the supply and demand for commodities, even while the value of gold (and currencies tied to gold) is stable. It is hard for me to find any great evidence of a significant change in gold’s value due to the mining boom of the 1850s. If there was such a change, as one would expect, its magnitude appears to have been small enough that it would have caused no particular consequences for economies as a whole.