We have been discussing the Balance of Payments, or one aspect of it, the Current Account deficit (or surplus), in the context of Economic Nationalism.

The easiest way to understand the Balance of Payments is to look at the Balance of Payments of an individual, or an individual household.

October 27, 2024: Economic Nationalism: The Current Account Deficit

It might seem at first that this is a sort of analogy, or metaphor. But, it is not. This is the actual Balance of Payments of an actual economic entity, in this case an individual or household. There are other kinds of economic entities, primarily businesses or government entities, whether the Federal Government or the local public library. Basically an “economic entity” has a bank account, buys and sells, makes and receives payments, holds assets or engages in liabilities.

The Balance of Payments on the “national” level is actually the aggregate of these individual entities. There is no “national balance of payments,” except perhaps in the case of the Soviet Union where it really was the central government that engaged in all external trade. The “national balance of payments” is simply the aggregate of the individuals that are categorized as having that “nationality.” The “United States” does not sell automobiles. The Ford Motor Company sells automobiles. “China” does not buy US Treasury bonds (except perhaps the central bank). Chinese entities buy US Treasury bonds.

So it is perfectly normal to use the example of a household, because this is the reality of trade, rather than the abstraction of statistical aggregates. You could create another statistical aggregate, of blue-eyed left-handed Catholics; and they would also have an aggregate Balance of Payments, equally legitimate (although less useful) than the official statistics for the national level.

We saw that the Current Accounts would be “balanced” if income matched expenditure; or, if the “exports” (wage income) of the individual matched its “imports” (purchases of goods and services). There would be a “current account surplus” if there was less spending than income. This is savings — in particular, financial savings. You could argue that buying the 10lb bag of coffee at Costco is a kind of “savings,” because you are increasing your inventory of coffee, an asset. You could also buy a piece of land. These are legitimate forms of savings, but we are, for now, particularly interested in “financial savings,” or the acquisition of some financial asset, at first a bank deposit balance, which can be traded later for some other financial contract, a stock or bond. There would be a “current account deficit” if there was more spending than income. This would require either selling assets, or issuing liabilities of some sort, typically debt or equity. Thus, the “current account” would be matched, inevitably, by the “financial account.” “Savings” — at least, financial savings — requires the acquisition of some financial asset; a stock or bond, or at least a bank deposit. Asset sales or creation of liabilities (typically borrowing money) arise naturally from a “current account deficit,” since obviously you can’t spend more than your income unless you acquire that extra cash by some means.

There is sometimes some debate about whether a “current account surplus” arises from the “exporting and importing” side (Current Account) or the “savings” side (Financial Account). We should see that they are two aspects of the same act. Our individual “exports” labor and gets paid, and then “imports” things that are purchased, leaving some residual, or “savings.” There is a current account surplus. Maybe the individual gets a promotion and then gets paid more money. Maybe the individual’s expenditures do not rise as much as his income, and therefore savings rises, an “increase in the current account surplus” for the individual, and an “increase in the current account deficit” for the Rest of the World. Did this current account surplus, or “trade imbalance,” arise because the person got paid more, or because he saved some of his additional income? Obviously it is both; the increased savings required both the increased income, and also, the decision not to spend the extra income. Today, the international price of oil rises, and the revenues of Saudi Aramco increase. Some of this increased revenue goes into the purchase of Treasury bonds, increasing Saudi Arabia’s “current account surplus” with the Rest of the World and increasing the Rest of the World’s “current account deficit” with Saudi Arabia. Was this because of the higher price of oil, or because of “savings” in the form of the acquisition of Treasury bonds, instead of the acquisition of Ferraris and Veuve-Clicquot?

Quite often, a country runs a persistent current account deficit, because it is a good place to invest. The Rest of the World wishes to acquire equity and debt, because of all the good business opportunities that will make that equity and debt a good investment. The United States ran a persistent current account deficit throughout the nineteenth century.

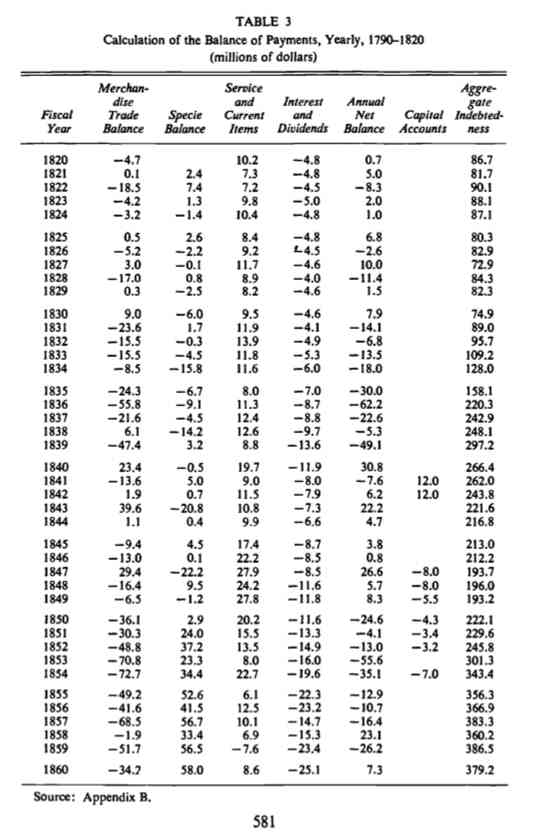

September 8, 2011: U.S. Balance of Payments During the 19th Century

This was not a bad thing. All that foreign capital and foreign investment helped make America wealthy.

Today, however, one reason for the large Current Account Deficit of the United States is not healthy investment, but a combination of two factors:

- Low domestic savings. Not enough capital creation/savings/investment.

- Large government deficits, financed through bond issuance. This consumes the small supply of domestically-generated capital, and results in government indebtedness to foreigners.

These are genuinely bad things, and their symptoms are evident in the Balance of Payments as a Current Account Deficit.

We will talk more about this topic soon. In general, I am taking the path of discussing a number of minor issues, to clear the table for a discussion of what I consider the heart of the discussion about Economic Nationalism. Otherwise, we would be constantly distracted by these minor issues.