Stable Money

September 5, 2010

“The gold standard” is the answer to a question. The question is: “How do we create stable money?”

Until you understand the importance of stable money — in short, until you ask the question — the answer won’t make any sense.

July 25, 2010: The Argument for a Gold Standard (2010 edition)

I spend most of the first chapter of my book Gold: the Once and Future Money, and in actuality all of my book, explaining why stable money is desirable. So, in some sense, this little essay serves as an enticement to learn, in much more detail, why stable money works, and why unstable money (floating currencies) do not, by reading the book. However, I don’t want to just repeat what I said in the book here, so let’s go at this in a slightly different fashion.

First of all, what is a “stable money?” It is money that doesn’t change value. Its “purchasing power” may change. For example, a twenty-dollar bill has less “purchasing power” in downtown San Francisco than it does in Bozeman, Montana. In other words, prices tend to be higher in San Francisco than Bozeman. However, the value of the dollar is the same. In the past, people discovered that gold is stable in value. So, if their currency’s value was linked to gold, then the value of their currency would also be unchanging, or at least as stable as gold. For the most part, this worked beautifully. But, even if you didn’t take gold to be a benchmark of monetary stability, you could still use the same principle and devise some other system with the goal of maintaining a stable currency value. However, historically, this never happened. There never has been, to my knowledge, a currency system whose aim was stability of value, that used some other method than a gold (or occasionally silver) standard.

The idea that stable money is good used to be self-evident. I say that no economic problem in history has been caused by stable money. Without getting into the theoretical specifics, we understand this instinctively from daily experience. Have you ever seen this on CNBC?

Peter Moneyshuffler: Well, Maria, it really comes down to this. The currency is much too stable. The government needs to make the currency much more unstable. Nothing is going to get better until this excessive stability problem is resolved.

Maria: Norbert? What do you think?

Norbert Bigdome: This is contrary to all the known laws of economics. Capitalism simply cannot function with a stable unit of account. An unstable currency is one of the primary means by which speculators can appropriate the wealth of the productive classes. The currency in Anglia has been so stable, that speculators’ profits have fallen miserably. We all know what that means in today’s speculation-based economy. Financial engineering as a percentage of GDP has fallen to perilously low levels. Instead, the economy is focused on producing useful goods and services, which, of course, is unproductive.

Peter Moneyshuffler: Maria, there hasn’t been an asset market bubble in Anglia in at least twenty years. During my entire professional career, interest rates have fluctuated in a 100 basis point range. I’ve been reduced to reading financial statements and researching business plans. Frankly, Maria, for a moneyshuffler of my stature, it’s embarrassing.

Maria: Let’s go now to Bob Pisani, who is on the street in Robertsburg, Anglia’s capitol, where public demonstrations have broken out criticising the government’s response to the economic crisis.

Bob Pisani: Maria, it’s incredible down here. People are showing their anger at a government they call corrupt and incompetent. Let’s see what they have to say. (Turns to demonstrator.) You sir, what are you most angry about?

Demonstrator 1: We’re having a currency crisis! Look, I have here a ten-dragoon note. Ten years ago, I could buy lunch with this. Or get a taxi ride across town. Today, I can still buy lunch with it, and taxi prices are about the same. Can you believe that? Its value hasn’t changed a bit. Not in ten years! My gold investments have been a total disappointment.

Demonstrator 2: Our government promised us that the value of the currency would fluctuate unpredictably, and possibly even collapse. Instead, it has remained pegged to gold for the last fifty years. The way things are going, it might remain pegged to gold for the next fifty years. How am I supposed to run a business like this? What does this mean for my children? I feel betrayed.

Never happens, does it? And yet, if you look at the present state of understanding, almost nobody today is an advocate of stable currencies. Everyone is the other way. They think they can solve all their problems with currency manipulation. For the last eighty years, economists have been building up a sort of religion of currency manipulation. This is expressed in our present floating-currency system. There are no stable currencies today. There isn’t even a single government that attempts to create a stable currency.

Thus, we have two different viewpoints: the stable money people, and the funny money people.

April 26, 2009: Two Monetary Paradigms

“Stable money” is itself the answer to another question. The question is: “What is the best way to manage a capitalist economy?”

You can make a lot of intellectual arguments regarding this topic, but I think it is best to start with a brief overview of history. I’ll do a little handwaving and say that “capitalism,” as an economic system, emerged most recently in Europe from the end of the Middle Ages, around the 14th century. The Middle Ages were characterized by a simple agrarian system, in which households (or, more broadly, the medieval manor), were more-or-less self-sufficient. People grew their own food, made their own houses, and made most of their other household goods such as clothing, using locally-available materials, without interacting, in a commercial sense, outside of their immediate environs. Money wasn’t used much, and monetary contracts, such as stocks, bonds, employment contracts, pensions and so forth, were rare. Then, we have the growth of capitalism from about the Renaissance period. The early capitalists were found mostly in Italy, in places like Florence, Venice or Genoa. By the 17th century, Europe’s most impressive capitalist powerhouse was Holland. The 18th and 19th centuries were dominated by Britain, with Germany, the U.S. and Japan taking a role in the later 19th century. The United States took over the lead in the 20th century.

During this time, there were many, many experiments with all sorts of floating currencies, devaluations, and whatnot. Hundreds and hundreds of experiments with every sort of unstable-money system. You can read This Time Is Different for a very brief overview of what I’m talking about. Glyn Davies’ A History of Money is also a wonderful reference. You can even go back to the Plato/Aristotle debates, where Plato was a soft-money guy and Aristotle was a hard-money guy. Also, during this time, there were hundreds of experiments with stable money systems, which, historically, has always meant a gold standard. I guess nobody could think of a better one — although they tried, and you can look at the discussions in the 1870s about William Jevons’ commodity basket proposal if you like.

The point is: the great successes during the entire modern history of capitalism over the past 600 years or so were all hard-money systems. At the end of the day, a capitalist economy is an economy of cooperation. No longer do we grow our own food, make our own houses, and sew our own clothes from fabric that we wove ourselves from thread that we spun ourselves from flax that we grew ourselves. Although this cooperation is anonymous, and often has competitive elements, nevertheless, the way in which we produce our goods and services is by specialization and trade. If you think of a capitalist system as a vast network of cooperation, organized by money, money-measurements (profit and loss), and money contracts, then it is easy to see that if this fantastically complex system of cooperation is organized via money, then it is important to keep this “communication system” as clear and uncorrupted as possible. Thus, humans have always sought the most stable money possible, and concluded that gold is the best real-world representation of this ideal of perfect, unchanging stable money.

In short, the capitalist cooperation-system (specialization and trade) works best with stable money. That’s why all the great economic successes over the past 600 years were those that had stable money, i.e., gold-linked money.

August 5, 2006: What is Economics About?

This was the case up until 1971, when the world left the gold standard. At first, the dollar floated, but all major currencies remained pegged to the dollar so exchange rates were stable. Today’s floating-currency system did not fully appear until 1973, when major currencies began to float against the dollar. This system was never planned. There was never a great international convention, like the Bretton Woods meeting of 1944, in which everyone discussed the pros and cons and concluded that we should have a floating currency system. The break with gold in 1971 was an unplanned consequence of Richard Nixon’s attempt to goose the U.S. economy with “easy money” before presidential elections in 1972. Oops!

I’m trying to put a picture in your head: 600 years in which the biggest, most successful capitalist industrial economies (Britain, U.S., Germany, Japan) all had hard money/gold standard systems, against 40 years in which we’ve had worldwide chaos as the consequences of the funny-money manipulators’ attempts to fix economic problems with currency games. 600 years vs. 40 years. And yet, somehow, during those 40 years, the funny-money guys have managed to convince everyone that the previous 600 successful years did not exist, or are irrelevant.

I like to represent this 600 years of stable money:40 years of floating money ratio with this graph of the value of the “dollar,” which was originally a standardized European coin called the “thaler.” We see that the “dollar/thaler” didn’t change in value from its inception in 1513 until 1933, where it undergoes a single step-devaluation. The “floating dollar” doesn’t appear until 1971. It’s that little wiggle on the far right of the chart.

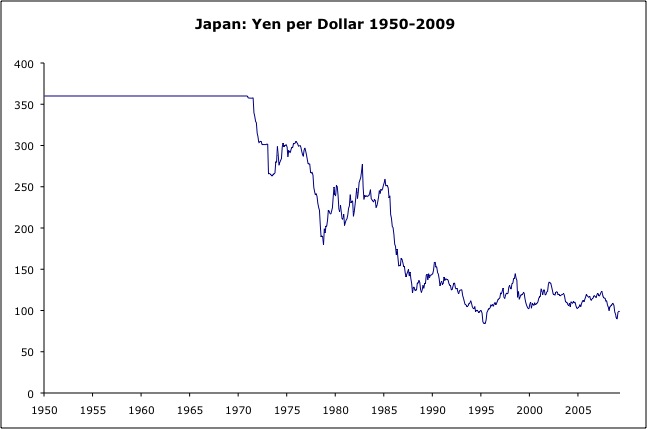

Likewise, if you have two countries with currencies pegged to gold, then of course the two currencies have stable exchange rates. I don’t think people today believe me when I say that exchange rates used to be stable and unchanging. This chart helps:

That’s the way it’s supposed to work. The way capitalism is supposed to look.

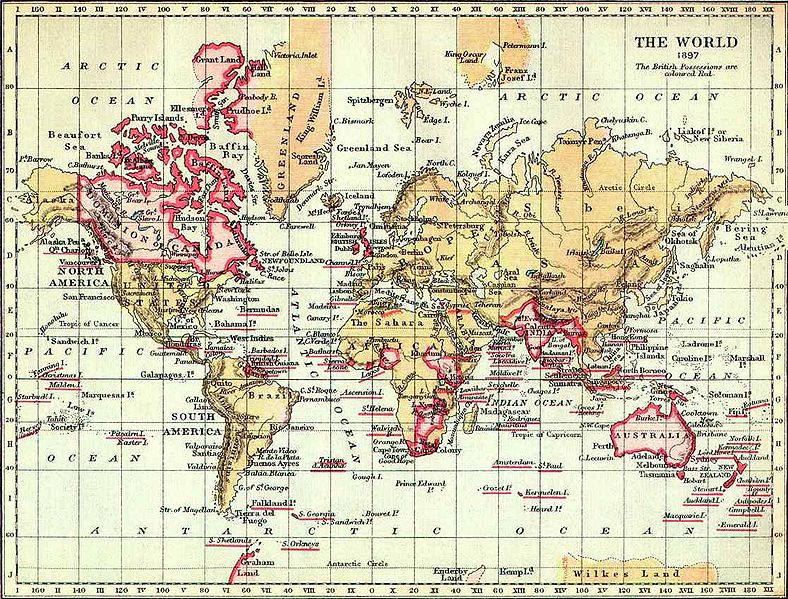

The funny-money guys all try to convice you that if you adopt a gold standard, your head will explode. How is it, then, that Britain, which has one of the greatest records of currency stability in the world, 233 years of a gold standard at the same parity (1698-1931, with some lapses), became in the 19th century:

The world’s leading financial center

The source of the world’s premier international currency

The center of an empire that spanned the globe

British Empire, 1897. Islands that were part of the Empire are underlined in red.

British 5-pound gold coin.

After 1931, Britain descended into Keynesian money manipulation, with a series of devaluations between 1931 and 1971. Britain’s industrial leadership? Poof! Premier international currency? Kaput! World-spanning empire? Gone! It is still a leading financial center, although that may be in part because The City is not quite the same as Britain.

The baton was handed to the United States. The U.S. has perhaps the second-best record of hard-money stability in the world, with 182 years (1789-1971, with some lapses) on the gold standard with just one permanent devaluation in 1933. As a result, in the 20th century, the U.S. became:

The world’s leading financial center

The source of the world’s premier international currency

The center of an empire that spanned the globe

Wow, what a coincidence! The same action produces the same results! Yes, people, it really is that obvious. Guess what: their heads didn’t explode. Instead they became a global colossus.

What about Holland? Remember them? They were the economic leaders of Europe before Britain adopted the gold standard in 1698. During the 17th century, Holland’s era of economic pre-eminence, they enjoyed a gold standard organized around the Bank of Amsterdam. And what happened? During that time, Holland was:

The world’s leading financial center

The source of the world’s premier international currency

The center of an empire that spanned the globe

Think about that. Holland! A rinky dinky nowhere, on some of the worst land of all of Europe. The population of Holland was 1.8 million people in 1700, and less before then. The population of Amsterdam in 1660 was 200,000. And yet, this 1.8 million people from rinkydinkyland — this is the population of greater Charlotte, North Carolina — were able to build an empire that included parts of (or all of) today’s:

Taiwan

Australia

Iran

Iraq

Pakistan

Yemen

Bangladesh

India

Indonesia

Oman

Burma

Thailand

Malaysia

Cambodia

Vietnam

China

Japan

South Africa

New Netherlands (United States, including New Amsterdam, now known as New York)

Netherlands Antilles and Aruba

Suriname

Guyana

Brazil

Virgin Islands

Tobago

Colombia

Chile

Ghana

No exploding heads in Holland either. Try to imagine, if you can, the people of Charlotte, North Carolina conquering the world. Actually, the Dutch were more interested in trade than conquest, but you get the idea.

The U.S. has been able to hold onto its top-dog position despite leaving gold in 1971, because the dollar has been the most stable currency in a world of worse options.

The U.S. middle class used to be an amazing story of ever-increasing wealth and prosperity. However, the middle class hit the wall exactly when we went from hard money to soft money, in the early 1970s.

June 21, 2010: What Happened to the Middle Class?

Wow, what a coincidence! Soft money produces economic stagnancy and decline, exactly like the hard money guys have been saying for six hundred years!

The same action produces the same results!

“Soft money” usually means a currency that declines in value. Sometimes there is a persistent rise, as Japan experienced in the 1985-2004 period. But that is very, very rare. Sometimes there is a period of fluctuation within a range, as was the case in the U.S. in 1982-2004. This causes a persistent ill-health and underperformance. However, in the long-term picture, “soft money” inevitably means “easy money” during a period of economic weakness, and this ultimately leads to declining currency value.

When a currency loses value, then obviously nominal wages paid in that currency also lose value. Wages may rise to offset this currency devaluation, but they usually do not rise anywhere near the degree that the currency declined, so on balance wages fall in real, devaluation-adjusted terms, which in practice means in terms of gold. This makes perfect sense from a productivity standpoint as well. Most any economist will tell you that wealth is a direct function of productivity. You can’t enjoy more goods and services unless you make more goods and services. Where would they come from otherwise? Outer space? Since unstable money distorts and corrupts the capitalist cooperative system of specialization and trade, we can see that we cannot generate more productivity from making a mess of the system that makes productivity possible. In short, productivity will also decline as a result of currency instability, which is why that although nominal wages may rise in response to the currency devaluation, they do not reach their old peaks, except perhaps after a few decades of recovery.

To summarize: soft money = lower wages. Obviously, if wealth/productivity/economic health and vigorousness is represented by higher wages, then a method that produces lower wages isn’t going to get you there, is it?

These are “weekly wages of production workers,” excluding management, income from capital, healthcare costs and other nonwage compensation, etc.

Or, as they used to say: “You can’t devalue yourself to prosperity.”

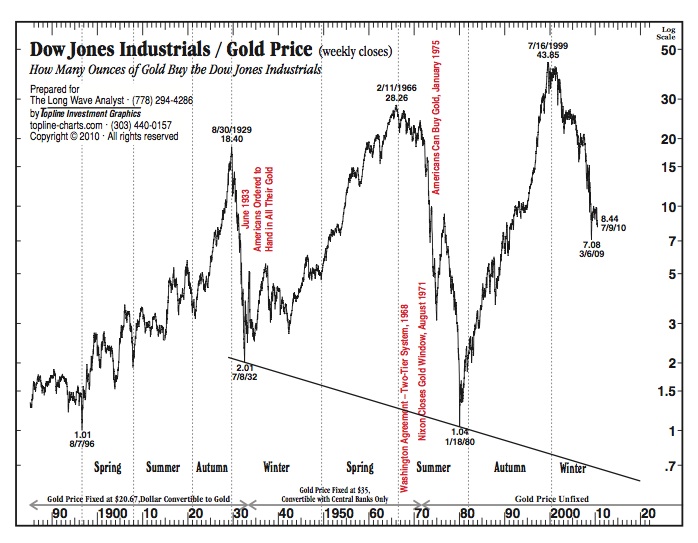

Just as currency instability/devaluation results in poorer workers, it also results in poorer corporations. Here’s the Dow Jones Industrial Average, as measured in real money — gold.

Whoops!

April 15, 2007: The Value of Today’s Dollars in 1854 Dollars

Traditionally, the hard money guys have run into difficulties when faced with a recession. They tend to want to stand around and “do nothing.” This is not an easy political sell even when it is the right thing to do, but it is even worse when it leads to a sort of obliviousness about economic developments. The Classical economists’ solution to the exploding worldwide trade war set off by the Smoot-Hawley Tariff in the U.S. in 1930 (with preparations in 1929), was: do nothing! When this was followed by an even more destructive trend around the developed world toward soaring domestic tax hikes, exemplified by the 1932 Hoover tax hike, their response again was: do nothing! Even in less dramatic times, economists need a better solution than: do nothing. In fact there is quite a bit a government can do instead of “easy money.” I’ve listed a few options:

June 27, 2010: U.S. Tax Hikes of the 1930s

September 14, 2008: Depression Economics

October 12, 2008: Effective Bank Recapitalization 2: Three Examples

October 5, 2008: Effective Bank Recapitalization

September 28, 2008: Every Crisis is Like All the Others

January 27, 2008: Crisis Management

November 10, 2008: “Austerity”

November 2, 2008: “Stimulus”

January 18, 2009: “Austerity” and “Stimulus” 2.0

June 24, 2010: Stimulus, Austerity, and the Spiral of Decline

December 9, 2008: Preventing Bubbles

April 6, 2008: Liquidationists vs. Interventionists

May 2, 2010: Thoughts on Greece

May 30, 2010: The Flat Tax in Russia

The soft-money guys really come into their own when politicians are looking for solutions to their problems. This might be something minor, like Nixon’s re-election plan, or something major, like the Great Depression. The soft-money guys have a zillion proposals, although they all boil down to the same proposal: “easy money.” Combined with government “stimulus” spending, it’s their one-size-fits-all soution for every kind of economic event. Politicians fall for this time and time again, because, often, it works! For at least a short time, it seems like the economy is improving, although as we’ve seen before this never seems to persist in any sort of “long run.” It’s all illusory. Plus, it doesn’t seem to cost anything, seems to bypass the difficulties of the democratic legislative process, seems like it can be implemented immediately, and generally flatters politicians’ Master of the Universe fantasies as they imagine themselves to be “macro fine-tuners” of some sort. When the inevitable long-term results appear — economic stagnation and decline — it is hard to attach blame on the soft-money managers, who are always ready with a blizzard of confusing nonsense to cloud the issue.

July 28, 2008: “Why Not the Gold Standard?”

March 23, 2010: China Vs. U.S.: Clashing Monetary Paradigms

Another very real problem with “hard money” today is that hardly anybody knows how to make it happen. Someone can say “oh, it would be so wonderful if we had a proper stable money/gold standard system,” but if they don’t know how to implement it, then the result could be a disaster. Most of the “hard money” proposals I’ve seen in recent years would almost certainly create a disaster. Unfortunately, noble sentiment alone is not enough. You need to have some technical competence to go with it. One reason that people cling to today’s soft-money system is that at least it is the Devil We Know. Thus far, from 1982 to the present, it seems to be tolerable enough, the “Great Moderation,” although that era is surely slipping by as we embark on a new phase of currency devaluation today. It won’t be until the Devil We Know is getting to be so horrible that people are willing to chance a turn at the ignorance and stupidity of today’s hard-money guys — the Devil We Don’t — that things may change. It would all be a lot easier if we just learned how to play this game properly, and then the transition could be an occasion of celebration.

January 3, 2010: The GLD Standard

November 23, 2008: Redeemability and Reserves

August 26, 2007: How To Operate a Gold Standard

August 19, 2007: Gold Standard Fallacies

June 2, 2008: World Without Paper Money

May 6, 2008: The Key to Managing Currencies