Recently, I’ve been doing a fair amount of historical research, and the similarities struck me between the gold standard proposal expressed by Lewis Lehrman in The True Gold Standard (2012) and the common practices and values of the Bank of France in the pre-1914 era, and also the twentieth century. This is no surprise, since Lehrman dedicated the book to Jacques Rueff, his mentor from the 1970s, and also a Deputy Director of the Bank of France who was quite influential in the deGaulle administration (1959-1969).

This proposal was fairly meticulously worked out, and I think it is pretty good in its details, although rather different in spirit than the British (Bank of England) or U.S. (Federal Reserve or National Bank System) traditions in these matters. Some of the salient details include:

1) No holdings of government debt. This is a different approach from the British or U.S. practice, where government debt is commonly one of the most desirable assets. The French tradition rejects government debt from first principles, to avoid any pressure by the government to finance its deficits. France held effectively no government debt in the pre-1914 period.

2) No foreign reserves. In the pre-1914 period, France, Britain and the U.S. were the only major central banks that held effectively no foreign reserves. Transactions and assets held in foreign currencies was quite common in the pre-1914 era, and became the basis of the Bretton Woods system.

Foreign Exchange Transactions and the “Gold Exchange Standard”

France acquired some foreign reserves as a result of its return to the gold standard in 1926, but then swapped all of these for gold soon afterwards.

3) Short-term commercial bills are the primary debt instrument, possibly combined with small holdings of longer-term commercial debt. Central banks grew up from commercial banks, who themselves were largely providers of working capital for companies via discounting (purchasing) of “commercial bills,” which were, essentially, accounts receivable. The use of “open-market operations” primarily in government bonds was something of a later development. Obviously, since government debt is banned on first principles, that would limit any open-market operations to corporate bonds, which are a much less liquid market, particularly in the time of Jacques Rueff, and particularly in France. The primary means of adjusting the amount of debt assets (discounting) would be the discount rate. Because the maturity is quite short, typically about six or eight weeks for a bill, total holdings could grow (from new purchases) or shrink (from maturity) without engaging in purchases or sales on the secondary market.

4) Base money liabilities would be convertible to gold on demand. Although direct convertibility is not a technical requirement for a gold standard system — the U.S. did not have it from 1933 to 1971 — it contributes a lot in terms of political and operational stability. In practice, without the legal requirement to produce either gold bullion, or an international reserve currency, on demand, central banks and governments can quickly become quite sloppy.

5) Circulation of gold coins would be encouraged. This serves again as an important symbol and reminder of the basis of the monetary system. It contributes a lot to the intellectual and political environment, even if it is not technically necessary. The British tradition since Adam Smith and David Ricardo had been to “economize” on gold, by substituting banknotes for coinage and intentionally discouraging coinage use.

Lehrman also adds a pretty good methodology for finding an appropriate new gold parity for the U.S. dollar, somewhat in the manner, perhaps, of France in 1926. This is a welcome change from the various strange and regrettably popular notions of Murray Rothbard, which amounted to a big dollar devaluation.

Let’s look at a little of France’s history in these matters.

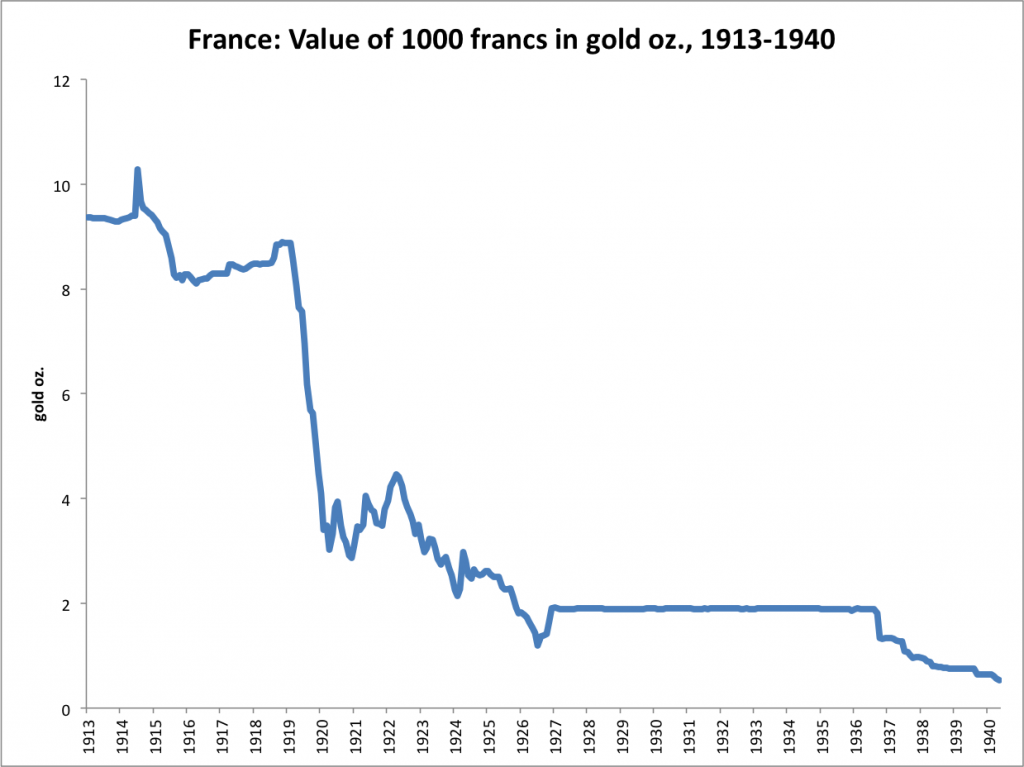

During World War I especially, the Bank of France was pressured to finance war deficits with the printing press. This led to a large decline in the value of the franc after the war.

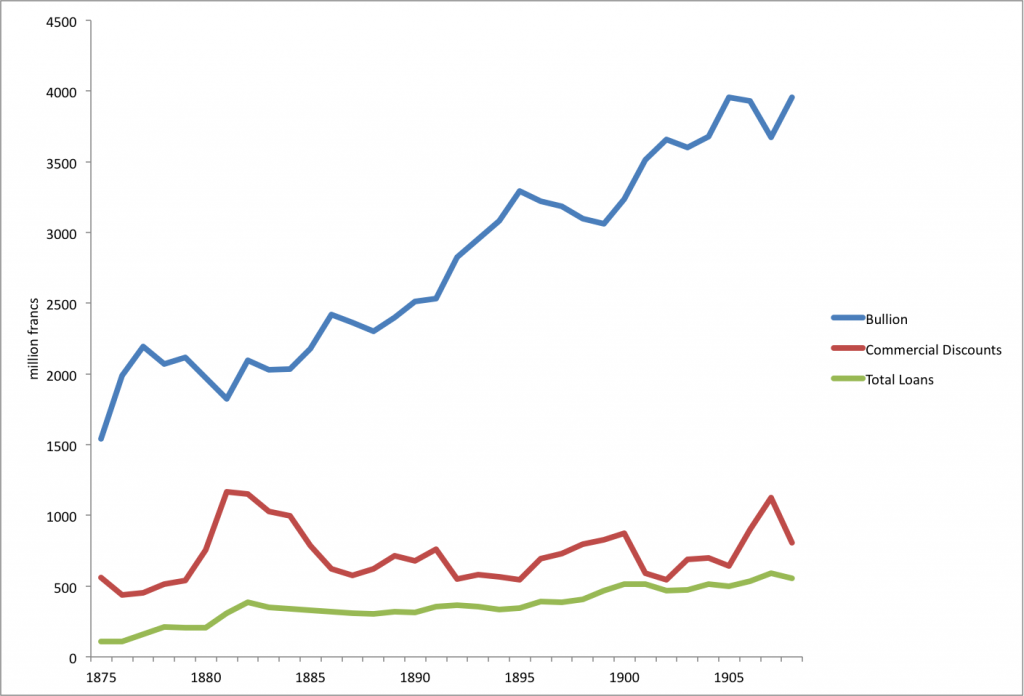

Bank of France, assets, 1870-1908

Gold bullion was the primary asset of the Bank of France, with a reserve ratio typically around 60% or higher. No government debt.

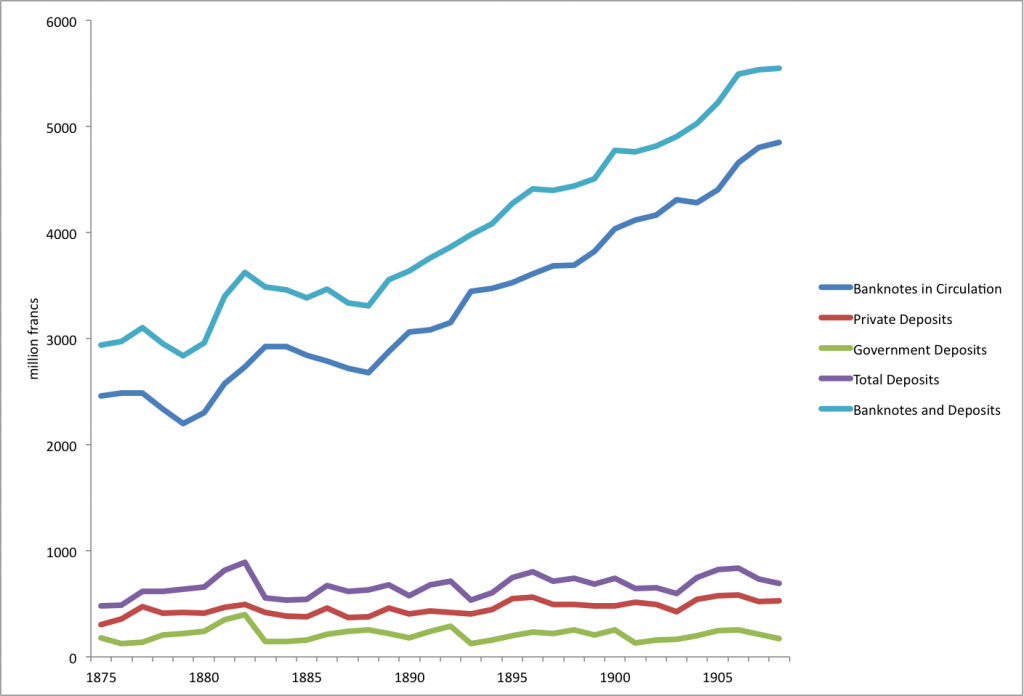

Bank of France, liabilities, 1870-1908

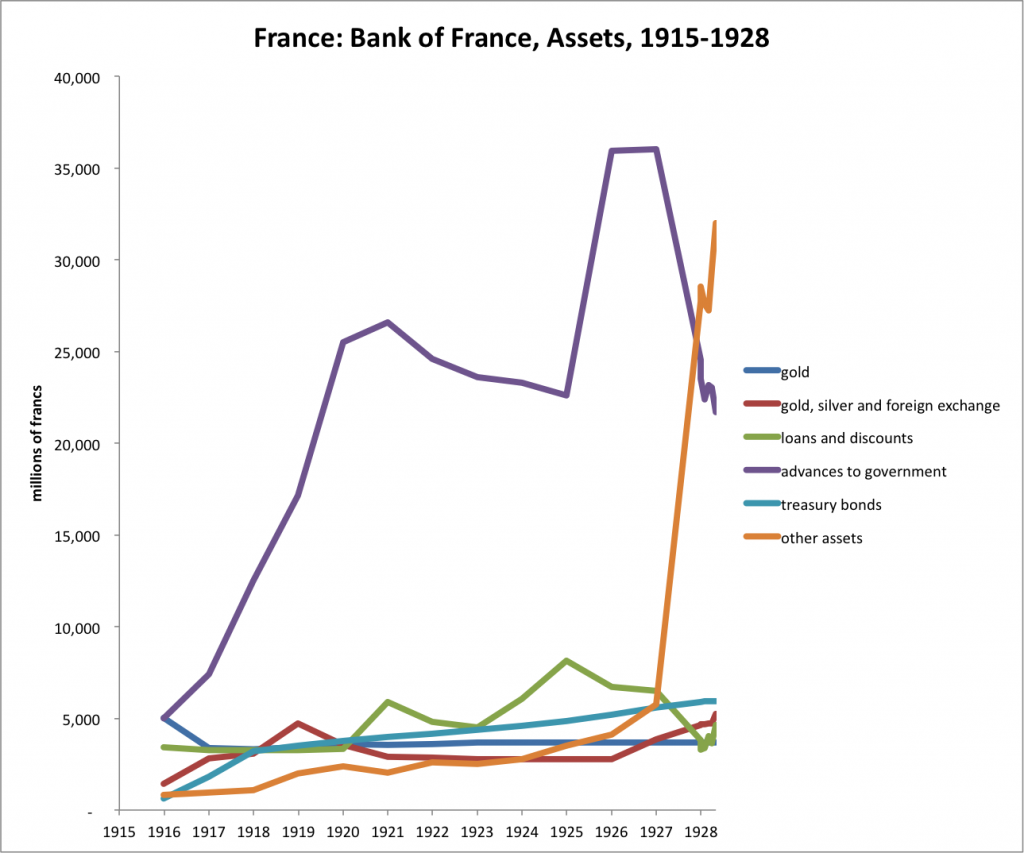

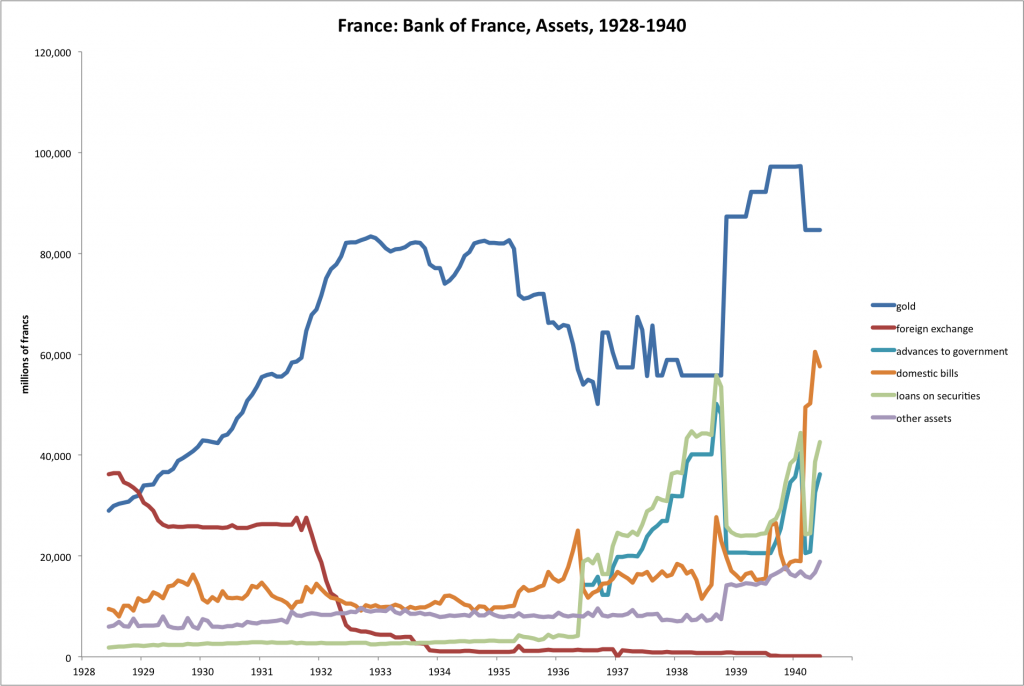

This is somewhat crude data, but illustrates the printing-press finance that took place during WWI. The franc was repegged to gold in 1926, but this was accomplished largely via a currency-board-type system with the British pound, which led to an increase in foreign reserve assets. In 1928, direct gold conversion was restored, and also, most or even all government debt had been purged from the Bank of France’s balance sheet.

After direct gold conversion was restored in 1928, the Bank of France then embarked on a program to swap its foreign reserve holdings for bullion. This was partially accomplished in 1928-1929. The Bank of France no doubt felt a little stupid for not completing the process before the devaluation of the British pound in 1931. Afterwards, remaining foreign reserve assets were swapped for gold bullion, thus returning the Bank of France to something like its pre-1914 practice of holding large bullion reserves and commercial bills. However, after the devaluation and floating of 1936, government financing (“advances to government”) makes a big reappearance. The franc’s value slid downward again after 1936.

All in all, it is a meticulous and functional solution, with no great problems that I see except perhaps that adopting France-like bullion reserve ratios of 60%+ worldwide could be problematic. Eliminating reserve-currency systems (“gold exchange standards”) is one goal of the proposal. I agree that dependence upon reserve currencies has tended to cause disruption when those reserve currencies are themselves devalued, in 1914, 1931 or 1971, so the idea of greater independence from the mistakes of a single government is a desirable trait. Many of the rationales favored by Rueff, focusing especially on the “balance of payments”, I find to be mistaken, but that was a common notion throughout the world in the 1960s.

I find it quite nice to have a proposal that is sensible — this has been unfortunately rather rare — and also from a different sort of intellectual tradition than we are accustomed to. I myself have come from nearly the opposite tradition, tending toward the Ricardian (British) “gold price rule” or gold standard system without convertibility at all and thus no need to hold any gold reserves at all; combined with an operational dominance of open-market operations in government debt assets. This is also an important principle to understand. But, by integrating and appreciating the virtues of both systems, and also many other variants, we can develop the breadth of expertise and familiarity with underlying principles that I think is necessary today.