We’ve been looking into the idea that there was some kind of sudden and very large rise in the value of gold, beginning in late 1929, that was a major contributor to the Great Depression.

September 11, 2016: The “Giant Rise in the Value of Gold” Theory of the 1930s

September 18, 2016: The “Giant Rise in the Value of Gold” Theory of the 1930s 2: Never Happened Before

Some of the conclusions we’ve come to so far:

2) The magnitude of the rise in gold’s value would have to be in excess of 100% (i.e., a doubling), perhaps far in excess, over a relatively short period of time of less than five years.

3) Commodity prices vs. gold were actually rather high in the 1920s, compared to historical norms, indicating that there was no long-term tendency for a “rise in gold’s value” (implying low nominal commodity prices) prior to late 1929.

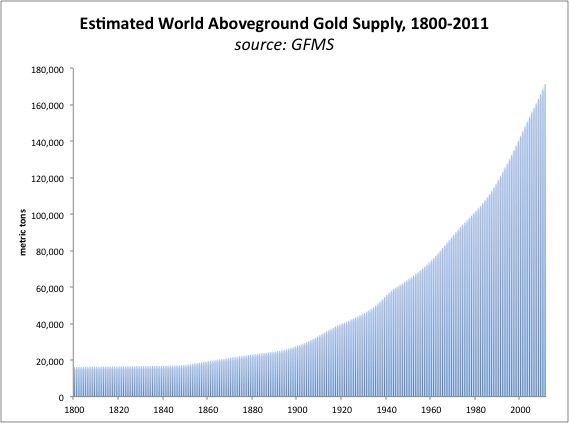

4) Because aboveground gold (“supply”) is much larger than annual mining production, variation in mining production has little effect on gold’s value. Even a 10x increase in production, in the 1840s and 1850s, did not produce much noticeable effect.

Certainly any kind of gigantic and unprecedented rise in gold’s value must be related to some kind of change in supply/demand conditions — of a sort not seen in at least 500 years. Let’s keep looking at the supply and production side of things.

Here is aboveground supply, as estimated by GFMS. This smooth curve represents the gradual accumulation of gold from mining production.

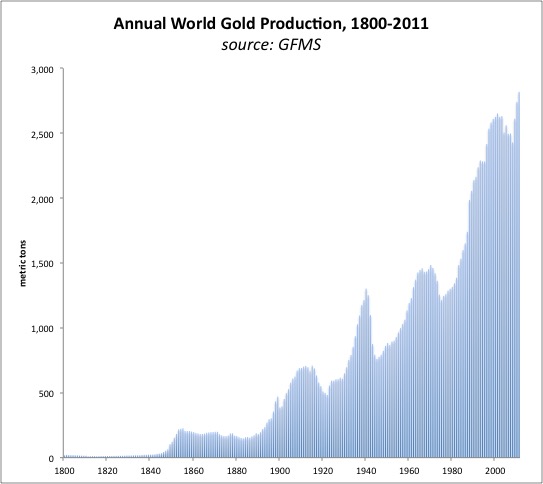

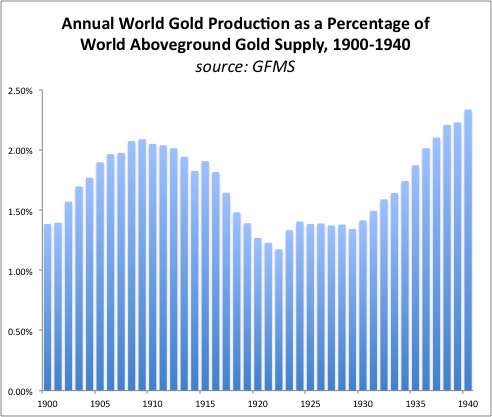

Here is mining production.

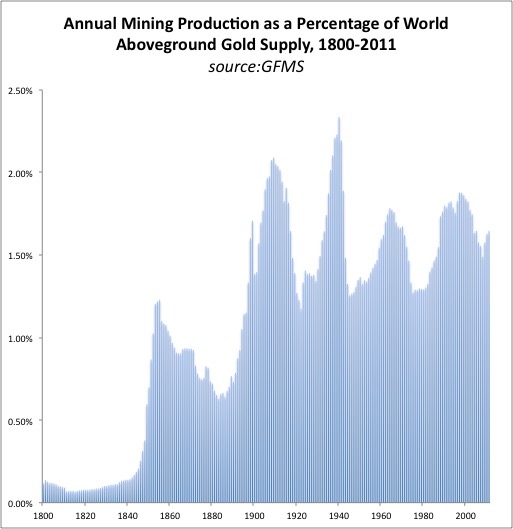

Here is production as a percentage of aboveground gold. We see that there was indeed some falloff in production during the 1920s, but from peak levels to levels that were still relatively high.

Now we will look at “demand,” in particular, demand from central banks for reserve holdings — the core of Gustav Cassel’s arguments. We’ve looked at this before, but we can go over some of the data again.

Beginning around 1850, central banks spread around the world, and with them, paper banknotes. These central banks held a considerable amount of bullion in reserve. The increase in central bank holdings of bullion was fingered for falling commodity prices in the 1880s and 1890s — although, I again will point out that these prices also reflected the supply glut of many commodities at the time. It was a time when people were scratching around for any kind of excuse to devalue currencies using various “free coinage of silver” arguments, not only in the U.S. but around the world.

The following data comes from Timothy Green’s 1999 paper, “Central Bank Gold Reserves: an Historical Perspective Since 1845”, available here:

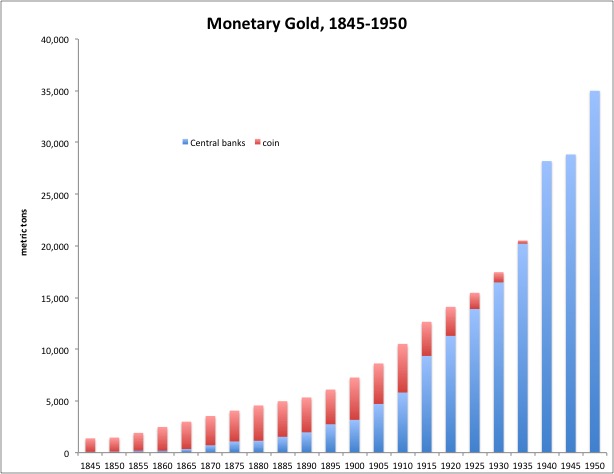

Here we can see that big rise in central bank gold holdings, which continued to about 1950. Before 1925 or so, much of the increase in central bank gold reserves came about via the reduction in circulating gold coinage — people “deposited” their coins for banknotes.

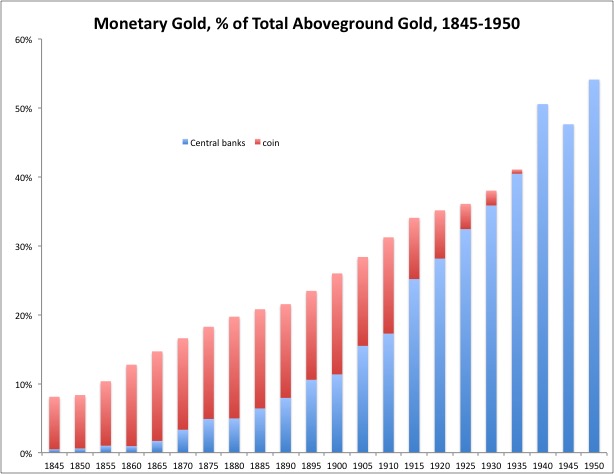

This is what it looks like as a percentage of estimated total aboveground gold, using the GFMS estimates.

What do we see here?

First, we see that by 1895, central banks didn’t really hold all that much gold — a little less than 10% of aboveground gold, by this chart. I find it very difficult to ascribe any effect at all to gold “demand” from central banks, or other monetary uses, to some kind of rise in gold’s value in the 1880-1895 period. That is one reason why I think that the decline in commodity prices worldwide 1880-1895 was primarily, and perhaps entirely, a matter of a supply glut of commodities.

We get a little more of a rise between 1925 and 1935, but it is still pretty small. Remember, even by early 1929 commodity prices were highish, and economies were generally doing quite well, so there was little evidence that all the accumulation of gold by central banks in the 84 years between 1845 and 1929 created any kind of rise in gold’s value. Also, the continuing accumulation 1935-1950 (which is much more dramatic) also did not cause any noticeable evidence of a rise in gold’s value — commodity prices after WWII were again toward the highish end of their long-term range. If gold did rise in value 1929-1933, then it would have had to fall again 1935-1950 to cause commodity prices to return to around their 1920s levels vs. gold. So, if you are going to argue that the increase in central bank gold reserves 1929-1933 had some kind of catastrophic effect, then you also would have to argue that the much larger increase in reserves 1935-1950 not only had no effect, but actually the opposite effect!

As you can see, these arguments are quickly becoming rather silly.

Also note the dramatic decline in circulating gold coinage throughout the world, by 1930. You might expect that there would have been some kind of dramatic rush towards gold coinage, as people withdrew their bank deposits for fear of bank failure. This indeed happened, but the magnitude was very small. Also, by the end of 1931, many countries were already off the gold standard. There is no evidence here of any private-sector surge in gold demand, at least in the form of coinage.

Green’s data is nice because it includes both gold coinage worldwide and central bank reserves. Now, let’s take a little closer look with annual data. Unfortunately, we now have to give up our worldwide data on circulating coinage.

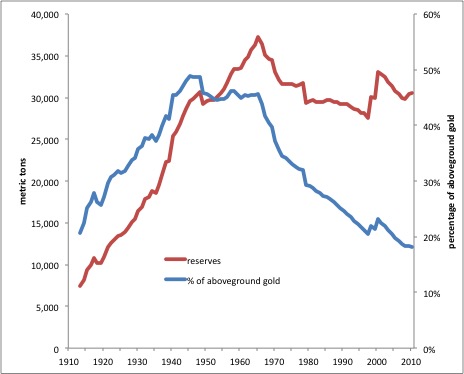

Here are central bank gold reserves, 1913-2010, in terms of tonnage and also as a percentage of aboveground gold. We see the rise in reserves until the late 1960s, after which it flatlines.

What do we see here? The increase in central bank gold reserves was very smooth during this period. This is a surprising result. The outbreak of World War I, the floating of currencies worldwide, the return to gold in the 1920s, the Great Depression and the breakdown of gold standard systems, and even World War II, did not seem to alter this trend of accumulation much at all.

Rather pointedly, we see absolutely nothing happening around 1929-1933. All of the central bank bullion accumulation between 1845 and 1929 did not cause any noticeable increase in gold’s value — commodity prices in the 1920s were rather high. Nor did all of the bullion accumulation after 1935, which resulted in highish commodity prices vs. gold again after WWII. There was absolutely no change in central bank bullion accumulation behavior at all around 1929-1933. So how did some kind of catastrophe occur during those four years, which did not happen in the other hundred years of gold accumulation between 1850 and 1950?

Anyone claiming some first-time-in-500-years explosion of gold’s value beginning around 1929 — of catastrophic Great Depression-causing magnitude — has, to my eyes, nothing to go on from either the supply side or the demand side. Not even a little wiggle.

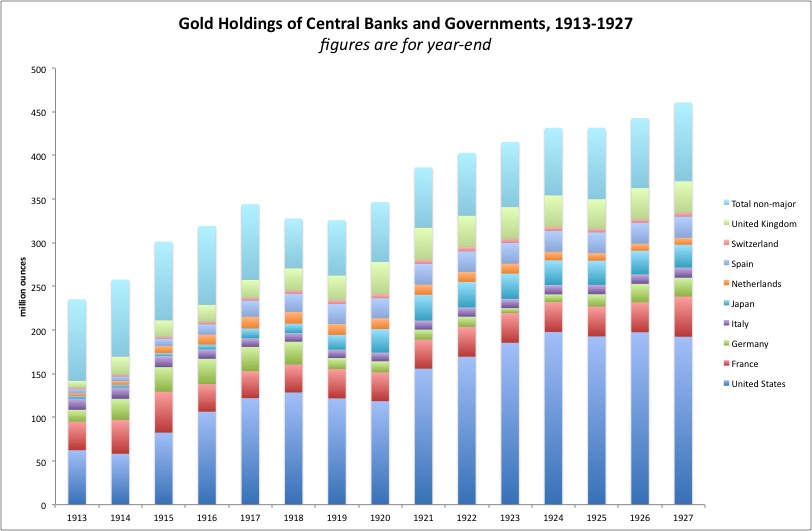

Here’s a closer look at annual data, for the 1913-1927 period. This is from the Federal Reserve’s Banking and Monetary Statistics. Once again, we see surprisingly little going on here, despite all the turmoil of war, floating currencies, and the return to gold in the 1920s.

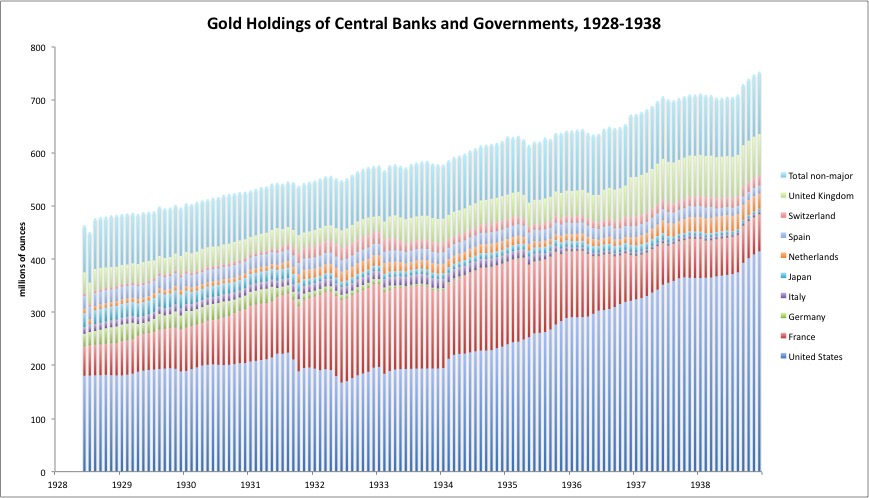

Here’s monthly data, for the key time period of 1928-1938. Remember, we are looking for evidence of some kind of catastrophic supply/demand imbalance beginning around the second half of 1929. It has to be big enough to cause a rise in gold’s value sufficient to blow up the world economy.

Look closely. Look very, very closely.

Nothing, right? France did accumulate some gold, but this was offset by moderation elsewhere. Total central bank gold reserves have a smooth trend of accumulation, with nary a ripply despite all the turmoil of the time.

We’ve been beating this horse a long time now, but it is not quite dead, so let’s continue with another thought:

Let’s say that there really was some kind of dramatic rise in gold’s value 1929-1933. What would we expect to see in that case?

Central banks would have had to force their currencies higher in response, to “catch up” to the rising gold value. This would have probably involved some kind of monetary base contraction — at least, some kind of change in behavior, in reaction to the once-in-500-years Great-Depression-causing dislocation supposedly taking place. A similar sort of thing happened in Argentina and Hong Kong in 1997-1998, where currency boards had to keep up with a rising value of the U.S. dollar, their “standard of value” at the time. A similar thing also happened in the 1919-1922 period, when a weak dollar following the printing-press finance of WWI (causing gold outflows once the gold embargo was lifted) was corrected by a large monetary base contraction.

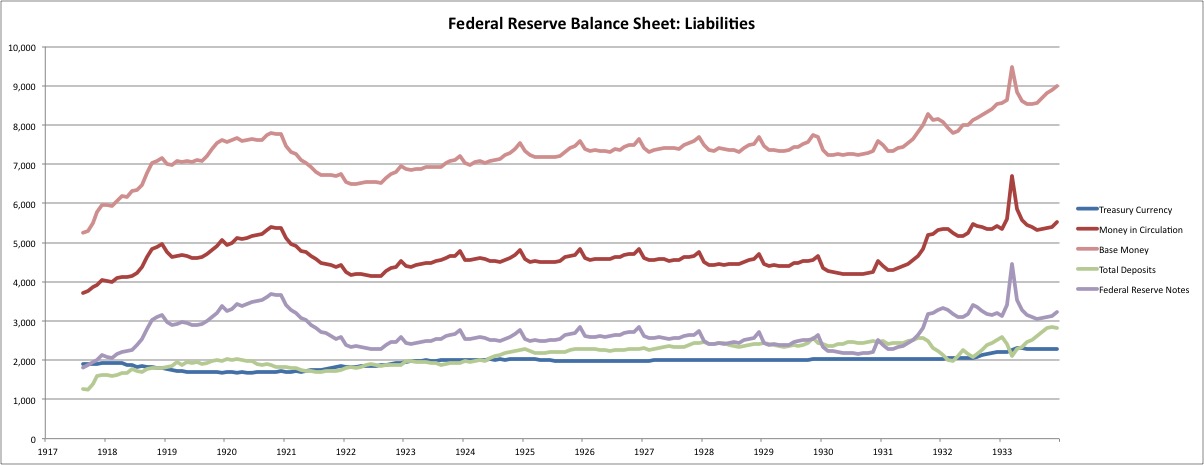

But, there was no such monetary base contraction, among major central banks, in the 1929-1930 period.

July 31, 2016: Blame France 2: Balance Sheet Peeping

We see nothing here that indicates a response to some kind of powerful rise in gold’s value beginning in late 1929. Everything is about as placid as can be until after the disruptive British devaluation of September 1931. There is no contraction of the monetary base, but rather, a rise.

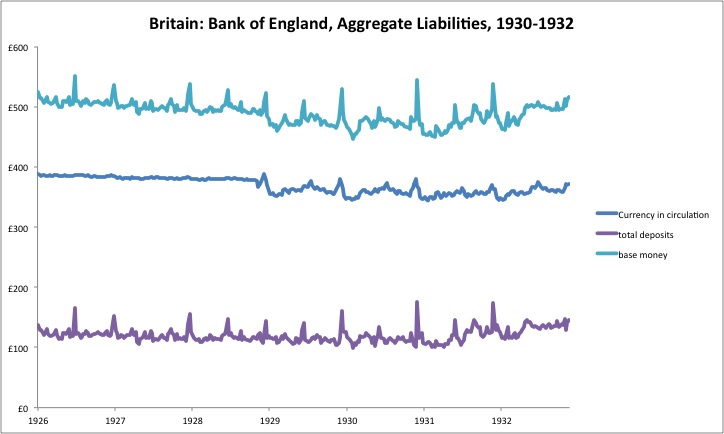

Nothing at the Bank of England either.

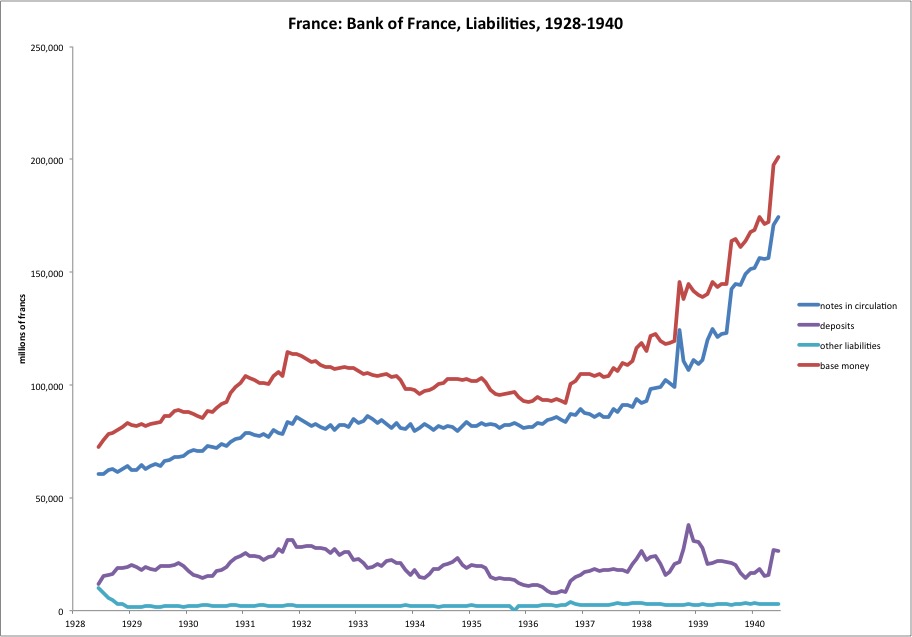

And nothing at the Bank of France, where we find a substantial monetary base expansion.

So again, nothing here to support the hypothesis of some kind of catastrophic rise in gold’s value.

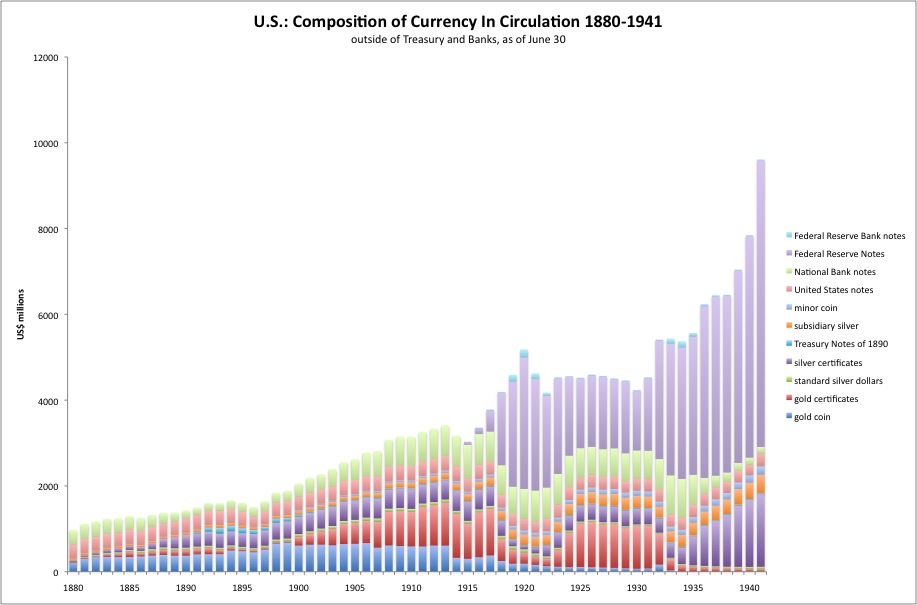

Here’s a look at gold coinage in circulation in the U.S.:

We see nothing here in 1929, 1930 and 1931 — no evidence of any new demand for gold coins. There is a peak of gold coinage in circulation in 1899, and a steady decline afterwards — mirroring the worldwide data we saw earlier. There was indeed a rise in gold coinage in 1932, probably representing a flight from failing banks and the potential for dollar devaluation (remember the big Federal Reserve open-market purchases of that year). The dollar was in fact devalued in 1933. But, this rise in coinage was rather minor in the scheme of things. You could extend this to gold demand for “safe haven investment” as a whole — that there was, strangely as it may sound given what we know, hardly any such demand in 1929-1931. It is hard to imagine some kind of powerful demand for large bullion bars, and no demand for gold coins. The U.S. Treasury gold certificates could be converted to gold on demand, in large size. Again, there is some contraction of the Treasury gold certificates in 1932, but the scale is small. After March 1933, U.S. citizens could not own any gold at all, which sort of eliminates “demand” one would think, not to mention the confiscation of existing gold holdings, which is a sort of forced “negative demand”. I don’t know how prevalent similar restrictions on gold ownership were worldwide, but I would guess it was pretty common in Europe by the late 1930s. In any case, due to its size and also the wealth of its citizens, the U.S. was probably one of the most important countries as regards these topics.

To summarize all of this, here’s what I see: very little evidence of any supply-demand imbalance that led to a rise in gold’s value during the 1880-1895 period; and certainly no evidence of some kind of supply/demand imbalance causing world-economy-destroying effects in 1929-1933. Thus, I conclude that in both cases, gold served as it always had, as a stable measure of value, the “monetary polaris.” The decline in commodity prices in the 1929-1933 period was due to a collapse in demand, caused by a worldwide economic breakdown due to nonmonetary reasons — primarily a global tariff war and domestic tax increases, plus “systemic” issues including bank failure and sovereign default, often an anti-business regulatory attack, and political instability. After the British devaluation of 1931, monetary effects also enter the picture.

Today, I’m mostly addressing the arguments of Gustav Cassel, and those who reference Cassel while making similar arguments today. Cassel formed his notions in response to the decline in commodity prices in the 1880-1895 period — a time when central bank bullion accumulation was still quite low. By the late 1920s, there was ample evidence that all the bullion accumulation by central banks over the decades up to that date had little effect on gold’s value. Cassel nevertheless wanted to apply his notions also to the breakdown of the early 1930s. In part, it was much like the 1890s in some respects — people were just hunting around for any excuse to devalue currencies, and would grab whatever was at hand, no matter how silly.

Actually, my conclusion — that there was no great monetary disaster, at least before the big currency devaluations — was the standard opinion until about 1960, and remains a dominant opinion to the present time. So, I am not exactly an outlier here.