We’re continuing our look at some of the things that have been said about the 1920s and 1930s, particularly regarding monetary affairs.

February 7, 2016: Blame Benjamin Strong 2: So Obvious It’s Hard To Believe

January 31, 2016: Blame Benjamin Strong

December 13, 2015: Money and Credit 2: Credit

November 8, 2015: Money and Credit #1: Money

So much of today’s conventional wisdom derives from what I would consider mistaken interpretations of that time. A major source of this confusion, it seems to me, is the tendency to mix together “money” and “credit” into one bewildering stew. This actually dates back into the late 19th century.

An easy way to think of it is this: imagine if all monetary transactions took place with gold and silver coins. This includes direct payment in coinage, and also interbank clearing. So, you would still be able to “pay” with a check, credit card, wire transfer etc., but the interbank clearing would be done solely with coinage or, perhaps, bullion.

In this case, it should be obvious that credit has nothing to do with the money. The money is gold and silver, and no banking activity has any effect on it. Banks do not “create money.” Only the mint creates money. If you extend this to banknotes and base money (deposits in a central bank clearinghouse), also linked to gold, the situation does not really change much.

Thus, “credit contraction” is a totally different phenomenon than an undersupply of currency leading to a rise in currency value. However, I think that “credit contraction” can be a very serious event. If bank credit (and all credit including bonds) contracts, what happens? Basically two things can happen: one is that borrowers default. This makes the loan disappear, or at least results in a markdown and writeoff of some sort. Obviously, a default indicates distress of the borrower, and also a “shortage of money” to make the required payment.

The other possibility is that borrowers pay down the balance of the loan. This means that a lot of cash is used to make the payment, which means that the cash cannot be used to spend on other things, whether consumption or investment. People short of cash might want to liquidate assets, possibly driving down asset prices. Obviously, this also includes a “contraction of money”, namely the bank deposits used in payment. Some borrowers might be able to refinance a bank loan with something like a bond issuance, but usually when banks are retreating, it is equally difficult (if not more so) to issue bonds. And, of course, this option is not available to all.

So, you can see how we can get a conclusion of a “shortage of money” when banks ask for their loans to be paid back. This has nothing to do with the medium of exchange, the currency. There is no shortage of actual currency. Much of this talk of “deflation” has focused on banks’ liabilities (deposits), but it is primarily a reflection of banks’ assets (loans), it seems to me.

People were accused of “hoarding” instead of “spending” during the Great Depression, and indeed a reduction in debt constitutes net “savings,” in other words, a higher savings rate. However, it looks to me that much of this was basically paying off debt, which doesn’t create a “hoard” of any sort. Since “hoarding” (i.e. “saving”) in those days mostly meant either banknotes in a coffee can or a bank deposit, or perhaps a gold coin, it appears that there wasn’t much “hoarding” going on since deposits fell dramatically, while banknotes and gold coins were both mostly unchanged.

We would naturally expect to see a contraction in total bank liabilities when we see a contraction in assets, and vice versa. They must naturally be in balance, as they are the two sides of banks’ balance sheets, except for the portion of shareholders’ equity, which could be expected to be roughly stable. Banks in those days funded themselves almost entirely with deposits, just as is the case today except for the largest money-center banks.

Let’s just look at some statistics for the 1920-1940 period.

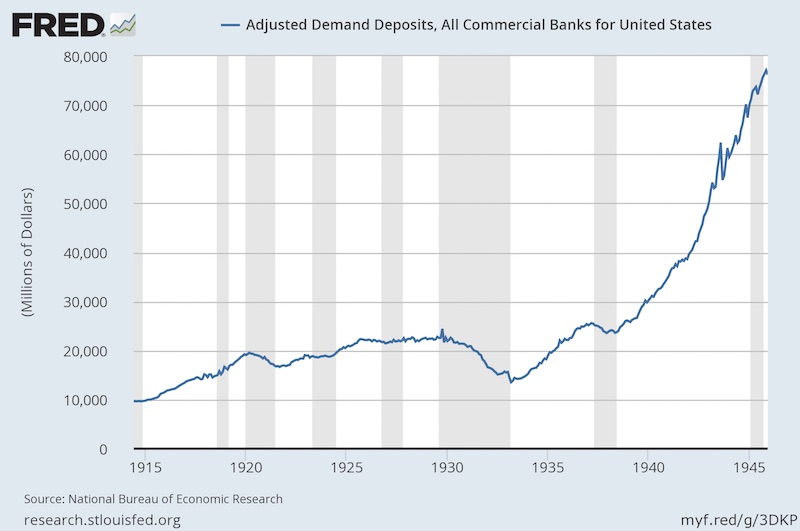

Demand deposits for all U.S. banks.

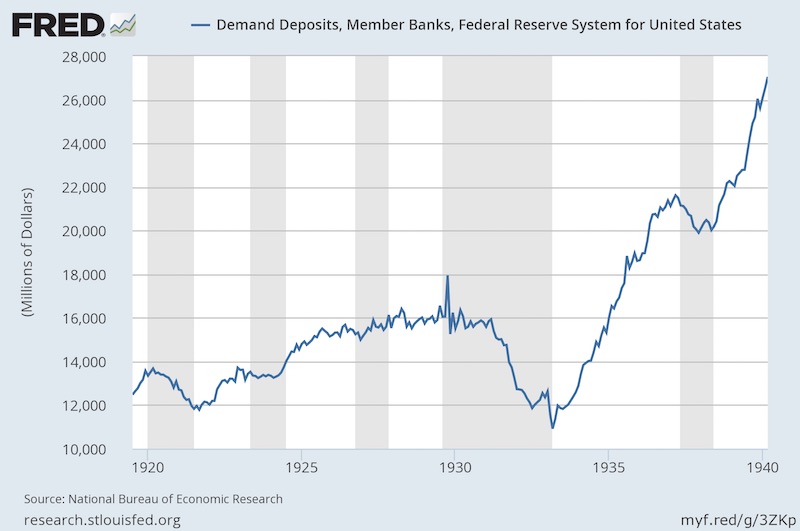

Demand deposits of Federal Reserve member banks. The “all” figure is about $22 billion in the late 1920s, while this is about $16 billion — obviously, leaving about $6 billion of demand deposits at non-member banks.

Demand deposits include both “checking” and “savings” accounts. Obviously, savings accounts are not checkable, and can’t be used as a payment device.

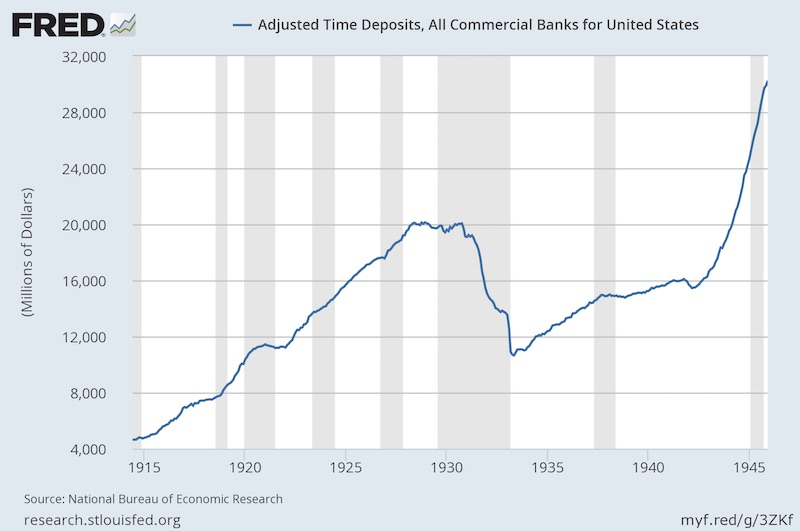

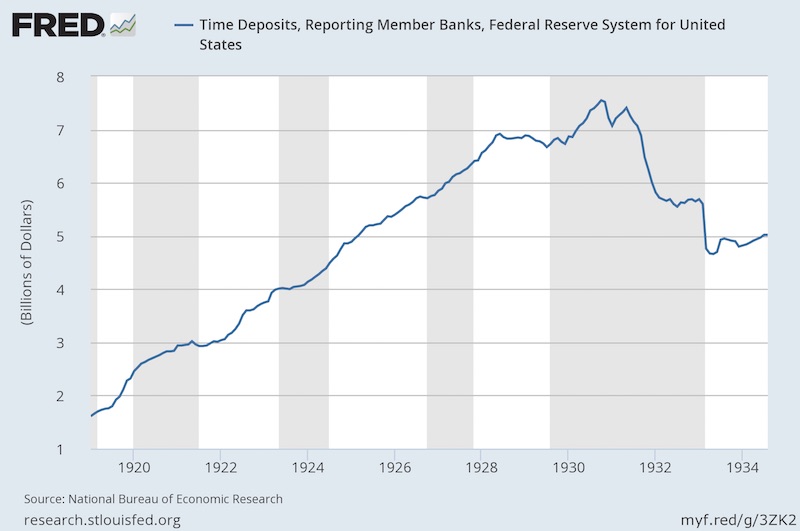

Time deposits. Roughly the same quantity (here $20 billion) as demand deposits.

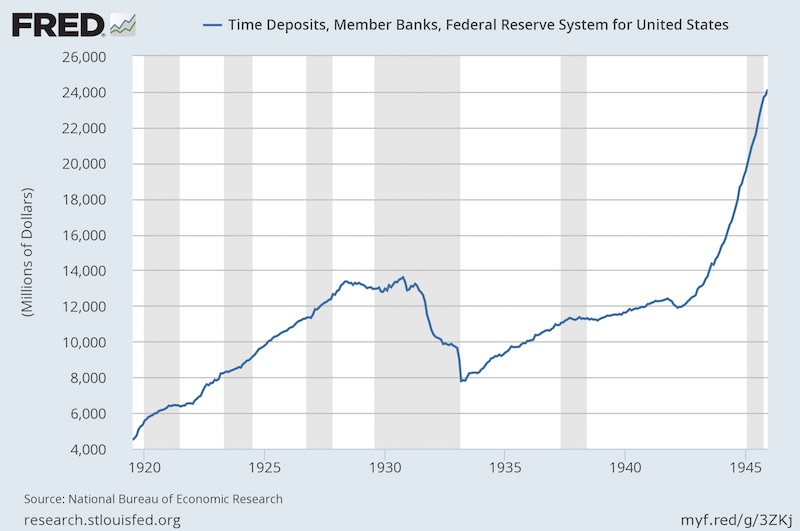

Again, time deposits at member banks are proportionately lower.

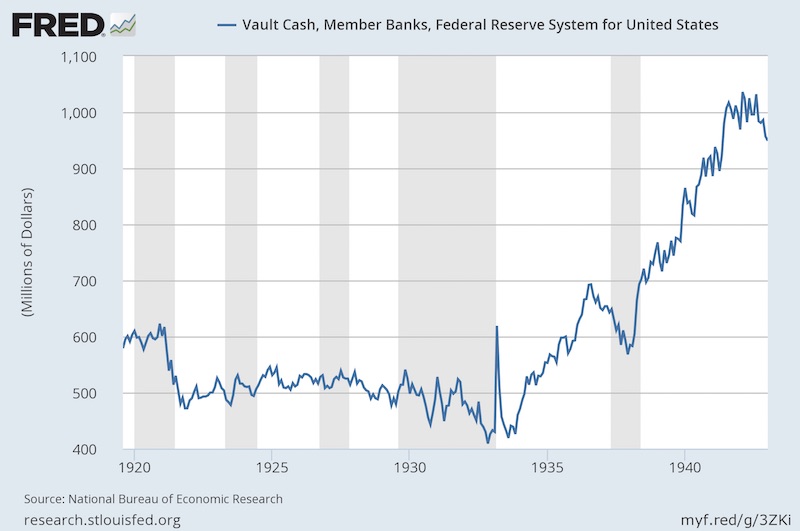

Vault cash of member banks that report weekly.

“Reporting” banks are a smaller subset of banks that reported their condition weekly.

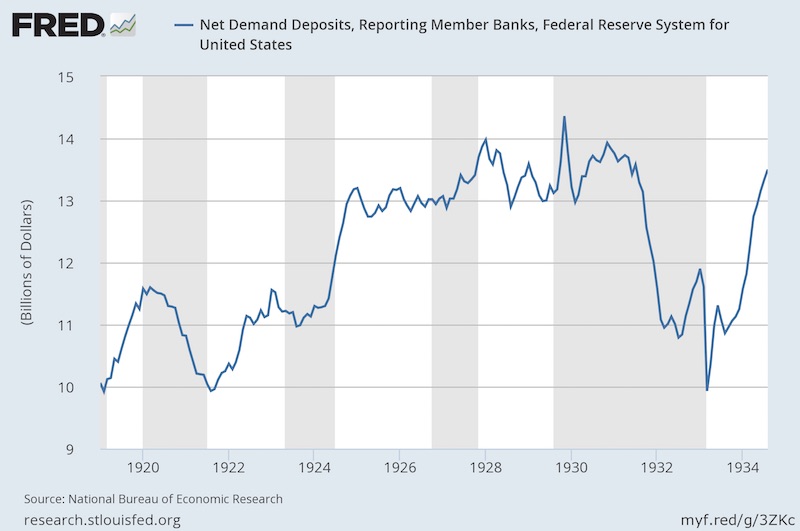

Demand deposits of “reporting” banks. Total deposits of “reporting” banks were about $20.5 billion at the end of 1929.

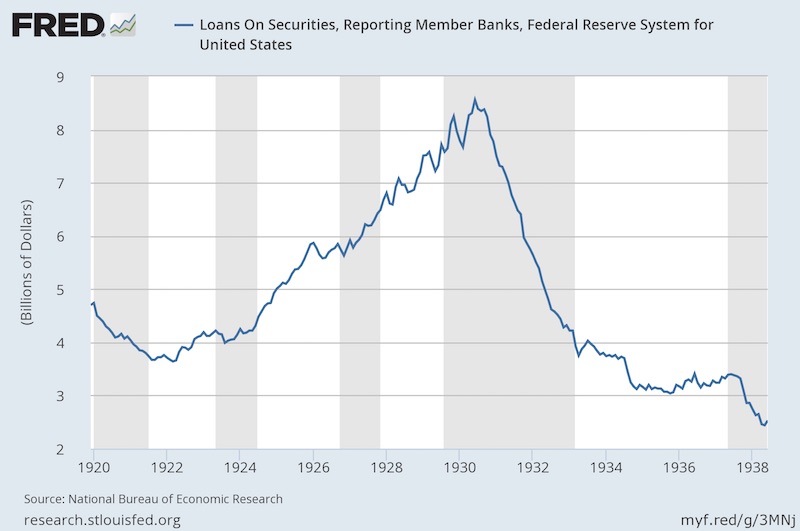

Loans on securities. This seems like an extraordinarily high number to me. It includes margin lending on stocks, but might also include a wide variety of collateralized lending. A big rise and fall here. However, the fall does not begin until 1931. Margin lending on stocks would have been through securities brokers, not banks, although the brokers would have needed financing for loans from banks. Also, in this pre-Glass-Steagall time, banks and brokers could be combined.

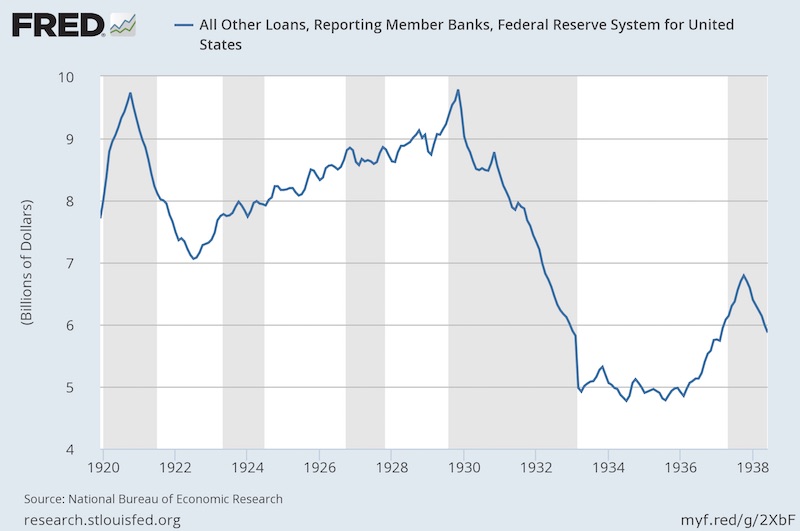

All other loans (i.e. not lending on securities). I’m amazed that “all other loans” are about the same as securities lending. Not a lot of expansion here, even with the roaring economy of the time.

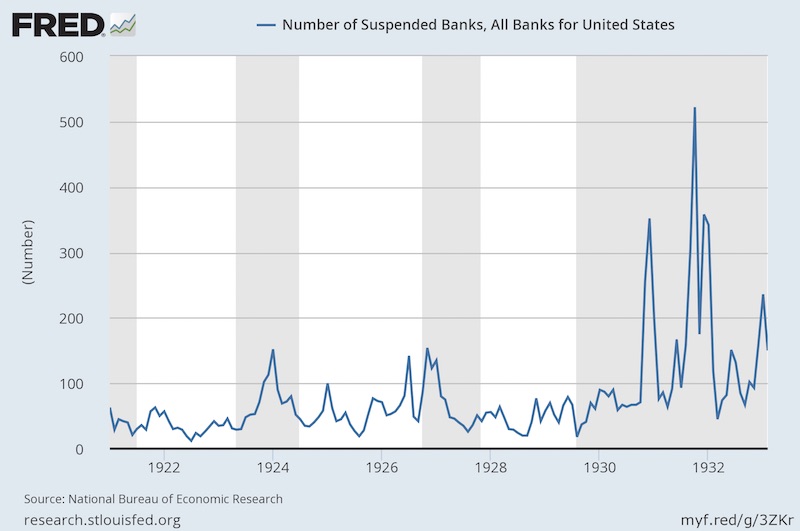

Suspended banks.

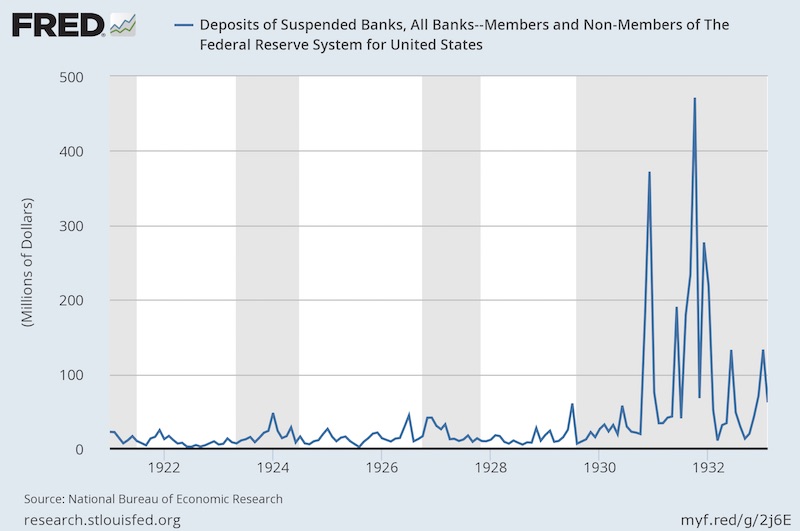

Deposits of suspended banks. Not such a large proportion of the roughly $42 billion of deposits at all banks.

That’s all for this week.