We were recently talking about M2, and how it is basically a measure of the banking system.

April 27, 2025: Understanding Money Mechanics #6: Blame M2

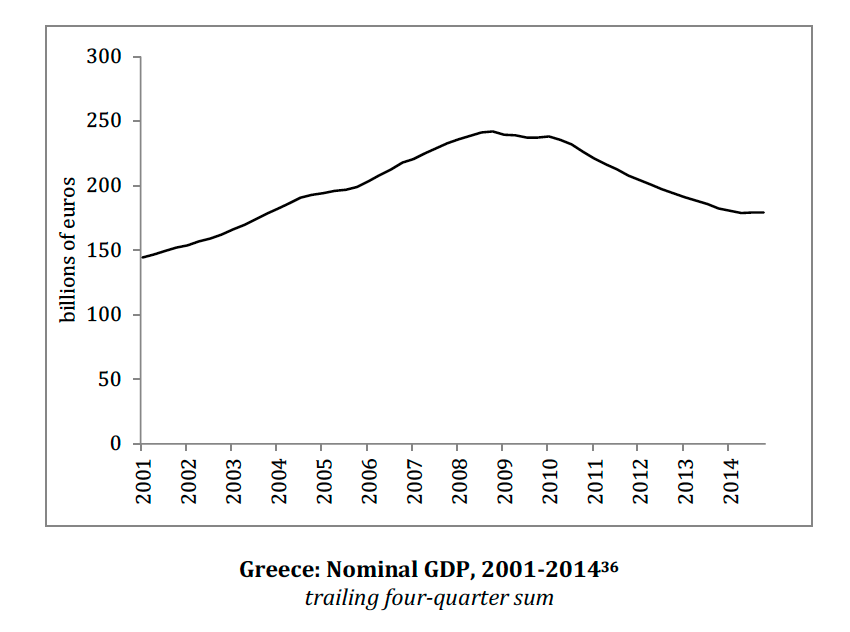

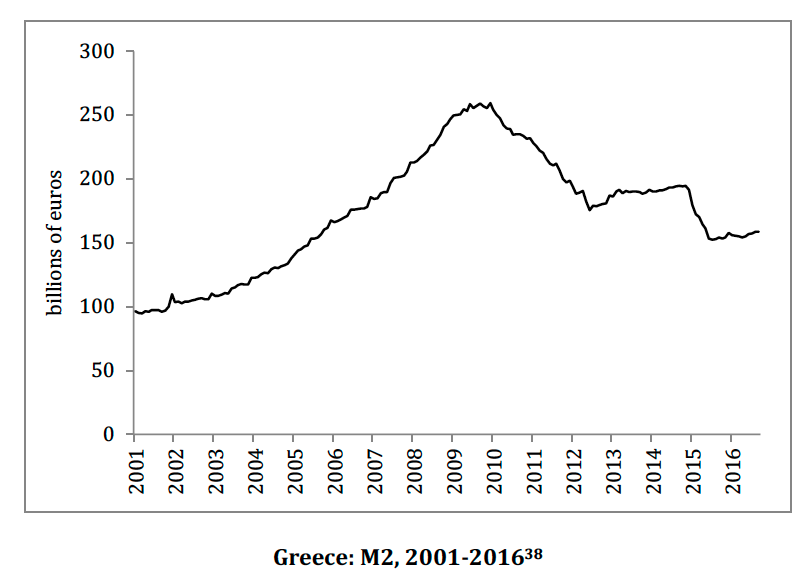

We would expect the banking system to, more or less, follow the progress of Nominal GDP as a whole. And indeed this is what we see. We looked at the recent example of Greece:

Greece had some serious economic difficulties during this time. However, it didn’t have much of anything to do with the money. Greece shared the euro currency, with Germany, France and the other members of the Eurozone. The other euro users didn’t really have much problem, so we can see that this was not a monetary problem with the euro. It was a problem, basically, of bad economic policy.

All of this focus on “M2,” which is basically just a correlate of Nominal GDP (with “third generation” Monetarists now just focusing on NGDP directly, or NGDP Targeting), adds up to an excuse to apply some kind of monetary “stimulus,” in response to non-monetary problems caused by other factors. This we saw during this time in Greece, as many economists wanted to “stimulate” the Greek economy through some kind of “easy money” solution. To facilitate this, they wanted Greece to leave the eurozone and basically introduce a domestic floating currency, whose value would promptly fall. Usually, these arguments are not for devaluation explicitly. They focus on other matters, such as “M2.” However, significant currency depreciation is the expected result; and indeed, these methods wouldn’t work without it. If they could work without it, you could just do it without leaving the euro (or, Gold Standard in the 1930s).

From this recent Greece example, we can then extend to the Great Depression period, when exactly the same arguments were made for exactly the same reasons. This of course includes Milton Friedman, and his “Monetarist Interpretation” of the Great Depression in the 1960s, but also, a number of economists of the 1930s as well.

Today, we will look at the “Austrian definition of the Money Supply,” which, I argue, arises from the confusion and admixture of Money and Credit that goes back at least to the Theory of Money and Credit of 1912; and probably well before that.

Here, Louis Spadaro begins with:

I. The Definition of the Supply of Money

The concept of the supply of money plays a vitally important role, in differing ways, in both the Austrian and the Chicago schools of economics. Yet, neither school has defined the concept in a full or satisfactory manner; as a result, we are never sure to which of the numerous alternative definitions of the money supply either school is referring.

The Chicago school definition is hopeless from the start. For, in a question-begging attempt to reach the conclusion that the money supply is the major determinant of national income, and to reach it by statistical rather than theoretical means, the Chicago school defines the money supply as that entity which correlates most closely with national income. This is one of the most flagrant examples of the Chicagoite desire to avoid essentialist concepts, and to “test” theory by statistical correlation; with the result that the supply of money is not really defined at all. Furthermore, the approach overlooks the fact that statistical correlation cannot establish causal connections; this can only be done by a genuine theory that works with definable and defined concepts.1

In Austrian economics, Ludwig von Mises set forth the essentials of the concept of the money supply in his Theory of Money and Credit, but no Austrian has developed the concept since then, and unsettled questions remain (e.g., are savings deposits properly to be included in the money supply?). And since the concept of the supply of money is vital both for the theory and for applied historical analysis of such consequences as inflation and business cycles, it becomes vitally important to try to settle these questions, and to demarcate the supply of money in the modern world. In The Theory of Money and Credit, Mises set down the correct guidelines: money is the general medium of exchange, the thing that all other goods and services are traded for, the final payment for such goods on the market.

***

Now, this is really nice, because it reiterates everything I’ve been explaining. And, I didn’t read it before just recently. Despite this promising start, however, we then devolve into pathetic nonsense.

Another entity which should be included in the total money supply on our definition is cash surrender values of life insurance policies; these values represent the investment rather than the insurance part of life insurance and are redeemable in cash (or rather in bank demand deposits) at any time on demand. (There are, of course, no possibilities of cash surrender in other forms of insurance, such as term life, fire, accident, or medical.) Statistically, cash surrender values may be gauged by the total of policy reserves less policy loans outstanding, since policies on which money has been borrowed from the insurance company by the policyholder are not subject to immediate withdrawal. Again, the objection that policyholders are reluctant to cash in their Austrian definitions of the surrender values does not negate their inclusion in the supply of money; such reluctance simply means that this part of an individual’s money stock is relatively inactive.

While all of these things can serve as money substitutes, replacing silver coins held in an iron box under the bed, they are not money. We have already established that all monetary transactions take place with Base Money, today exclusively a liability of central banks, since this is the only thing that can actually change hands. Bank deposits, and also life insurance policies, are not transactable.

We should ask the question here: Why do we care what the “money supply” is?

Who cares?

In the past, nobody cared. They cared that the value of the money was fixed to gold. There were hundreds and even thousands of issuers of currency, in the 19th century. Nobody even knew what the “total money supply” was. With the advent of the National Bank System, which did keep statistics, we had some decent measures. However, still nobody cared.

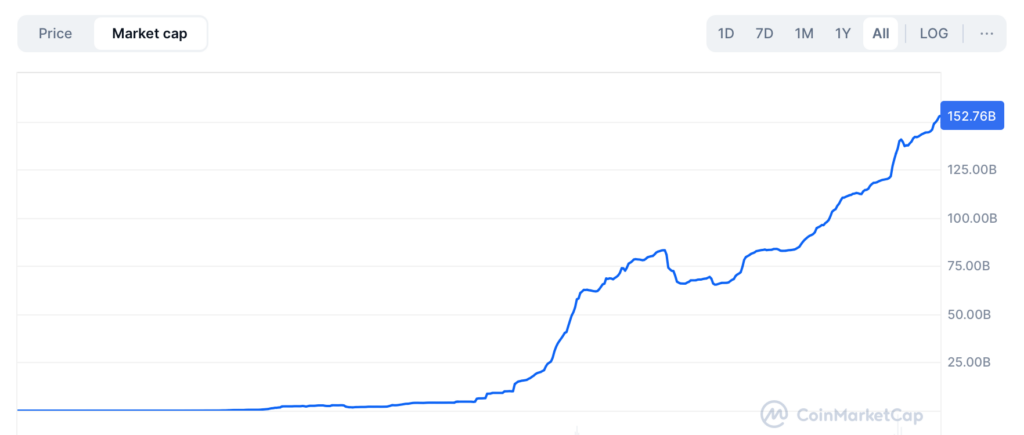

The Gold Standard, or any fixed-value policy such as today’s currency boards, are self-regulating systems. The supply is a residual of the mechanism (conversion) that keeps the value fixed to its standard of value. Today, we have the example of dollar stableoins such as Tether (USDT). What is the “money supply” of Tether? Nobody cares. Of course they care about the creditworthiness of Tether, about which there have been some doubts. But as long as it works, there’s no problem.

Here is the “money supply” of Tether.

There has been a huge expansion, although also some substantial retreats. If you just looked at this alone, you would probably say that there was some kind of catastrophe — either “inflation” from the huge expansion, or perhaps “depression” during the huge retreats. But actually, everything has been just fine (despite some periods of doubt), and Tether has maintained its fixed USD value just as, in the past, similar systems maintained values fixed to gold.