This week we will look at a funny and little-known episode in the history of the U.S. dollar and Federal Reserve, notably the wartime years of WWI and the Recession of 1920 that immediately followed.

The Federal Reserve was, of course, signed into law in 1913, just in time for WWI. There was something of a liquidity crisis upon the outbreak of war, but that was handled by the existing “bank clearinghouse system” which was legitimized by the Aldrich-Vreeland Act of 1908. The Federal Reserve system had not yet been set up, and was not operational.

The U.S. entered the war in April 1917. This coincided with the time when the Federal Reserve banks became operational. Virtually from day one, the Fed was pressured into “keeping interest rates low” for the flood of government borrowing that was happening to finance the war. Here’s how Richard Timberlake describes it, in his wonderful and essential book Monetary Policy in the United States: an Intellectual and Political History:

The Federal Reserve banks were just about operational when the United States became involved in World War I. Almost immediately, the U.S. Treasury Department asserted its dominance. The discount policy of the Board was to maintain rates “in harmony with the low interest rates borne by the Government loans,” stated the Board’s annual report for 1917. Even more pointed was a section in the annual report for 1918, … which began: “The discount policy of the Board has necessarily been coordinated . . . the Treasury requirements and policies, which in turn have been governed by demands made upon the Treasury for war purposes.” Again, in 1918 the annual report admitted that discount rates were based upon rates currently borne by government securities, and “must for the time being continue to be fixed with regard to Treasury requirements.” The Board “recognized its duty to cooperate unreservedly with the Government to provide funds needed for war.”

The report for 1919 excused the Fed’s subservience to the Treasury by asserting that no higher rate structure would have been sufficient to persuade the securities market to absorb the Treasury issues: “It was necessary to cooperate with the Treasury in every way,” the report claimed, “to facilitate first the sale of Government securities and then their absorbtion by investors.”

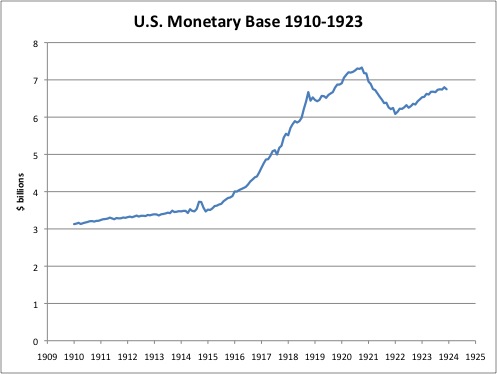

As you might imagine, this involved printing money. Here’s what happened to the monetary base in the U.S. during that time. This data is from Milton Friedman’s Monetary History of the United States, 1867-1960:

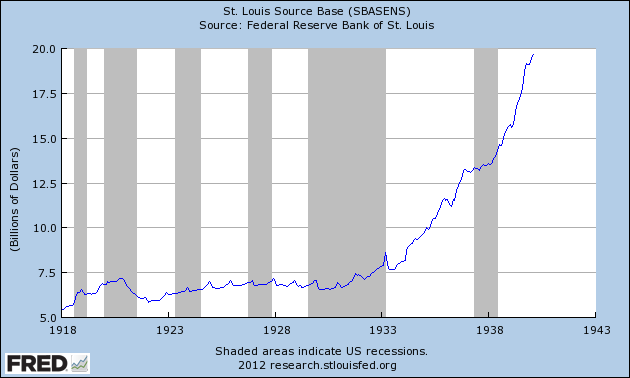

Here’s what it looks like when we continue the series into 1940. This data is from the St. Louis Fed:

There are a couple interesting things on this chart. For one, hardly anything at all happens during the 1920s, despite the booming economy. As the Great Depression begins at the end of 1929, the monetary base begins to expand by quite a bit. This is what you’d expect to see, as banks would be under pressure of withdrawals and holding paper banknotes was probably becoming more popular. The “money supply shrank” stories you’ve heard are fiction — they represent M2, which is mostly bank deposits, not base money.

Getting back to our original story …

During the wartime years, there is an embargo on gold in the U.S., so nobody can buy, sell or export gold. The Bank of England had effectively suspended redeemability of its banknotes into gold in August 1914, rendering the British pound a floating currency. The pound was also printed to finance the British government’s war effort. At the beginning of the war in 1914, the estimated pound base money supply was around £200 million, according to the book Sterling: the History of a Currency. By mid-1919, the pound base money supply had expanded to around £550 million.

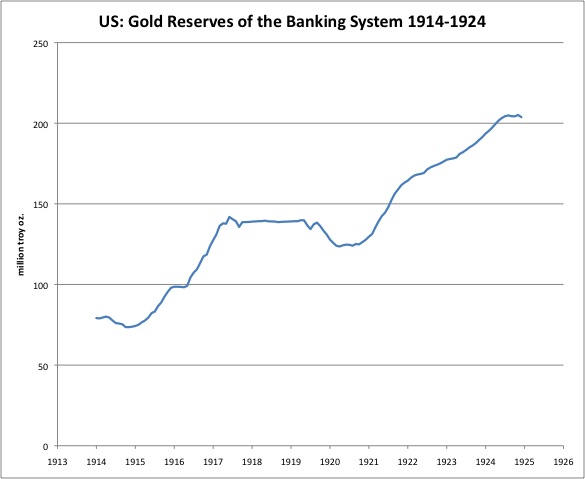

Here is a graph of the gold bullion reserves of U.S. banks:

We can see bullion reserves rise in the beginning. I interpret this as a rush of European interest in holding dollars and dollar assets, as their governments were all at war with each other. Then, there is an odd flatline around mid-1917-mid 1919, and a brief decline. The flatline is probably the gold embargo period.

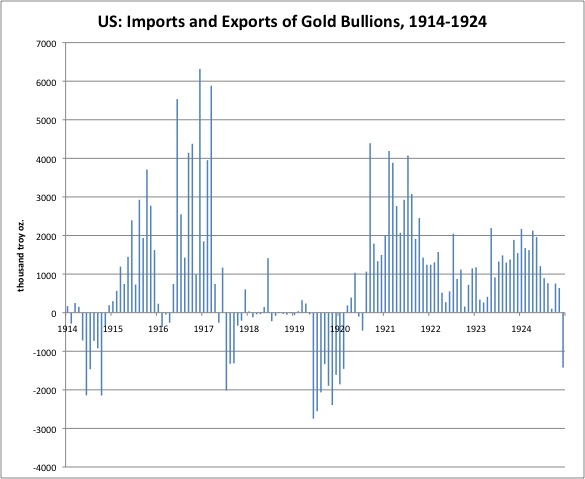

Here’s a graph of U.S. gold imports and exports. Negative denotes an export.

We see a brief outflow at the outbreak of war in Europe, then an inflow, which once again suggests Europeans rushing to hold dollars. This switches to an outflow in mid-1917 and goes negative. Probably, redemptions of banknotes for gold are happening here. From mid-1918 to mid-1919, there’s a flatline, which is probably the embargo on exports of gold. When the embargo is lifted after the end of the war, there’s a big gold outflow. The Fed and banks react by shrinking the monetary base (above), which turns the outflow to an inflow. The source for all these is the Fed’s Banking and Monetary Statistics, conveniently available at the St. Louis Fed FRASER archive. (I’m making the sources clear so you are able to make graphs like these yourself if you want.)

So, basically what happened is the Fed was pressured by the Treasury into facilitating the funding of the war effort, which involved printing too much money. This led to gold redemptions, which were stopped by government edict. After the war, there was a big rush of gold redemptions, signalling that the dollar was much too weak compared to its gold parity. The Fed and the banks (the Fed was not yet the monopoly issuer of currency then) reacted by shrinking the monetary base.

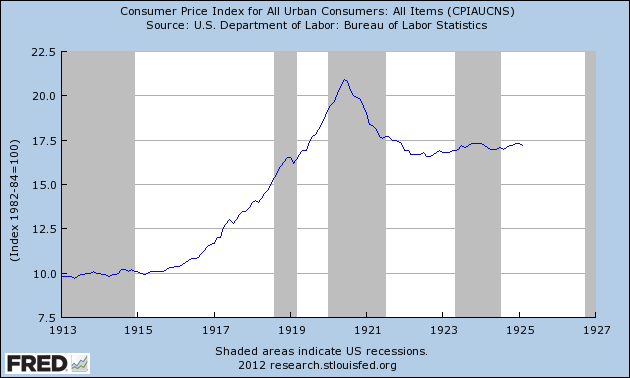

The combination of the demobilization of soldiers, the decrease in war-related demand for goods, and the monetary deflation resulted in the recession of 1920, in which prices fell considerably. This graph is titled “Consumer Price Index,” but I think it is really the Bureau of Labor Statistics Wholesale Price Index, which is more of a broad commodity index, and not really comparable to the CPI which wasn’t compiled until 1940. However, this index still stabilizes at a much higher level than before the war began. (The BLS WPI began to be compiled in 1919, but data was gathered back to 1913, which is exactly when this time series starts.)

There are a few more things to say about this time period, but I think I will save that for later.