Thoughts on Greece

May 2, 2010

This Greece situation is turning into a good way to talk about a number of related ideas. I thought I’d put them all together in one place.

What should a statesman do in such a situation? What are the options and possibilities? The present Greek government leadership was elected in October 2009. It later revealed that the Greek government budget deficit was much larger than the previous government reported (due to some Goldman Sachs-assisted prevarication), thus starting off the crisis.

A baseline solution: My basic solution would be to stay within the eurozone, and just default. Blame it on past governments. Then, reduce government spending dramatically. This is mandatory anyway because without the ability to issue debt, the government won’t have any money in its checking account. It’s amazing how much a government’s spending can decline when it doesn’t have any money. Let’s call it a good thing! This is a great time to dump all sorts of parasitic hangers-on, from pork spending to the oligarchs who have been sucking the Greek government for vastly bloated contracts, to the excessive number of public employees. Dump them all in one go, quickly and cleanly. Indeed, there will hardly be any other option due to cash constraints.

This step would have mixed political results. Obviously, government workers and the oligarchs would complain, but many other people would be happy to see the mess in Athens finally being cleaned up.

The next step would be to implement a dramatic tax reform. I would consider just keeping the existing 19% VAT. It was raised to 21% in March, but lower it again back to 19%. Then, eliminate all other taxes, and declare a tax amnesty for any previous tax evasion.

This is not so much different from the flat-tax systems implemented throughout eastern Europe, to great success. Following Estonia in 1993 and Russia in 2000, we now have Bulgaria, Albania, Czech Republic, Georgia, Kazakhstan, Kyrgyzstan, Lativa, Lithuania, Macedonia, Montenegro, Romania, Serbia, Slovakia and Ukraine.

Would a VAT-only system be better than a flat-tax type system, as has been implemented in many other countries in Eastern Europe? Personally, I like the slight “progressive” character of the flat-tax system, but it would be interesting to give the VAT-only system a try. I can pretty much guarantee that the results would be good. Also, it helps to make friends with the oligarch-types, who might be miffed since they are no longer able to bleed the Greek government for endless billions.

Admittedly, I am influenced simply by curiosity. After many flat-tax examples, we should have some VAT-only examples just to see what would happen. If they didn’t like the results, they can change it later. In any case, it would be much better than what they have now.

A big tax reform like that would also be quite popular.

Thus, Greece would be left, after the default, with: a) a vastly slimmed-down government; b) a stable currency (euro); c) the most growth-friendly tax system in Europe; d) massive unemployment.

The unemployment is a given in any case. It would result from the huge reduction in government spending (about 10% of GDP) caused by the lack of capital markets access. If the Greek government defaulted, then withdrew from the eurozone and issued its own currency, and then raised its already-high taxes — in other words the standard IMF playbook that many others recommend — the result would be even worse unemployment and a moribund economy.

The difference here is that we now have a very pro-growth framework, which invites capital to create opportunities to put those unemployed to work in productive new jobs. Most “economic growth” is actually a process of unemployment. Most people used to be farmers. As farming productivity increased, there was a steady reduction in farming employment, freeing up resources to provide new goods and services. If you had two people farming, and then farming productivity doubled, you would have one farmer and one person providing some other service, like a hotelier for example. Thus, the production of the economy increases.

Thus, we could look upon the great numbers of people being released from unproductive government jobs as a great resource for future growth. This growth would never happen if the environment is one of high taxes and unstable money. But, it would happen in our scenario of low taxes and stable money. Those people would be employed in the production of new goods and services. This creates greater wealth, greater GDP, and of course greater tax revenue.

A stable euro: The Magic Formula is:

Stable Money

Obviously, the above 19% VAT-only system takes care of the low taxes component. The stable money is provided by the euro. This presumes that the euro is stable. It has been much more stable than the alternatives, such as the independent drachma or many other options. However, the euro management (ECB) is, alas, incompetent. They don’t really understand how to manage a currency correctly. If they did, this minor Greek government default would be no problem. Why should the value of the euro decline just because someone missed some payments? Who cares? If the value of the euro did have a sagging tendency, the ECB would simply reduce the supply of euro base money by selling bonds on the open market and making the cash received in payment disappear. What happens in these situations, normally, is that there is some event — it happens to be the Greece situation but it could be anything — and the currency sags in value. The ECB is plainly worried about the situation but does nothing effective to counteract it, such as reducing base money in “unsterilized intervention.” This is a big tell: the ECB isn’t doing anything effective because it doesn’t know how. Now we have two currency negatives: first, the original condition, and second, the fact that the ECB obviously doesn’t know what it is doing. This causes the currency to fall further, and then we are on the way to a currency crisis.

This incompetence by the ECB is driving the policymaking process towards bailout. Nobody wants a currency crisis. They think that if Greece’s government can avoid default by way of some IMF-led lending program, then a currency crisis can be averted, supposedly. But, it would be much better if the ECB just knew what it was doing, and then they would avoid a currency crisis whether or not Greece’s government defaulted.

February 14, 2010: The Problem with Greece

Bailing out the banks: What’s really going on here? There is about 300 billion euros of Greek government debt. Who owns it? Mostly banks, and other financial institutions like insurance companies, pension funds and the like. The pressure for bailout is growing because these entities — not the government — want to get bailed out.

Let’s say you own 50 billion euros of six-month Greek debt. Greece doesn’t have the money to pay you. It can’t get the money by issuing new debt. When an entity doesn’t have the money to pay you, what happens? Guess what — you don’t get paid. However, if Greece is able to borrow from the IMF etc., then you would get 100% of your money back. It’s just like AIG and Goldman Sachs. AIG had some committments to GS, but it didn’t have the money to pay. What was supposed to happen is that GS wouldn’t get paid. The government’s “bailout” of AIG was really a bailout of AIG’s creditors, namely Goldman Sachs.

Look at it from the Greek government’s perspective. Before, it owed 50 billion euros to some banks. Afterward, it owes 50 billion to the IMF. Not much of a change there. But look at it from the banks’ perspective: before, they had a 50 billion euro loan that they weren’t going to be paid back on. Afterwards, they have 100% of their money. Big difference. So who is really getting bailed out here?

In a rather amazing scam, it appears that forthcoming IMF etc. loans to the Greek government could be made subordinate to existing debtors. Eh? This is completely the opposite of normal procedure for distressed/bankrupt debtors, where the latest loans are made senior to existing creditors. It’s another bank bailout! For example, let’s say that there is 300 billion euros of Greek government debt out there. The IMF deal might be for 125 billion euros for the first three years or so, to allow the Greek goverment to roll over maturing debt. That’s great for the bankers who own the 125 billion euros of maturing debt. They get paid off. But what about the bankers who own the remaining 175 billion of debt? A year from now, they might be facing default once again, just as they are now. And, the price of the bonds will reflect that risk of future default. They would trade at a discount. However, what if the IMF loans were subordinate? The fateful day comes three years from now. The IMF now has loans of 125 billion euros to the Greek government, and the bankers have 175 billion. The government defaults. Probably the next thing that would happen is that there would be a restructuring, so the government agrees to pay 70% of the principal value. Now the value of the Greek government debt falls from 300 billion euros total to 300*70% or 210 billion euros. Normally, everyone would take a 30% “haircut”. This is 90 billion euros. However, if the IMF is subordinate, then the IMF would take all of the 90 billion euro loss. Since the IMF’s portion is 125 billion, the IMF would absorb the whole loss, and the bankers would get 100%! The most important part is that this would be reflected in the price of debt in the market today. People could do the calcuation, and compute that the probability of the existing debt taking a loss is low, because the IMF is subordinate. So, the senior debt would trade for a high price. Thus, the bankers could sell their Greek government debt today at a high price. They don’t have to wait years.

Zerohedge: Greek (Inverse) DIP Update: Bailout Loans To Be Junior To Existing Claims

“Bankruptcy” and “failure.” “Greece” — the country — isn’t going to “fail.” Short of military invasion, it isn’t going anywhere. Even the central government will probably survive (depends on politics), and continue its oprations, despite missing some loan payments. These terms that get tossed around are ridiculous. “Default” is the term used when a debtor does not abide by the committments of the loan contract. Typically this means missing a payment, but there are also varieties of “technical default” such as breaking a loan covenant like misuse of funds or exceeding some ratio like debt/assets, collateral coverage, or many other things. “Bankruptcy” is the term for the legal process that ensues after a default. What legal process ensues for a sovereign government? Not much of anything, really. Nobody is going to seize the assets of a sovereign government. The government continues to exist and operate. The main difference is that, having failed to make the payments, lenders are less likely to loan money to that government in the future. So, the big change for Greece is that it would no longer be able to run a budget deficit. That might be a good thing.

The government is not the country: We always hear that “Greece” is doing this and “Greece” is doing that. I usually try to use the terminology “the government of Greece.” Greece is a country with 50,944 square miles of land and about ten million inhabitants. It is home to many millions of businesses and households, but Greece is not itself an economic entity. “Greece” — the entire country — does not have assets or liabilities, revenues or expenses. Within Greece are many government entities. There are city governments, county or prefectural governments, independent government “authorities” like a public transit system or a water district, school districts and maybe state-run universities. Possibly public hospitals or even a public museum. All these government entities have their own balance sheets, revenues and expenses. Among these dozens if not hundreds and thousands of government-type entities is the central government. The central government is an organization with certain revenues and expenses, assets and liabilities. It has a certain number of employees and so forth. Although the central government might be the largest single economic entity in the country — more employees, more revenue and so forth — it is relatively small compared to the sum total of all the economic activities and entities in Greece, the country. So maybe this one entity, the central government, doesn’t pay back the bankers on some of its debt. Who cares? If the Greek central government defaulted, that doesn’t mean that the Athens public bus authority defaulted, or the Mykonos public school system has a problem. Let’s say you are an olive grower. You have plenty of cash to pay your debts, which are of course euro-denominated debts. So Tweedledee and Tweedledum in Athens are having a little crisis. This is no problem of yours. Nor do Greek households go into foreclosure on their mortgages.

Unfortunately, the egotism and incompetence of typical central government bureaucrats is such that they like to take everyone down with them. Thus the tax hikes, asset stripping, currency devaluations, and so forth.

The madness of the devaluationists: The Mercantilist economists, now known as the Keynesians, have two basic solutions to every economic difficulty: government spending and currency devaluation, or at least some variant of an “easy money” policy whether “lowering interest rates” or “quantitative easing” or some monetarist construct or whatever. Obviously, with the Greek government already running an enormous deficit and facing default, more government spending is off the table. Thus, they are restricted only to currency devaluation. Today, they are absolutely frothing at the mouth with different variations on currency devaluation.

Don’t you think this is a little odd? For one thing, Greece doesn’t even have a currency. It is part of the eurozone. This is why the Keynesians are apoplectic with their hysteric arguments about why Greece should have its own currency, why the eurozone doesn’t work and is doomed to failure, how everything could be solved if only Greece “had their own printing press,” and so on and so forth.

Here’s FT columnist Samuel Britten for example:

http://www.ft.com/cms/s/0/f11a4dda-1cc9-11df-8d8e-00144feab49a.html

Second, it should be obvious to even the layperson observer that this is definitely not a currency problem. This problem stems from the government’s long history of huge deficits, and the debt resulting from that policy. Obviously the solution must involve reducing government spending. How could a currency devaluation/easy money possibly resolve this? It’s inane.

January 27, 2008: Crisis Management

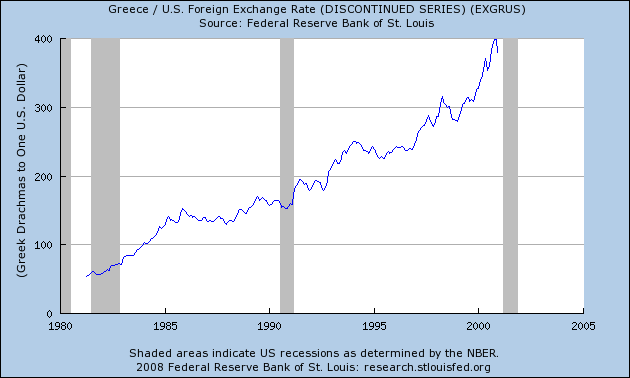

Here’s a history of the Greek drachma before the euro was adopted:

Actually, Greece had a long history of currency devaluation before entering the eurozone. So, if you want to understand the effects of currency devaluation, just ask a Greek person. We see here that the drachma went from about 50/dollar to 400/dollar, or about an 8:1 devaluation during the 1980s and 1990s. That is a lot. Prices of things would rise by 8x, which works out to 11% annual inflation, on top of inflation left over from the 1970s, which ran in the 4%-6% range in the U.S.

If your country has a history of this kind of chronic currency devaluation, why would anyone want to own debt denominated in this currency? A few speculators might try it, as the interest rate might be attractive for the short term. And, it might be useful for some domestic entities as a short-term “money market” type asset. Thus, interest in the debt tends to be low and the yield curve is short, typically under two years.

That’s why governments of countries with a history of poor currency management typically can’t issue large amounts of debt denominated in that currency. All the devaluationist types are screaming that “Greece needs to issue debt in its own currency, so that it could make the payments by running the printing press.” Guess what — nobody would buy this debt, including Greeks themselves. Greeks aren’t forced to buy this crap just because they happen to live in Greece.

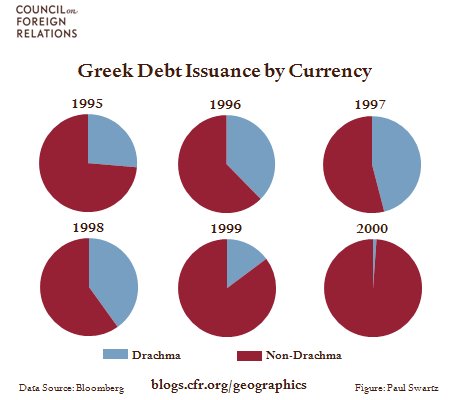

That’s why, before joining the eurozone, most of the Greek government’s debt was denominated in foreign currencies:

In the bad old days, in 1995, only about 25% of the debt was denominated in drachma. This is not because the Greek government didn’t want to issue debt in drachma. They would love to! The problem was that nobody would buy it.

This is true of most other governments too, especially those in Latin America, which have a long history of currency abuse.

This is pretty simple stuff. Even an economic novice should be able to understand what I’m talking about here. However, the madness of the devaluationists is everywhere these days. The Keynesian nutjobs are thick and heavy at the IMF. The typical IMF response to a government that defaulted on its foreign currency debt is an intentional devaluation. What does this accomplish? The government’s revenues are in local currency. If you devalue the currency, then it takes more and more local currency to buy the foreign currency. Thus, the government’s ability (and ultimately the taxpayers’ ability) to pay the foreign currency debt declines. You would think this couldn’t be more obvious. However, the Keynesian nutjobs are, as I mentioned, in a bind here. They can’t rely on government spending, and they only have one other trick. They try to solve the problem with currency devaluation, because in their minds it is an all-purpose generic solution for everything.

“Currency union requires political union:” This is baloney. If the ECB knew what they were doing — able to adjust the supply of money appropriately — then all the governments of Europe could default, and it would have no effect on the value of the euro. Remember, a “default” just means they didn’t make some payments. So what. There are another 23 countries using currencies pegged to the euro. About 70% of all the U.S. dollars in circulation are used outside of the U.S. Does that mean the dollar doesn’t work unless there is a political union with the whole world? The only thing a currency needs to be is stable. Traditionally, this means pegged to gold. All that you need to maintain stability is to properly adjust the supply of base money, to accomodate changes in demand for the currency. Read that last sentence again. There’s no need for political union, or budget deficit agreements, or whatever.

The euro was a good idea. Unfortunately. the bureaucratic class of Europe doesn’t have the talent base to properly manage the euro, or to deal with problems that pop up like this Greece affair. These are easy problems to solve, but only if you know how to solve them. If you don’t know how to solve them, they are insoluble.

“Uncompetitive.” Obviously, Greece had a long history of currency devaluation before joining the euro. This tends to keep wages low — lower than they should be — because the money that workers get paid in continuously falls in value, and also because economies just don’t work well under those conditions. After Greece joined the eurozone — and enjoyed the benefits of a stable currency — workers’ salaries naturally increased from their devaluation-depressed levels. This is now supposed to be a big problem, when it is actually one of the big benefits of a stable currency. We often see these arguments in the early stages of a stable currency after a long period of devaluation. In an environment of devaluation, the businesses which benefit most from devaluation — those which use cheap labor to produce some sort of exportable good or service — are the ones that thrive. Consequently, they also become more politically influential, and start to complain that the stable currency and rising wages are blowing up their cheap-labor-based business plan. In Greece, one of the main “cheap labor exportable” industries has been tourism. After a while with a stable currency, the industries that benefit from a stable currency — most of them — recover and offer a political counterbalance to the devaluation-obsessed cheap-labor-export group. In the case of Greece, it appears that these arguments are coming mostly from the Keynesians, who feel lost at sea without the ability to devalue the currency.

“Spending cuts and inevitable tax hikes:” The latest plan involves an increase in the VAT of about 3-4 percentage points. This is on top of a two percentage point rise in the VAT in March, to 21%. This never works. Tax evasion in Greece is already at high levels. This is because Greek people have already concluded that they are paying too much taxes. What happens when you ask them to pay more? They already aren’t paying it, so they just continue on in that fashion. Indeed, the legitimacy of the existing tax code just declines that much further, and the tax evaders look like the smart guys. I bet the government’s tax revenue/GDP declines as a result of this. Does anyone think that Greece’s problems arose because taxes were too low? This can actually happen sometimes. Sometimes, people want more government services, and are willing to pay for them with taxes. This almost never happens today, but was common around the end of the 19th century when governments started to provide basic services like universal education. Obviously, the solution for Greece is spending cuts without tax hikes — just as it is for California and many other bloated governments whose bloodsucking habits have reached their natural conclusion. I would go for a full tax reform in Greece.