The Bank of England, 1844-1913 2: The Banking Department

April 28, 2013

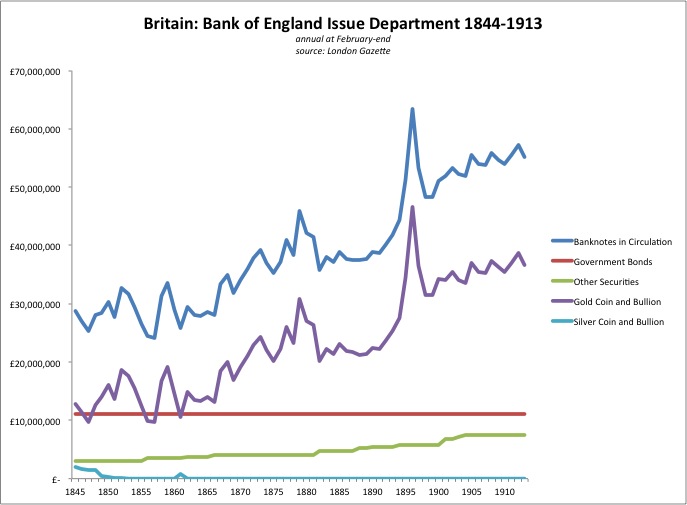

We are continuing our look at the Bank of England during the period 1844-1913. In 1844, the Bank fell under a new regulation and reorganization, in which it was separated into two entities, the Issue Department and the Banking Department. The Issue Department was solely responsible for paper banknotes, and operated a system very similar to the “Making Change” or currency-board type system we looked at earlier.

April 14, 2013: The Bank of England, 1844-1913

The Issue Department did not hold deposits. The only assets were gold bullion and bonds, either government bonds or “other securities,” most likely high-quality corporate bonds or gold-based bonds of other governments.

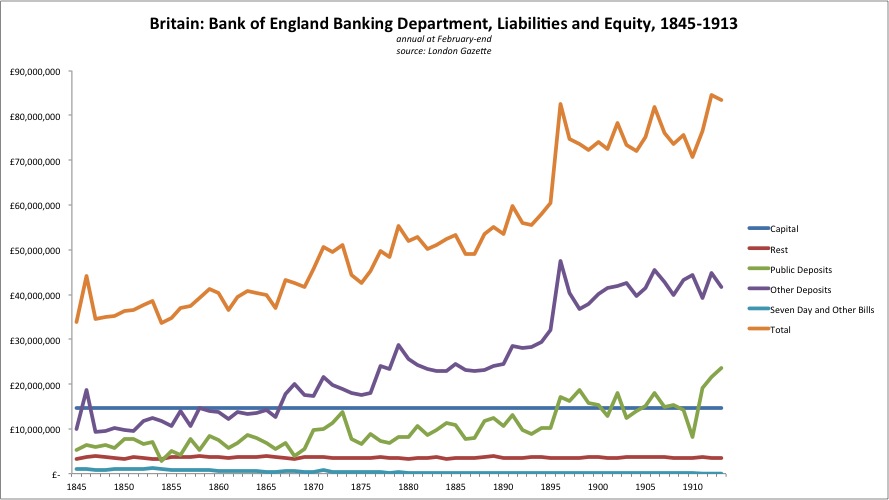

Here’s the liabilities side of the Banking Department’s balance sheet. “Capital” is the original shareholders’ investment. “Rest” amounts to retained earnings. “Capital” and “Rest” together constitute what we would call today shareholders’ equity or book value.

“Public Deposits” are demand deposits of government entities.

“Other Deposits” are demand deposits of nongovernment entities, mostly other banks.

Today, we recognize deposits at the central bank as a type of base money. Today, central banks hold both “public deposits” and “other deposits,” so we can combine them into aggregate deposits. Base money today consists of banknotes in circulation+public deposits+other deposits.

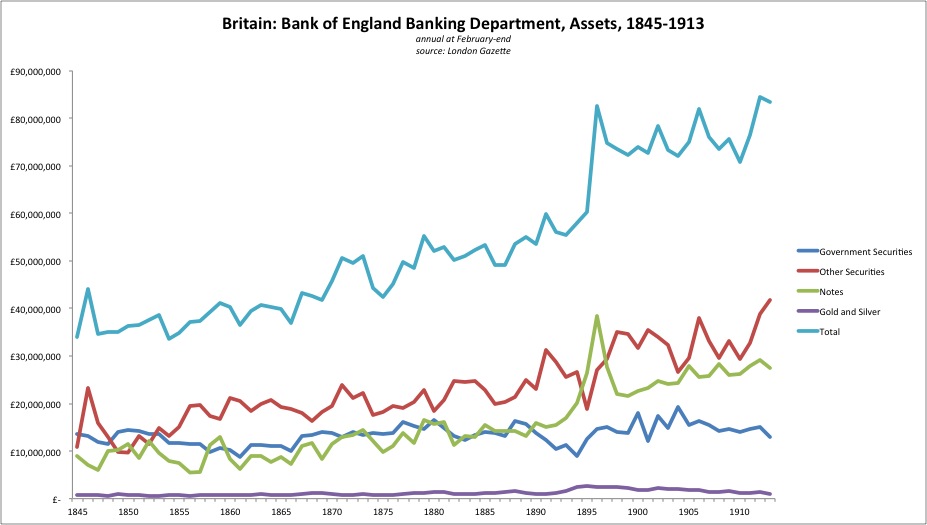

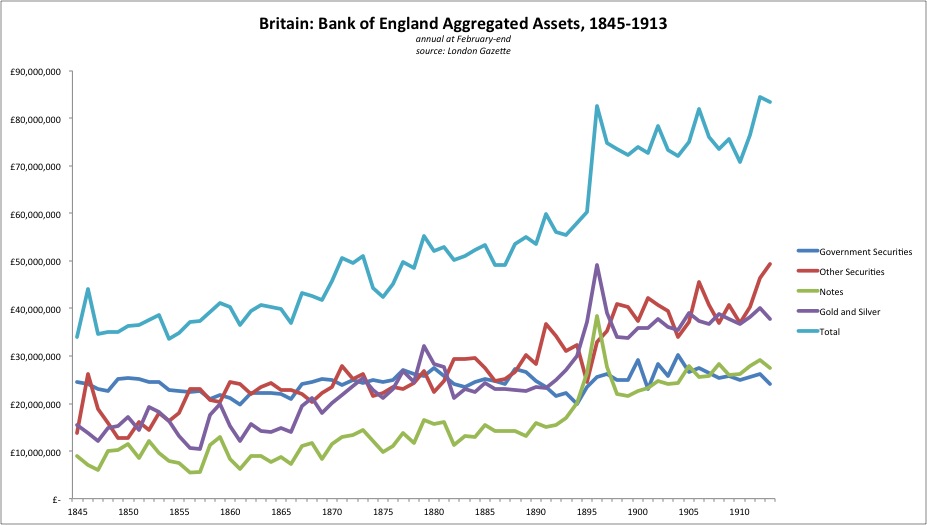

The Asset side of the balance sheet of the Banking Department looked like this. There was a little gold bullion, but not much. Government securities are of course government bonds, and we see that, unlike the Issue Department, they vary quite a lot.

I will have to look up the definitions of the other asset classes to be sure of what they mean. “Other securities” probably means corporate bonds. “Notes” probably means loans (promissory notes).

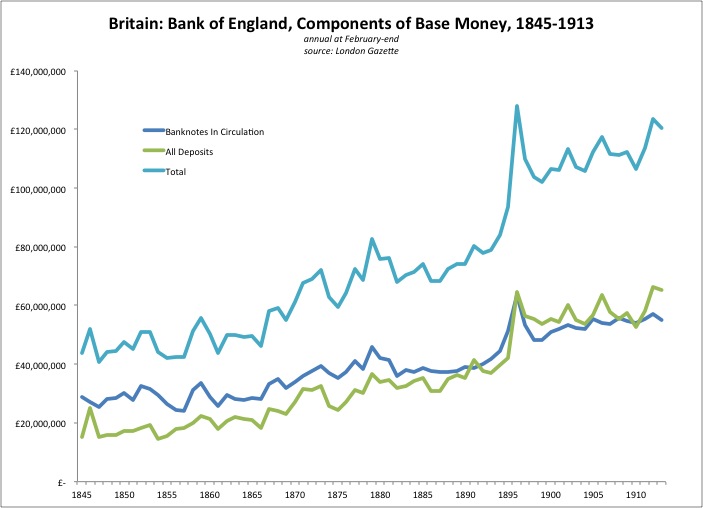

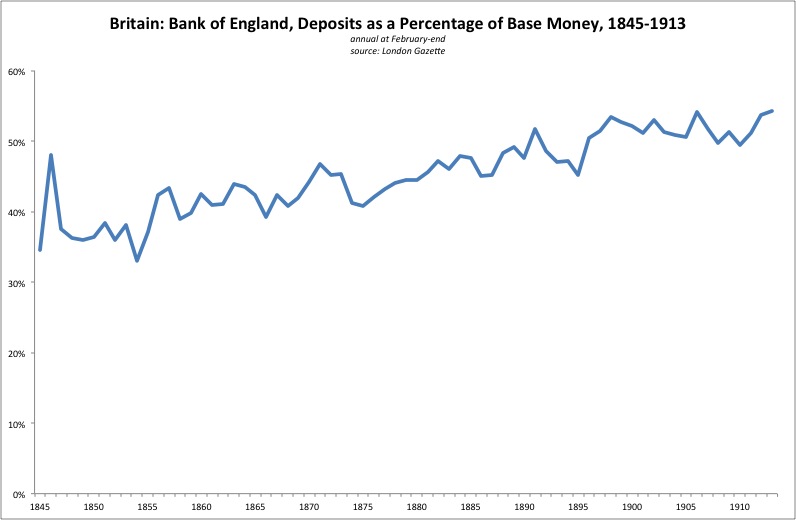

Here’s what it looks like when we combine the Issue Department and Banking Department. Banking Department deposits gradually became a larger and larger component of base money.

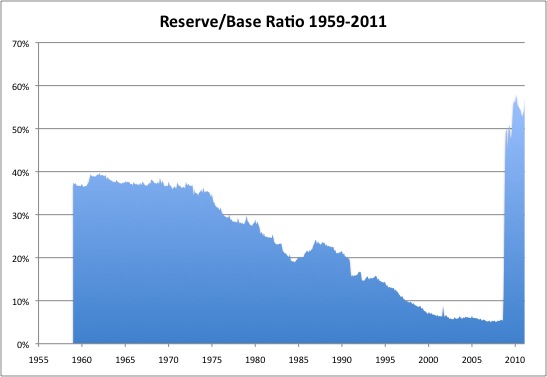

This was actually quite common at the time. In the United States as well, deposits at the central bank (“bank reserves”) were a large portion of base money, until just recently.

March 13, 2011: Bank Reserves 2: Reserves Out the Wazoo

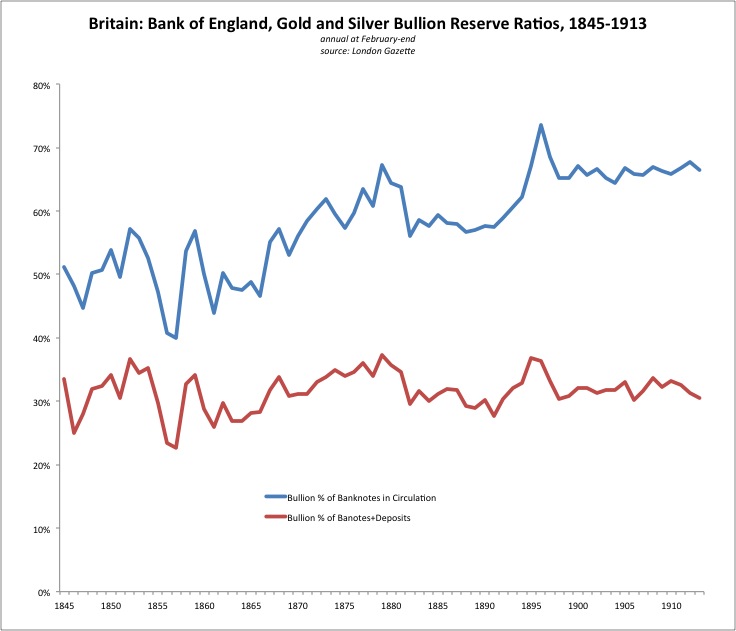

Taking into account banknotes in circulation alone, the gold bullion reserve ratio was about 60%. However, when including the deposit portion of base money, the bullion reserve ratio was quite stable around 30%.

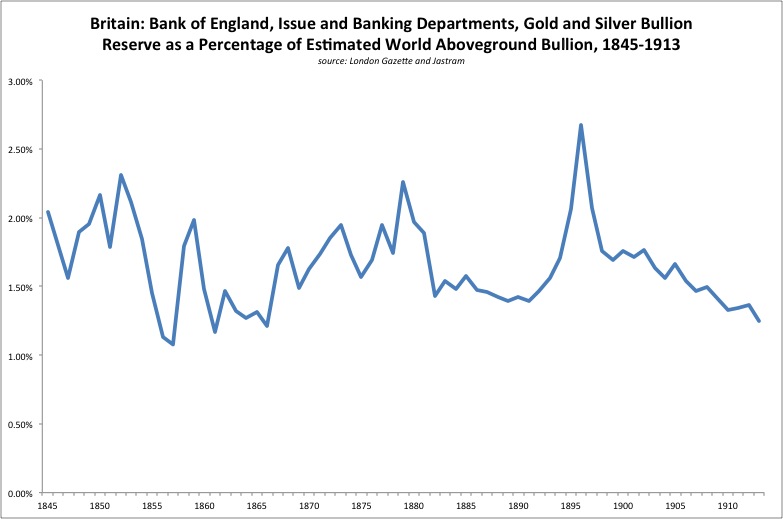

As a percentage of aboveground bullion, the Bank of England did not hold very much. It was around 1.50% during this seventy-year period. You can run the world’s premier reserve currency without holding a lot of gold bullion.

The liabilities of the Bank of England, both Departments combined, basically amounted to base money. On the asset side, this is what it looks like when we aggregate both the Issue and Banking Departments, mirroring central banks today.

Unlike the Issue Department, which ran an automatic currency-board like mechanism, the Banking Department had discretion as to how much it would expand or contract deposits. It did this by buying and selling government and other securities, and also adjusting the amount of loans (“notes”) it would make via changes in the Discount Rate (i.e. lending rate). If the Bank’s discount rate was generally above the prevailing market rate, people would pay back their loans to the Bank and the Bank would not make new loans, so lending (and thus base money) would contract. In practice, it appears that, toward the end of the 19th century, the Banking Department often managed aggregate base money by watching market exchange rates between the British Pound and other gold-based currencies worldwide such as the U.S. dollar. If the pound was sinking in value vs. the dollar, the Banking Department would sell government bonds. The money paid to the Banking Department for its bonds would most likely take the form of a deposit at the Bank. Thus, deposits would contract, shrinking the overall base money supply. Likewise, if the pound was a little strong on the forex market, the Banking Department would buy government bonds, thus increasing the amount of base money and lowering the value of the pound. The Banking Department could also buy or sell “other securities,” or let them mature without rolling them over, or adjust is lending via the Discount Rate or other means.

In practice, the Banking Department found that, toward the end of the 19th century, the effectiveness of discount rate adjustments, leading to adjustments in lending and thus base money, were becoming less effective due to the Banking Department’s shrinking market share of the short-term lending business. Thus, the Banking Department gradually moved toward open-market operations in government bonds and other bonds as a means of adjusting the monetary base. However, both techniques could be used together. This took place while the Issue Department also ran its own, currency-board-like automatic adjustment of banknotes in circulation, which also adjusted the monetary base.

Banknotes and deposits could be easily transferred one to the other. For example, if a bank wanted to “withdraw” its deposits in the form of banknotes, it could request the Banking Department to do so. The Banking Department would send gold bullion to the Issue Department and the Issue Department would send banknotes back. Or, the Banking Department could just buy bullion on the open market, and send it to the Issue Department, and thus not have to deplete its own (rather small) reserves. Likewise, if people had more banknotes than they wanted and preferred deposits, they could bring their banknotes to the Banking Department and get a deposit. If the Banking Department had too many banknotes, it would send the banknotes to the Issue Department, get gold bullion in return, and then either keep that or perhaps sell it on the world market. In other words, deposits and banknotes, two different forms of base money, were easily fungible.

January 29, 2012: Gold Standard Technical Operating Discussions 3: Automaticity Vs. Discretion

January 15, 2012: Gold Standard Technical Operating Discussions 2: More Variations

January 8, 2012: Some Gold Standand Technical Operating Discussions