(This item originally appeared at Forbes.com on November 4, 2022.)

In the past couple years, we had a gigantic debate about “inflation,” where anything and everything was discussed, without a lot of resolution. The only thing that seems to have been decided on was: Whatever the cause of “inflation,” the solution has something to do with the interest rate target of the Federal Reserve.

Why is this? As we were planning our recent book Inflation: What It Is, Why It’s Bad, and How To Fix It, we kinda knew this was going to happen. That’s why, on the cover of the book where people would notice, we suggested that common interpretations of “what it is” and “how to fix it” were wrong, or at least unproductive, and that there were better solutions — solutions that are not just our creative notions (too many of those these days), but things we actually did in the US over a period of centuries, and they worked.

It’s an easy book to read, but to make it even easier, here it is:

The word “inflation” indicates a vague hodgepodge of notions having something to do with rising prices. We separate all the various things that might influence prices into two basic categories: Monetary Influences (basically the central bank, or the currency), and Non-Monetary Influences (everything else besides the central bank). This is no great insight, but nevertheless, it is something that most people ignore. Today, the basic thought process is that there’s a Consumer Price Index which is X, and if this X is in excess of the Federal Reserve’s stated target (now 2%), then the Federal Reserve should address this with Higher Interest Rates.

It’s true that, during the 1970s, “inflation” was almost entirely due to monetary causes. In March 1980, the Consumer Price Index was up 14.75% from a year earlier, the worst this indicator got during that period. However, in March 1947, as price controls were lifted and the economy adjusted away from armaments and back to consumer goods, this indicator hit a peak of +19.7%. This was mostly nonmonetary in nature. The 10yr Treasury yield that month was 2.19%.

The monetary sort of “inflation” is best understood as: A decline in the value of the currency, and the consequences of that decline. This is an ancient notion: Governments were debasing their coins — reducing their precious metals content, which would effectively reduce their market value — as far back as the seventh century BC. Guess what: As the coins lost value, it soon took more coins to buy things. Rome engaged in chronic coinage debasement during its long decline in the second through fifth centuries. By one account, the price of wheat in Roman denarius rose two million times higher. This was many centuries before the use of paper money.

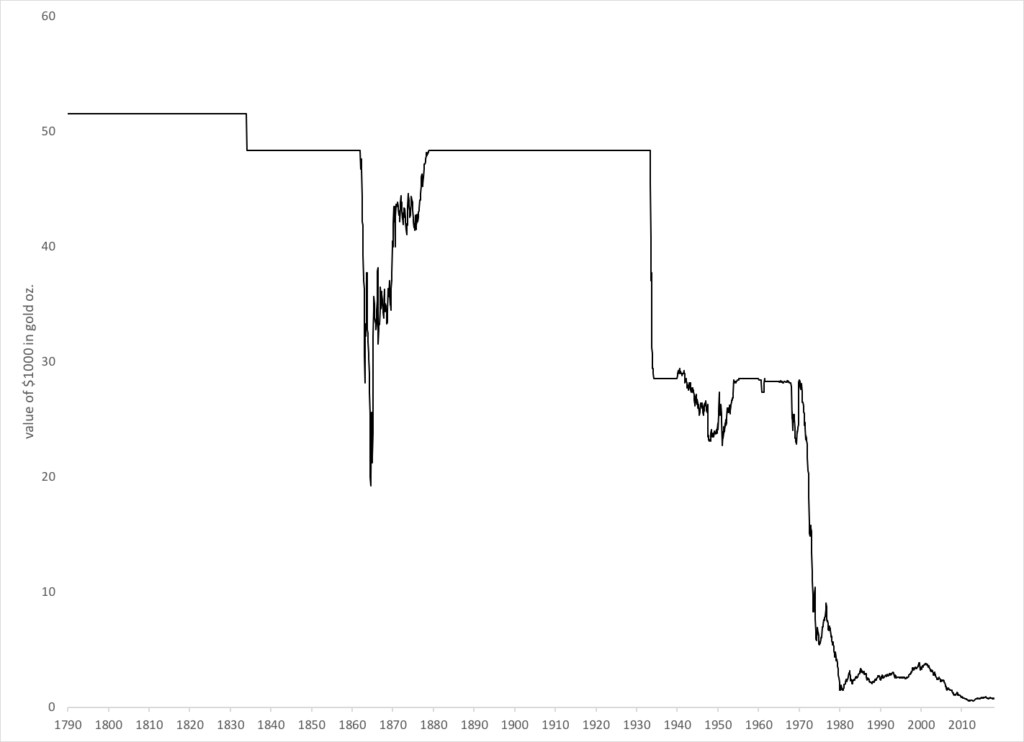

For many centuries, gold has been the best indicator of stable money value. That’s why all the world’s major currencies were linked to gold, as recently as the 1960s. Since the US left the gold standard in 1971, the value of the USD has fallen such that it now takes about fifty times more dollars to buy an ounce of gold than it did then. Recently, the value of the USD vs. gold went from about $1200/oz. in 2019 to about $1800/oz. in 2020-2022. It now takes 50% more dollars to buy an ounce of gold. It looks like the USD has fallen in value, again, which is no surprise considering how aggressive central banks were in 2020. We should expect that, over time, markets will adjust so that it will also take about 50% more dollars to buy everything else as well (i.e., prices go up about 50%) — just like Rome in the third century. We have done this many, many times and nobody should be confused about it.

But today, we never hear about this. Have you heard anyone mention that the value of the USD, or other currencies, has fallen by XX% (whatever your estimate may be), and that this has inflationary consequences? I haven’t. We hear about every other conceivable thing, but that. If the problem is falling currency value, then the obvious solution is: Don’t Do That. At the very least, keep the currency from falling further in value. Maybe, allow it to rise somewhat, to correct past error. In fact, this is what the Federal Reserve has done. (I think they are smarter about this than they let on.)

The whole point of the gold standard is that it would keep the currency from falling in value (or rising in value). And for nearly two centuries, 1789-1971, as long as the US stuck with this principle, there was never an inflation problem. Stable Money works.

Now, what does this have to do with interest rates? Does managing interest rates keep the value of the currency stable? The places with the highest interest rates often have the worst currencies.

In the past, the Federal Reserve’s interest rate policy was tied somewhat to money creation. To maintain lower interest rates, the Federal Reserve would create more money. This could cause a further decline in currency value, and would thus be inflationary. The actual relationship was rather chaotic, but that was a common pattern. So, raising the interest rate target might (hopefully) lead to less money creation, and thus keep the currency from falling further. It made a little sense, although it was always easier just to manage the value of the currency directly, and forget about interest rates.

However, today we have an interest rate mechanism, the Interest on Reserve Balances, that did not exist before 2008. The old pre-2008 Fed Funds Rate target is gone and, in today’s high-reserve system, won’t be coming back — which is fine, because that was also a pretty crappy system. When the Federal Reserve “raises” or “lowers” interest rates today, it is doing something different than what the Fed did in the past. This Interest on Reserve Balances actually has no direct relation to money creation; and thus, no obvious direct relationship with currency value. It is just set by decree.

In a proper monetary system, we would have something completely different:

1) The currency’s value would be kept stable — most likely, as more than half of all countries do today, by linking its value with some external standard of value. Gold has always been the best standard of stable monetary value. Since “monetary inflation” is simply a decline in currency value, then if you keep the value of the currency from declining, then there will be no more monetary inflation problems. Prices may still go up and down due to all kinds of nonmonetary factors.

2) Interest rates are left to the free market. Yes, you can do that. Wall Street can figure out for itself a reasonable price to pay for 91-day Treasury paper. This was the normal course of events before the Federal Reserve’s creation in 1913. The Federal Reserve, or other central bank, could still engage in nineteenth-century-style “lender of last resort” activities, which was completely compatible with the gold standard. This was, in fact, the original purpose of the Fed’s creation. Or, you could use the system of Canada during that same time, where individual banks could serve this role, without the need for a central bank.

In any case, the solution is: Stable Money, and a free market for interest rates without Federal Reserve manipulation.

Normally, when a currency is perceived as highly reliable — as gold standard currencies always were — interest rates fall to low levels.

We are, today, really far down the rabbit hole of central bank currency and interest rate manipulation. But, everyone should understand what the proper alternative is. We did it for nearly two centuries, before 1971, and became the wealthiest country in the history of the world.