Bank Reserves 2: Reserves Out the Wazoo

March 13, 2011

Last week, we were looking at what bank reserves are, the fuction they have in a monetary and financial system, and typical reserve/deposit ratios over time.

We saw that, historically, banks held rather high reserves, which is to say, that they held a high percentage of their total assets in the form of cash, literally paper bills. This was so that they could meet any obligations that could arise, and also reflected the availability of attractive lending opportunities. Banks try to balance their desire to earn interest income from loans, and also to be able to meet obligations.

The numbers here are direct from the Federal Reserve.

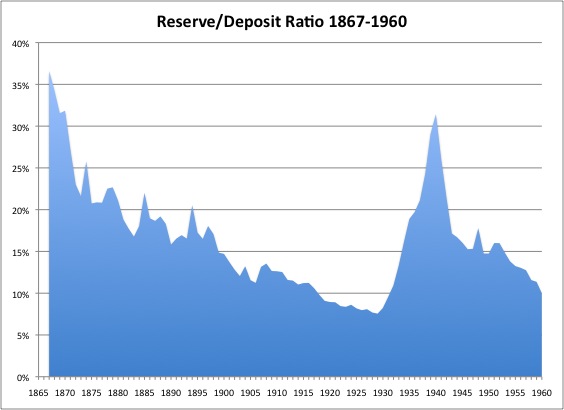

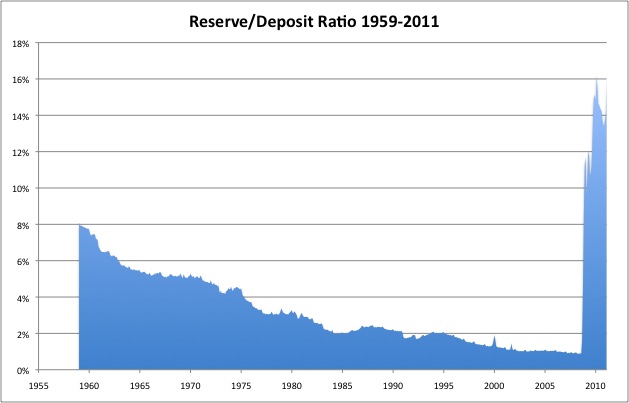

What we see is that during the 19th and the first half of the 20th century, banks typically held reserves of 10% or more of their deposits, although the ratio slipped below 10% during the Roaring ’20s. Beginning around 1960, this tumbles to much lower levels, ending up around 1% in the last couple decades. In recent times, bank reserve holdings have risen to a much higher level (15%), but take note that this much higher level was in fact a common level in the past, and indeed was exceeded when banks were under great stress, as in the 1930s (25%+).

Let’s say a bank has an obligation, but doesn’t have adequate cash (reserves, base money) to meet it. For example, depositors may withdraw their money, or depositors may draw down their accounts to meet some obligation, or some sort of loan (CD, bond) may be coming to maturity. Maybe the bank just wants to make even more loans. If the bank doesn’t have the cash, it must borrow the funds from someone else, typically another bank, at least for short-term financing. On the other hand, let’s say you are a bank with plenty of funds (reserves, base money). You decide that you don’t want to just sit on a big pile of banknotes, which don’t earn interest. You can lend the money to another bank, and make a little money. So the banks that want to borrow funds and the banks that want to lend funds meet on the interbank lending market. This is the interbank lending rate. There are overnight (one day) rates, one week rates, one month rates and so forth.

So the bank goes and borrows the money. But what if nobody lends money to the bank? Then it defaults on its obligations, which leads immediately to bankruptcy. Ouch. Why would a bank not lend money to another bank? Because a) they don’t think the bank will pay it back (credit risk), or; b) they don’t have the money to lend. If the bank’s risk of not being able to borrow is high, then the bank would tend to hold more reserves so that it doesn’t need to borrow. This is like holding more cash in your wallet if you think your credit cards might be declined.

The Federal Reserve was created in 1913, but it didn’t really become active until about 1918 or so. This is about the point at which banks begin to lower their reserve holdings below 10%. The Federal Reserve accomplished a couple of things, compared to the situation before 1913. The first thing is that it removed the risk of systemic liquidity shortage crises, which were a chronic problem during the 19th century and culminated in the Panic of 1907. The second thing is, the Fed provided an agent that could be appealed to if a bank wasn’t able to borrow from other banks due to credit risk fears. In other words, a bank could borrow from the Fed if no other banks would lend to it. The Fed was a “lender of last resort.”

This reduced a bank’s risk of not being able to obtain funding. So, over time, in order to maximize profitability, banks held less and less reserves until they held almost none at all.

Bank reserves, whether in the form of paper banknotes or Fed electronic registry, are a form of base money. Naturally, as banks tend to hold less reserves, the percentage of base money that consists of bank reserves has fallen.

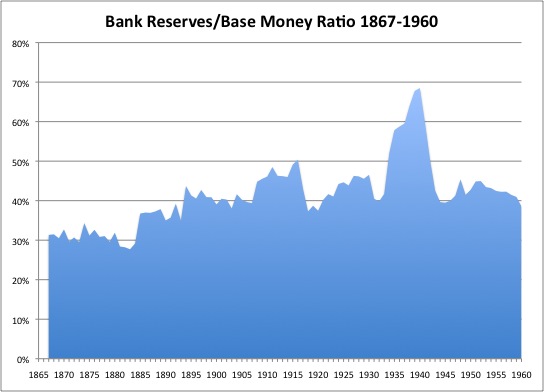

Here is a chart (once again from Friedman) that shows what percentage of base money consisted of bank reserves. We can see a sort of plateau around 40%.

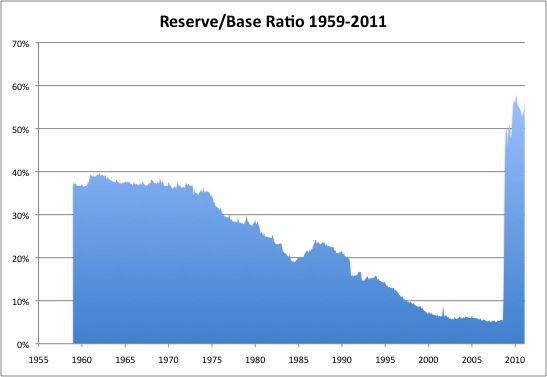

And here are the more recent figures. We see that bank reserves fell to a rather low portion of the monetary base. The recent spike higher returns the figure to more like its historical levels.

Now we have some figures on the supply of bank reserves, a form of base money. Later, we will think about the demand.