(This item originally appeared at Forbes.com on August 8, 2019.)

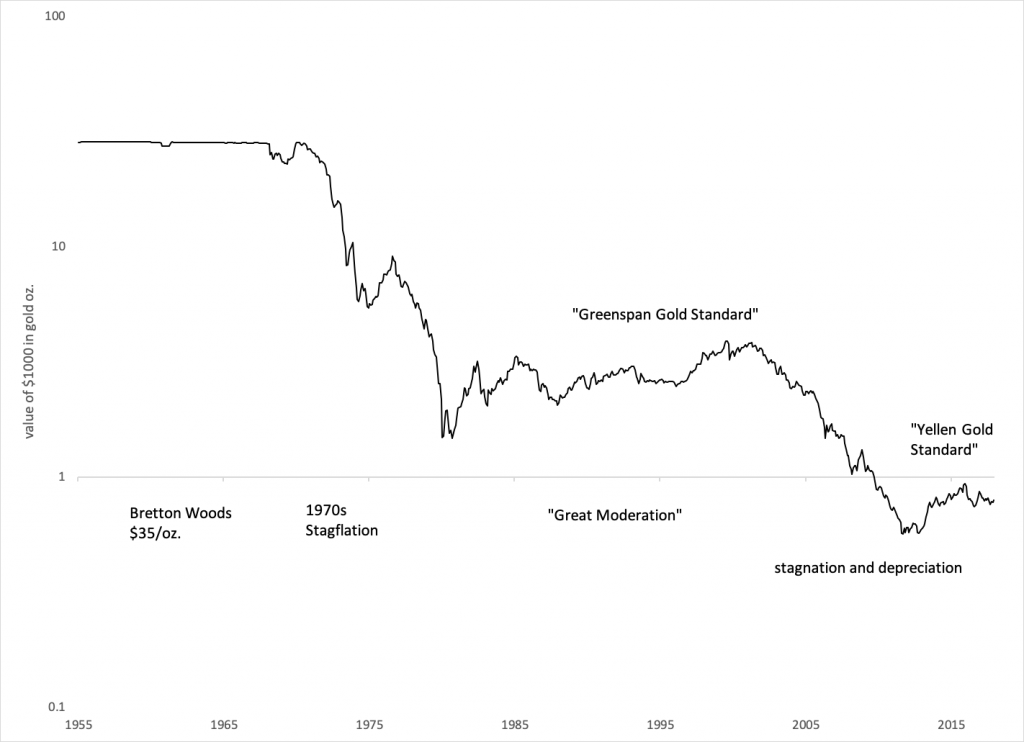

Humans have centuries of experience with basing their money on gold — a “gold standard system.” The last two decades of the gold standard era, the Bretton Woods period of the 1950s and 1960s when the dollar was linked to gold at $35/oz., were the best two decades worldwide since the Classical Gold Standard ended in 1914. Nevertheless, people ask whether gold could still serve the role today that it served for centuries previous, as a standard of monetary value that produces favorable outcomes.

Actually, much of the time since 1971 has also been guided by gold. In 1982, Federal Reserve Chairman Paul Volcker formally abandoned the “Monetarist experiment,” and adopted a loose and ad-hoc method that nevertheless aimed to stabilize the dollar’s value vs. gold and other commodities, taming the wild swings of the 1970s and early 1980s. He was helped in this by the other governments of the world, who got together at the Plaza Accord in 1985 to deal with a dollar that was too strong (it was $300/oz. at the time), and again at the Louvre Accord in 1987 to deal with a dollar that was too weak ($400/oz. at the time). The whole world was guiding the dollar into a rough band around $350/oz.

This process was refined by Federal Reserve Chairman Alan Greenspan, who succeeded Volcker in 1987. During his tenure, the dollar’s value vs. gold stabilized still further. Greenspan, a gold standard advocate in his youth, said later many times that this was intentional. In 2004 he said:

[The] most effective central banks in this fiat money period tend to be successful largely because we tend to replicate which would have probably occurred under a commodity standard in general.

This “Greenspan gold standard” was followed by a long period in which the dollar’s value vs. gold fell from its $350/oz. band in the 1980s and 1990s to a nadir of about $1900/oz. in 2011. Along the way, the price of oil went from $20/barrel to a range of $50 to $140. Oil producers today can’t justify new investment with oil prices below $80/barrel. Gold mining companies which were profitable at $350/oz. in the 1990s find today that they can’t make a buck unless gold prices are above $1200. Whatever the official CPI says, the input costs to oil and gold extraction have risen dramatically. It appears that the dollar really did lose that much value.

I think that, around 2011-2013, people in Washington and elsewhere panicked — just as they did in 1979, which gave Paul Volcker the political support to put an end to the rampant dollar depreciation of the 1970s (at first using a Monetarist framework). The outcome of this was a period in 2013-2019 when the dollar was quite stable vs. gold, which I call the “Yellen gold standard” period. The dollar’s value vs. gold remained in a band between about $1350/oz. and $1150/oz., with a midpoint around $1250. In 2015, as the dollar rose to $1050/oz., a wide variety of indicators showed that the dollar was too strong — much as happened in 1985. the Fed backed off and the dollar fell. Once again, the world was feeling its way to a new gold parity.

In the last few weeks, the dollar’s value has fallen outside the $1350/oz. floor of the “Yellen gold standard” period, and touched $1500/oz. Just as the “Greenspan gold standard” eventually came to an end, and was followed by a period of dramatic dollar decline vs. gold, so too the “Yellen gold standard” has perhaps seen its last.

Let us now look back on that period. It was short — only about six years — but that was also about as long as the recreation of the world gold standard in the 1920s, which also lasted about six years, roughly from 1925 to 1931.

The purpose of a “gold standard system” is to maintain a currency of stable value; or, as I like to term it, Stable Value. When a currency rises too much, problems arise (1985, 2015). When it falls too much, other problems arise (1979, 1987, 2011). A gold standard system relies on the natural stability of gold to avoid both of these outcomes; outcomes which, without the guidance of gold, it seems that we run into time and time again. It worked so well for Greenspan that people called him “The Maestro” and gave him a knighthood.

I think we can say that, during the “Yellen gold standard” period, we did not have strong evidence of a currency that was either rising too much in value (which we brushed with in 2015), or falling too much in value, producing “inflationary” tendencies, which were nowhere to be seen during that time. Once again, whether by intention or whether only by accident and coincidence, a dollar that was stable vs. gold seemed to produce “Stable Money” in an absolute sense, avoiding the problems of either “monetary inflation” or “monetary deflation.” The principle of a gold standard system still works, just as it worked in 1965 and 1995.

I have to add some caveats. Actually, a lot of caveats. During this period, central banks engaged in all kinds of interventionist activity, from zero-percent interest rates to negative yields on long-term debt, to actively participating in equity markets. I want to limit our attention here only to the value of currencies — whether they were too high (“deflationary”), too low (“inflationary”), or, as Goldilocks preferred, “just right.” It was hardly the soundness and stability that proper gold standard systems provided throughout history, but I think we have to conclude that, by this measure, things were tolerably good.

Many people have argued that gold/dollar markets themselves came under considerable official influence during this period. The “stability” of the dollar vs. gold was somewhat artificially engineered. I generally agree with this opinion. But, that was arguably true also during the “London Gold Pool” era of the 1960s, or the 1990s under Greenspan. As I described in detail in Gold: The Monetary Polaris (2013), a proper gold standard system has no need for this kind of intervention and coercion. But, even with all this, the basic principle of a dollar stable vs. gold seems to have worked.

It is popular to argue that a gold standard system is “unfeasible” today, which is a rather odd assertion considering that we have been 80% of the way there for the last several years. We could today, with little effort, formalize this informal system with a hard fix at $1250/oz., using the currency-board-like techniques that I described in Gold: The Monetary Polaris. Actually, more than half of all currencies today use some kind of hard fix of this sort, typically against an international currency like the dollar or euro. The best ones use a currency board. A gold standard system is, in essence, a “currency board linked to gold.” I think that China and Russia are ready to go on that. Europe would follow soon after. We could just get together and shake hands — “The Mar-A-Lago Agreement” — and the world gold standard would once again be recreated, with little more effort than the desire to do so, and the knowledge of how to do it.

But, perhaps we are not quite ready for that. The pattern since 1971 has been: either we have maintained a crude and informal stability against gold (the Volcker/Greenspan period, and the “Yellen gold standard”), or the value of the dollar has fallen by considerable amounts vs gold (1970s, 2000s). When the “PhD Standard” is untempered by gold, it tends to lead to a decline in currency value. The dollar’s value today vs. gold is less than one-thirtieth of its value during Bretton Woods. Very rarely was there any official policy of inflationism or currency depreciation. Usually, the official policy was the opposite. It just worked out that way.

“The world is moving toward a floating regime” the economist Robert Mundell said in 1969. “The experience will be so painful that by 1980 it will begin moving back to fixity.” I would just change the dates. Another period of dollar decline, accompanied by all the various market interventionism common today and perhaps leading even to “modern monetary theory” as a way to finance deficits, won’t be much fun. It would produce — just as it produced in 1979 and 2011 — the urge to produce Stable Money once again. When that time comes, when the political support for Stable Money again forms, let’s not fool around with temporary half-measures, but instead recreate a proper worldwide gold standard system, a modernized and updated version of the pre-1914 Classical Gold Standard system, appropriate for our times just as that was appropriate for theirs.