Previously, we looked into how much homes should cost. Basically, we concluded that the cost of homes should be a function of construction costs, which are basically stable, profit and some other non-construction costs such as corporate overhead, and land costs. Since there is no particular shortage of land in any U.S. city today, there is no particular reason for very high per-unit land costs; and thus, no particular reason why homes should cost very much more than construction costs.

October 22, 2017: How Much Should Homes Cost?

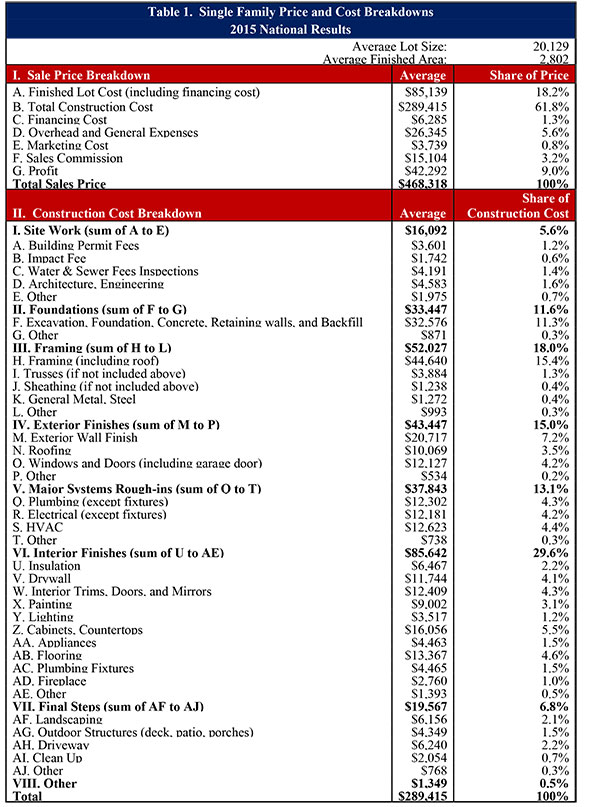

In 2015, newly-constructed single-family homes had a cost breakdown like this:

This is a situation where land is relatively plentiful — the average home site is half an acre, which is rather roomy for a single residence. I would argue that there is no particular reason to pay much more for land — as a percentage of total cost — even in higher-density areas. There, you would just use building forms which had a higher floor-area-ratio, such as the six-stories plus Narrow Streets for People form common to European cities such as Paris. Thus, although the per-square-foot cost of the land is higher, the land cost per square foot of built floor area can be about the same. The FAR in this example is 2,802/20,129 or 0.14. Actually, it is much less than that on a general basis, if you include all land such as the associated streets. The overall FAR is perhaps 0.10. (For larger suburban developments, where the developer also provides streets, this is intrinsic to the overall cost.) If we built at a FAR of 3.0 — including streets — which is not very difficult (six stories and 50% building footprint), you would have 30 times more floorspace on the same land; or, in other words, you could spend 30 times more on the land, while maintaining the same land cost/floor area ratio.

In this case, the cost of land is 18.2% of the total selling cost, which I might note, is just about the same as the 20% that I allocated in my “$50,000 San Francisco Home” example:

September 26, 2016: The $50,000 San Francisco Home

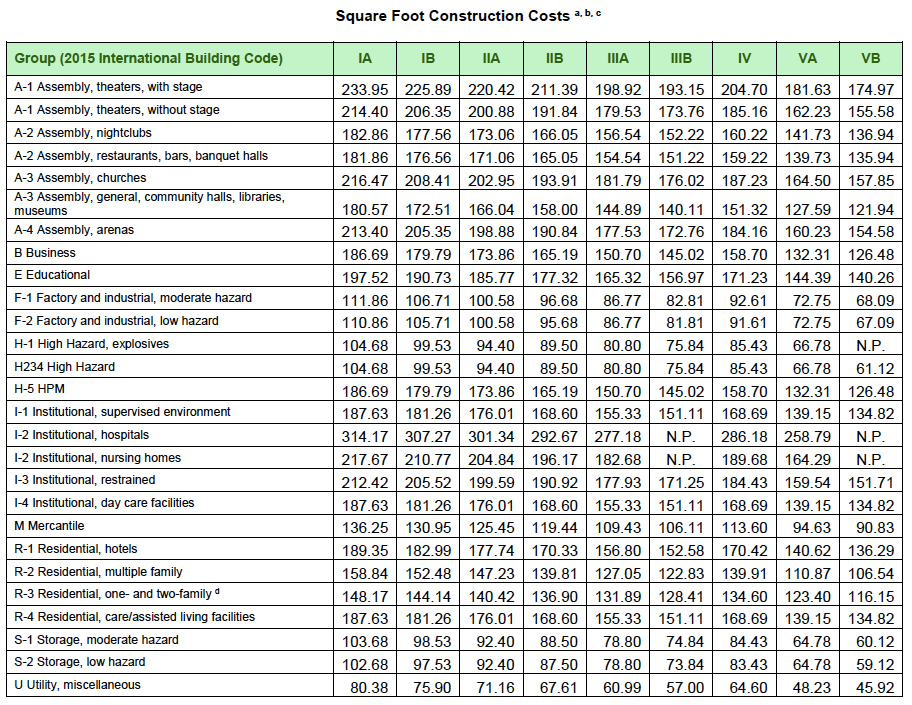

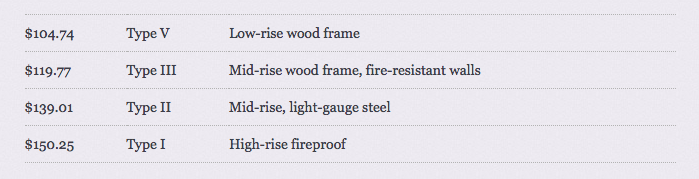

We see that total construction costs are 61.8% of the selling price in this example. The construction costs for this low-rise woodframe style are 2,802 square feet for $289,415, which is $103/sf — right in line with the $100/sf cost of low-rise woodframe structures that I often refer to. The total selling price is 2,802 sf for $468,318, which is $167/sf. If we double everything on a per-square-foot basis, which allows us to spend $206/sf on fireproof high-rise construction, then we would end up with $334/sf, which again is right in line with my $400/sf upper limit on the cost of newly-built homes. In this case, the cost of land would be 18.2% of $334, which is $60.79/sf. If you doubled the amount spent on land, to $121.58/sf, but the other factors (construction, overhead) were the same, it would just about hit that $400/sf target exactly. (Since we doubled the amount spend on land twice, we could spend 30×4=120 times as much on land as in the above example, with a FAR of 3.0.)

Now, let’s look at what that might mean in terms of rents.

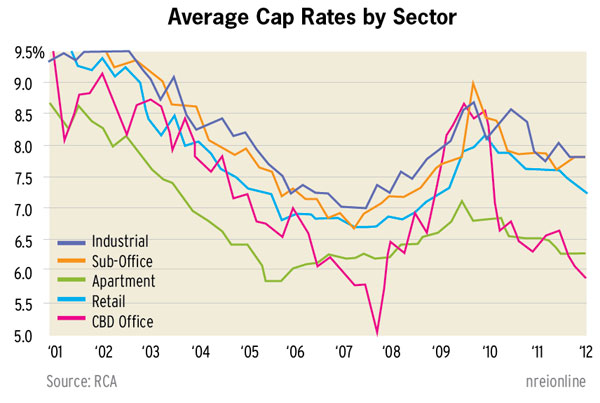

The valuation of buildings can change over time. The profit of a building to a landlord is basically the rental income minus expenses like property taxes, management, repairs, maintenance and so forth. This is the Net Operating Income. On this is placed a valuation, which could be expressed as a multiple of NOI. There are a lot of factors which go into this valuation, but interest rates are a big factor. If you could invest $100 million, would you be better off buying an apartment building, or a Treasury bond? If the $100 million apartment building generates $8 million of NOI per year (an 8% “capitalization rate”), that might be more attractive than a Treasury bond paying 4%, and less attractive than a Treasury bond paying 10%.

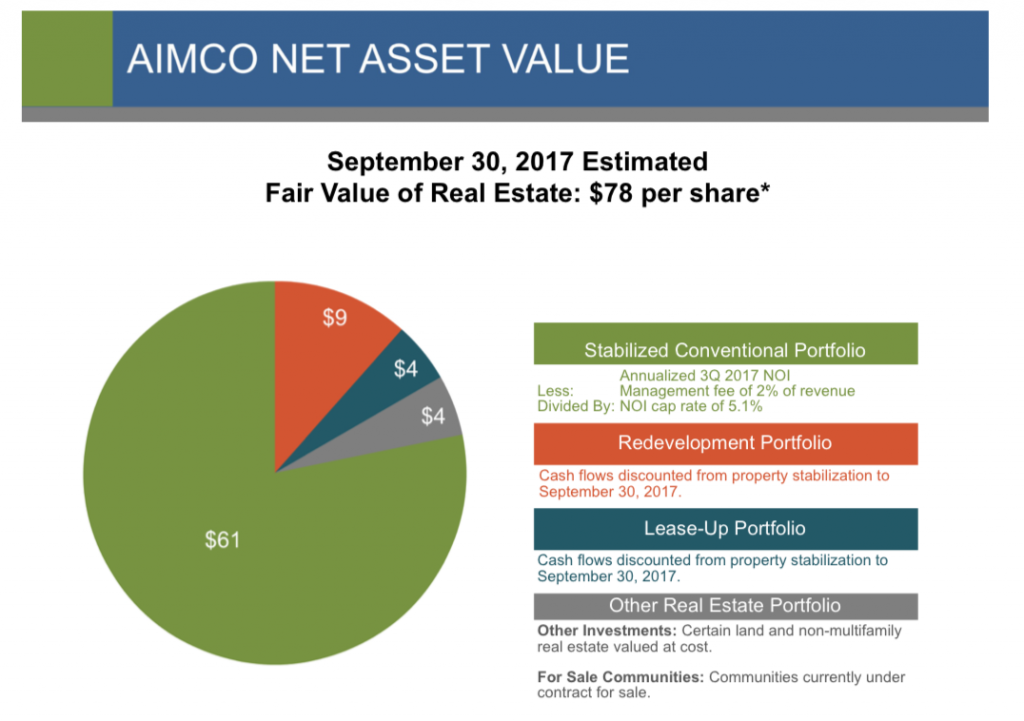

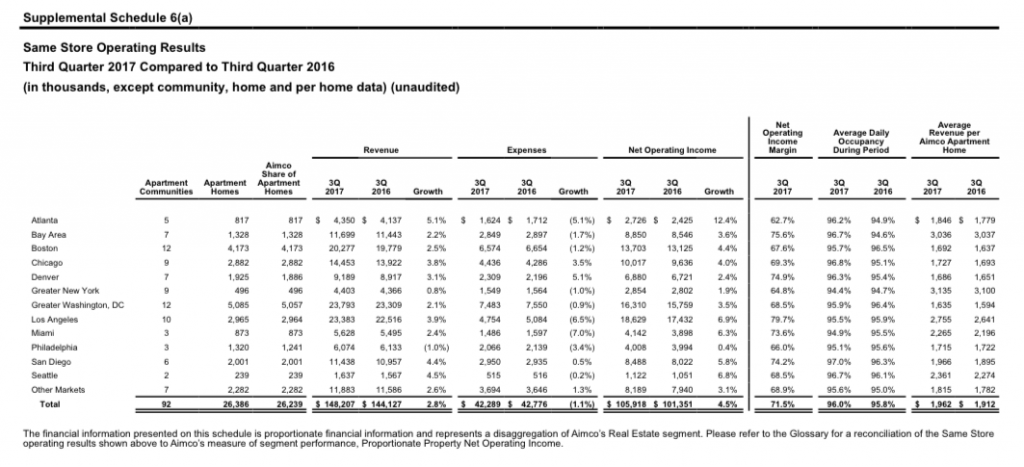

Aimco is a REIT that owns a large number of apartments in several U.S. cities. It provides an estimate of Net Asset Value to investors. This includes an estimate of the value of its real-estate holdings. Among these holdings are “stabilized” holdings, which are fully rented at relatively stable rents, and other properties which are being renovated, are not fully leased-up, or have other factors which do not represent their long-term earning capacity. Thus, we will look at the “stabilized” portfolio.

This tells us about all we need to know: the capitalization rate is 5.1%. In other words, NOI (adjusted by implied management fees) is 5.1% of the market value, or market value=NOI/5.1%. Thus, an apartment that generates $1 million of NOI is worth $1m/5.1% or $19.6 million.

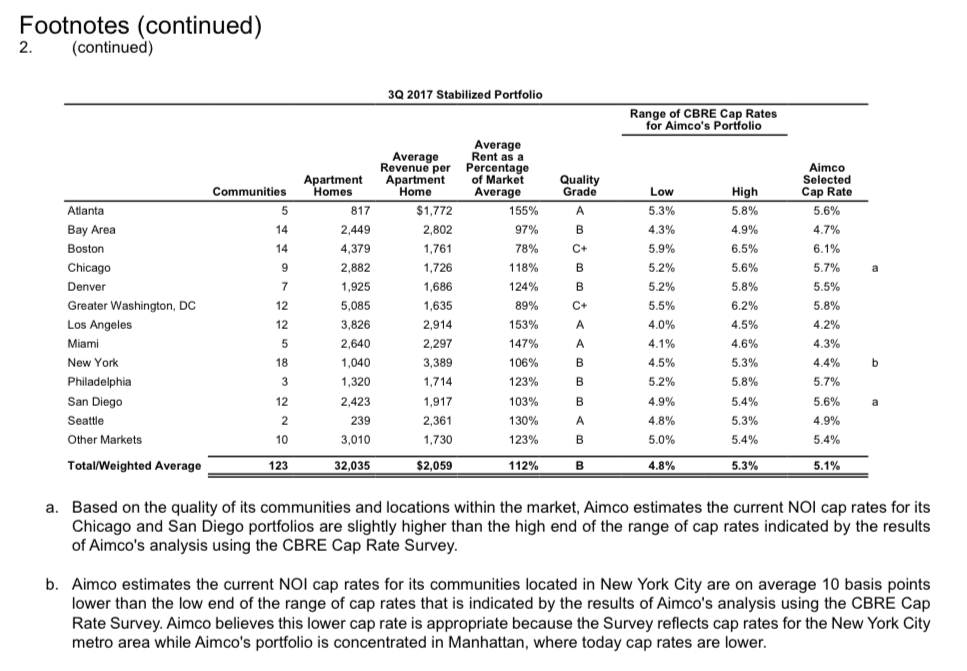

Here is a breakdown of properties and market cap rates.

However, NOI is the money that’s left after paying expenses. The actual rent paid is NOI + expenses.

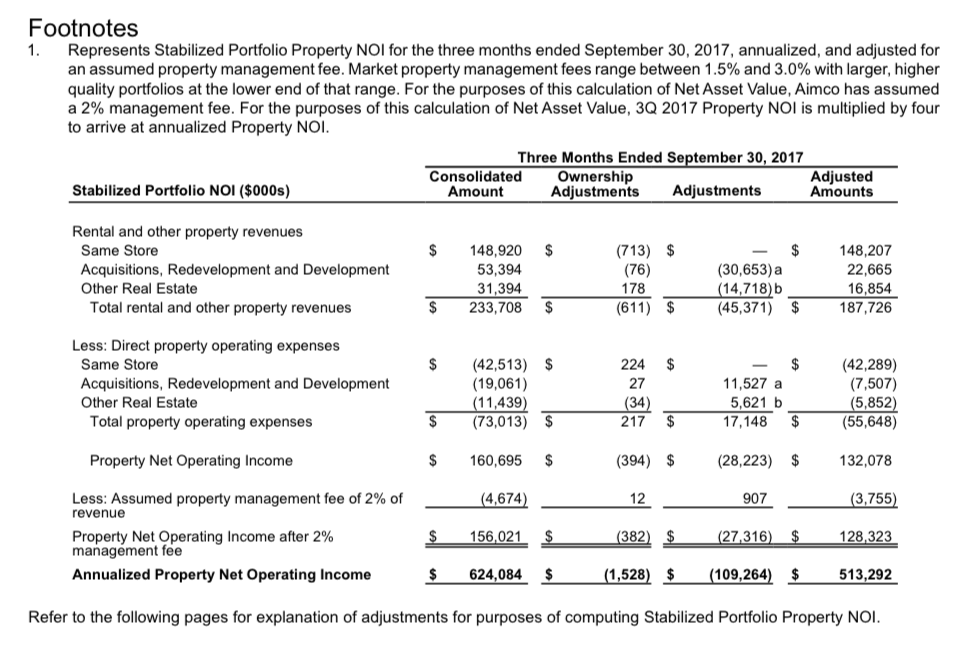

From this, we see that the NOI (adjusted for property management costs) is $128.323 million, out of total rental revenue of $187.726 million. The NOI margin is thus 68.4%.

Also, we have occupancy. Not every apartment is occupied with a tenant paying rent.

Here we can see that the occupancy was about 96%. That’s pretty high. So, the headline rent — the rent paid if there was 100% occupancy — would be 100%/96% or 104.2% of the actual rental income.

So, to get an idea of the ratio between property value and rent, we take the cap rate (5.1%), and divide by the NOI/revenue ratio (68.4%), and then divide by the occupancy ratio (96%). This produces a figure of 7.77%. Thus, the headline annual rent is 7.77% of the property value.

From this, if we have a building that would sell for $400 a square foot, we would have an annual rent of 7.77% of that, which is $31.08/sf. So, a 1000sf apartment would rent for $31,080 per year, or $2,590 per month. Or, a 200sf studio might rent for $518 per month. My 120sf “$50,000 San Francisco apartment” example would rent for about $311. If the building would sell for half of that, or $200/sf, as in our lowrise woodframe examples, the implied rents would be half of that.

Probably, there would be some additional costs for smaller apartments. Management fees would be a little higher, because you would have to deal with five times as many tenants if they were in 200sf apartments rather than 1000sf apartments. Also, the apartments would probably cost a little more on a per-square-foot basis to build and maintain, because even a little apartment still needs a kitchen and a bathroom, which are expensive. But, even if we adjust upwards by 20% to accommodate these factors (this seems generous), we can see that it is not too hard to make very affordable rental apartments, at a full market rate, even in the most expensive urban areas.