We’ve been taking a little look at Murray Rothbard’s influential 1962 book, America’s Great Depression.

January 31, 2016: Blame Benjamin Strong

Some people won’t like me for kicking sand in the face of Murray Rothbard. For them, everything is politics. Rothbard was one of the twentieth century’s great champions of libertarianism in general, and Classical economic thought in particular. The quantity and quality of his output was awesome. He was, among other things, a really fine writer, whose books and articles work both as popular pieces and serious academic work. This stands in contrast to, for example, Ludwig von Mises, who was encased in the tradition of Germanic academia, and whose writings sound the same turgid tones as Immanuel Kant. The thing that makes von Mises readable is that he was right about so many things. Today’s academics are almost completely unreadable, combining obfuscating prose with masturbatory mathematics, to arrive at conclusions that are laughably misguided.

Thus, it would seem, to these politically-minded people, that I should direct my attention somewhere else. Maybe Paul Krugman? But, I see it a little differently. The problem with the Classical economic tradition, as it exists today, is that it is too full of error and fallacy. If it is going to serve some purpose, this crude iron must be refined into steel.

I was going to look at Rothbard on a line-by-line basis. However, the two chapters of America’s Great Depression that I want to deal with, chapters 4 and 5, together constitute 84 pages of text. My comments would add more. So, I will try to summarize Rothbard’s arguments. Feel free to read the chapters yourself.

https://mises.org/library/americas-great-depression

The gist of my argument will be that the Federal Reserve was on a gold standard system. The value of the dollar was verifiably close to its gold parity, of $20.67/oz., by every measure. The mechanisms to produce this outcome — especially gold convertibility — were actively in place. A central bank, or other currency manager (and there were thousands of banks issuing banknotes in the 1920s, within the National Bank System) can’t really engage in very much “discretionary” policy at all. Any deviation of currency value from the gold parity would result in a correction of the previous error. In practice, you could have a little bit of “discretionary policy” if you also have substantial capital controls to batter the gold parity back in line. This was the case during the 1950s and 1960s, but not during the 1920s. Even then, you couldn’t really deviate from the gold standard by very much, not enough to cause any kind of major mayhem, like the Great Depression.

This, of course, is what Keynesians complained about for decades before 1971, the “Golden Fetters” that prevented them from engaging in whatever form of currency distortion they felt would help solve the problems of the day. It is no different than those countries who link their currencies to the euro via a currency board today: in doing so, they give up all avenues of independent domestic economic management via currency manipulation. And, Rothbard should know this. It’s funny that he doesn’t. Instead, he claims a worldwide economic catastrophe, that was due to something that happened while on the gold standard! The natural conclusion is that the gold standard system did not prevent, and perhaps even caused, the worst kind of disaster — a rather odd stance for a gold-standard advocate, especially when the natural gold-haters, the Keynesians, make no such accusation.

The second important part of my arguments is that money and credit are very distinct. Rothbard subscribes to an error of Classical thinkers throughout the 20th century which mixes money and credit in a confusing stew. This was also apparent in, for example, von Mises’ Theory of Money and Credit of 1913. I won’t go into the problems of this in detail now, but I think it is enough to understand that all of the activities of banks, including expanding or contracting credit, could and did take place with a monetary system consisting of gold and silver coins alone. It should be obvious that all of this business concerning lending can have no effect on the money, which is an unchanging lump of metal; and that the money, which is an unchanging lump of metal, can have no effect on bank managers’ activities. The same is basically true of representative monies (paper banknotes) which have an unchanging value ratio to an unchanging lump of metal, of $20.67/ounce.

The confusion here is related from the “Austrians'” own experience with hyperinflation in Austria in 1919-1924. The exact details of this hyperinflation, at least in the German case (I assume Austria was similar) was that the Reichsbank would “discount the bills” of banks. “Bills” here were short-term government debt. “Discounting” means buying them, using cash from the printing press. “Discounting” was basically a purchase, but it had a close relationship and historical connection with collateralized lending, and so it was often considered a sort of loan to banks. Thus, the Reichsbank, by purchasing government debt, was in a sort of fashion “making a loan to banks.” Obviously, making a loan is “expanding credit.” Even if you take the banks out of the loop, and just consider that the Reichsbank was buying government debt from the government directly (which was effectively the case), then the Reichsbank’s balance sheet would hold more and more government debt, purchased with the printing press. (No different than “QE” today.) A bond or bill is very similar to a loan, so you could say that the Reichsbank was “expanding credit” to the government, via the printing press.

The discount rate on these bills was very low. In Germany during the hyperinflation 1919-1923, it was 5%, until the very end. In effect, banks were paying 5% on their capital, at a time when a consumer price index was rising at hundreds of percent per year. “Real” interest rates were dramatically negative. The result was an explosion in lending. Banks had to open new offices to handle all the loan demand. Thus, “credit expansion” by the central bank also led to “credit expansion” by banks — within the context of hyperinflation, NOT a gold standard!

Americans didn’t have this traumatic experience with hyperinflation, and indeed they probably didn’t even really understand what was being referred to by those economists from Austria who would talk about it while quivering with PTSD. So, I think the American disciples of the from-Austria Austrians tended to expand this description really far beyond its original intention.

Let’s just look at what was going on with the Fed and other central banks in the 1920s. I’ve discussed this before, in greater detail, so go back and look at those items if you want to:

August 10, 2014: Gold Holdings of Central Banks and Governments, 1913-1941

August 3, 2014: The Reichsbank, 1924-1941

July 27, 2014: The Bank of France, 1914-1941

July 20, 2014: The Bank of England, 1914-1941

July 18, 2014: Foreign Exchange Rates 1913-1941 #8: A Brief Summary

June 22, 2014: Foreign Exchange Rates 1913-1941 #7: Switzerland’s Independence; Turkey Avoids Devaluation

June 1, 2014: Foreign Exchange Rates 1913-1941 #6: Hyperinflation in Poland; Russia’s WWI Decline

May 25, 2014: Foreign Exchange Rates 1913-1941 #5: Devaluations By Japan and France

April 27, 2014: Foreign Exchange Rates 1913-1941 #4: Britain Leads the World Into Currency Chaos

April 20, 2014: Foreign Exchange Rates 1913-1941 #3: The Brief Rebuilding of the World Gold Standard System

April 6, 2014: Foreign Exchange Rates 1913-1941 #2: The Currency Upheavals of the Interwar Period

March 30, 2014: Foreign Exchange Rates 1913-1941: Just Looking At the Data

January 26, 2014: The Federal Reserve in the 1930s #2: Interest Rates

January 19, 2014: The Federal Reserve in the 1930s

November 25, 2012: The Federal Reserve in the 1920s 2: Interest Rates

November 18, 2012: The Federal Reserve in the 1920s

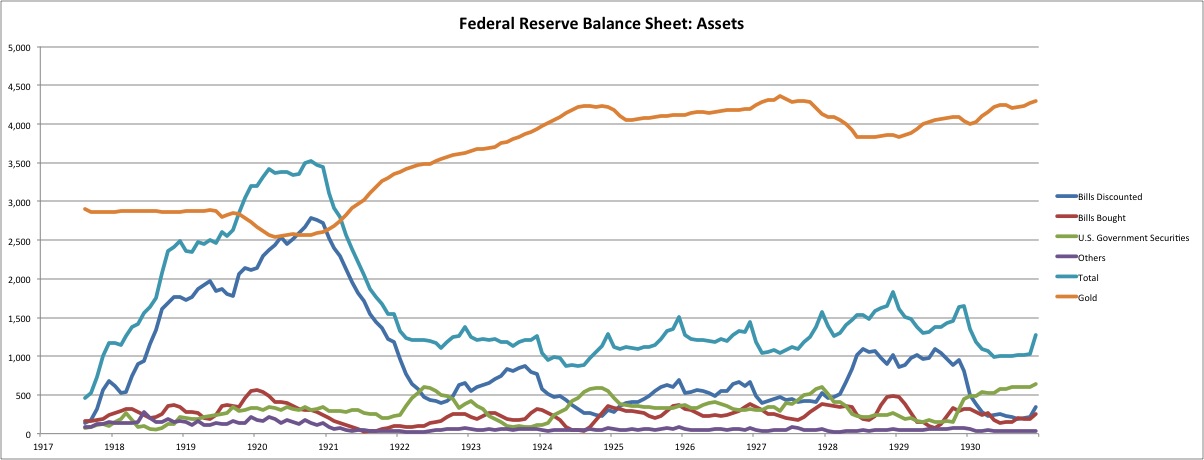

For now, ignore the big rise and decline before 1923. I talked about this here:

March 25, 2012: The U.S. Dollar During WWI and the Recession of 1920

By 1923, the dollar was effectively back on the gold standard at the prewar parity. This required some monetary contraction in 1920-1922. It was basically the same thing that Britain did in 1925, although rather more abrupt. So, I’m just going to be talking about the period after the start of 1923.

The orange line is gold bullion. The teal line labeled “total” is all non-gold assets, including government securities, bills bought, and bills discounted. These are all forms of “credit,” and thus the aggregate could be termed “Fed Credit.” For there to be a “credit expansion,” then the teal line would have to rise. Look at the teal line.

Did it rise?

It did, by a little bit, in 1928. So what. The wiggles here are basically irrelevant, as we will see.

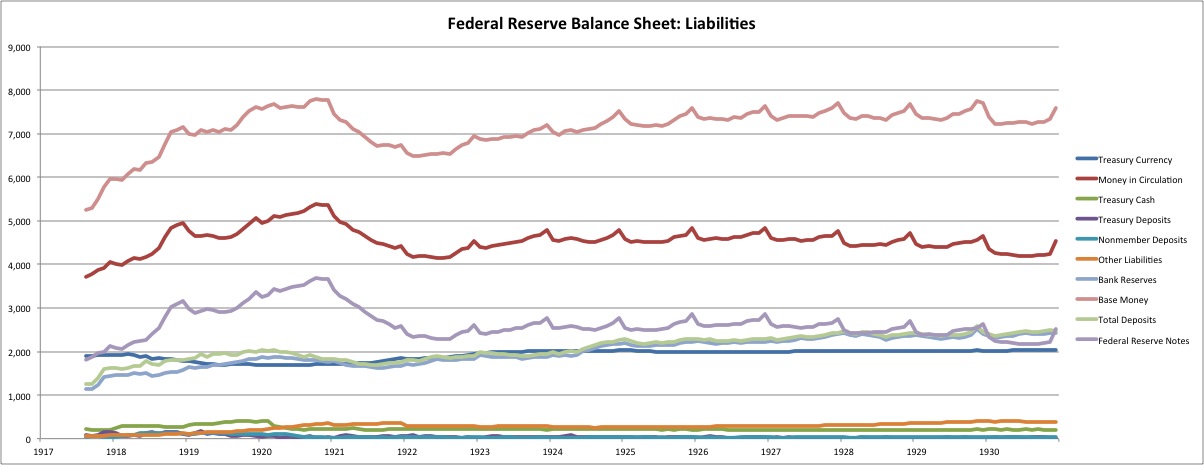

Here are the liabilities of the Fed and, strangely, also other banknote issuers including the Federal government (Treasury gold certificates) and the other note-issuing National Banks. What, the Fed wasn’t the monopoly issuer of currency? The Fed was not an effective monopoly issuer until after WWII.

From this we see that total base money (the top pink line) was hardly changed during the decade. There was no expansion at all. What little bit of “credit expansion” took place in 1928 by the Fed was offset by a reduction in gold bullion. The net result was zilch.

Was there any expansion in 1924, supposedly to help Britain return to the gold standard in 1925? There was none. “Fed credit” actually contracted in 1924, offset by an increase in gold bullion holdings.

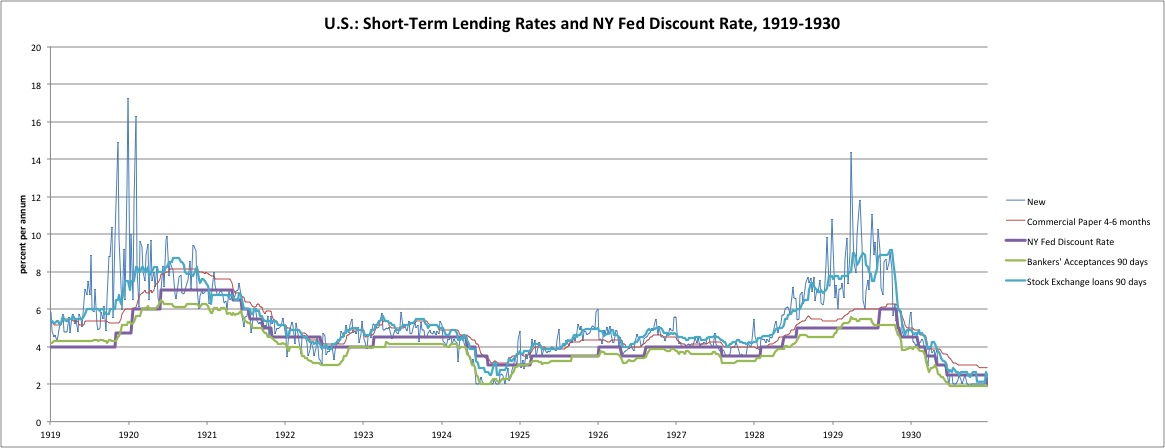

The Fed was originally conceived to be a “lender of last resort,” with a policy of a discount rate well above the typical rate of discount among private banks. This was known in 19th century central-banking terms as a “penalty rate.” However, the Fed wanted to have some loans on the books, for the simple reason that, if there was no debt on the balance sheet, then there would be no seignorage profits to pay dividends and expenses. Thus, in practice the Fed maintained a discount rate near the market rate.

For whatever reason, the market rate was apparently falling in 1924. The Fed was playing catch-up with its falling discount rate. This is apparent because discounts actually fall in 1924 despite the lower rates. Thus, the 1924 rate cuts were not “expansionary” in any way. They were to keep discounts from contracting still further. It didn’t matter either way, because the natural process of gold redeemability and monetization (here it was “monetization,” or gold inflows) made up for the contraction in the loan book, resulting in stable base money.

Rothbard concentrates on some funny business in 1927, which supposedly caused a great inflation:

[Federal Reserve Chairman Benjamin] Strong and [Bank of England chief Montagu] Norman organized the famous inter-central bank conference at New York, in July, 1927. The conference was held in camera, and included Norman, Strong, and representatives from the Bank of France and the German Reichsbank … Remaining to weld their inflationary pact, Norman and Strong agreed to embark on a mighty inflationary push in the United States, lowering interest rates and expanding credit—an agreement which Rist maintains was concluded before the four-power conference had even begun. Strong had gaily told Rist that he was going to give “a little coup de whiskey to the stock market.” Strong also agreed to buy $60 million more of sterling from the Bank of England.The British press was delighted with this fruit of the fast Norman–Strong friendship, and flattered Strong fulsomely. As early as mid-1926, the influential London journal, The Banker, had said of Strong that “no better friend of England” existed, had praised the “energy and skillfullness that he has given to the service of England,” and had exulted that “his name should be associated with that of Mr. [Walter Hines] Page as a friend of England in her greatest need.”

In response to the agreement, the Federal Reserve promptly launched a great burst of inflation and cheap credit in the latter half of 1927. Table 8 shows that the rate of increase of bank reserves was the greatest of the 1920s, largely because of open-market purchases of government securities and of bankers’ acceptances. Rediscount rates were also lowered. The Federal Reserve Bank of Chicago, not under the domination of the Bank of England, balked vigorously at lowering its rate, but was forced to do so in September by the Federal Reserve Board. The Chicago Tribune called angrily for Strong’s resignation, and charged that discount rates were being lowered in the interests of Great Britain. The regional Reserve Banks were told by Strong that the new burst of cheap money was designed to help the farmers rather than England, and this was the reason proclaimed by the first bank to lower its discount rate—not New York but Kansas City. The Kansas City Bank had been picked by Strong as the “stalking-horse” of the new policy, in order to give as “American” a flavor as possible to the entire proceeding. Governor Bailey of the Kansas City Bank had no inkling of the aid-to-Britain motive behind the new policy, and Strong took no pains to enlighten him.

pp 154-156

What to make of all this?

There certainly was a modest expansion in “Fed Credit” in 1927, although it was via purchases of government securities, not direct bank lending. Bank lending was actually rather depressed throughout 1927, which indicates that the small reduction in the discount rate had no real effect. Bank reserves did rise, although that rise was tiny. Get out your magnifying glass and look at the expansion on the Asset side of the Fed’s balance sheet. Bank lending had a big burst in 1928, while the Fed’s discount rate was actually rising. This was offset by reductions in government securities, but the overall effect was a further expansion of “Fed Credit” in 1928.

Now, let’s say that this expansion in “Fed Credit” was undertaken just as Rothbard says, due to various international agreements and so forth. What then? Well, we would expect this excess supply of base money to result in an incipient decline in the value of the dollar vs. its gold parity. At some point, people would come and trade base money (banknotes and deposits) for gold — in other words, gold redeemability. Gold bullion would flow out, and base money would contract.

And, that is exactly what happened. Gold bullion outflows exactly counteract the expansion in Fed Credit perhaps engineered by Strong. The net result was zippo, nada, zilch. Overall base money (liabilities, top pink line) show no meaningful change at all.

Exactly as it should be — with a gold standard system.

If you get out your microscope, what you would find is that the value of the dollar fell to its “bullion point” — the point at which the deviation of the market value of the dollar from its gold parity was large enough that the advantages of gold redemption (or “monetization” aka gold inflows) outweighed their small costs.

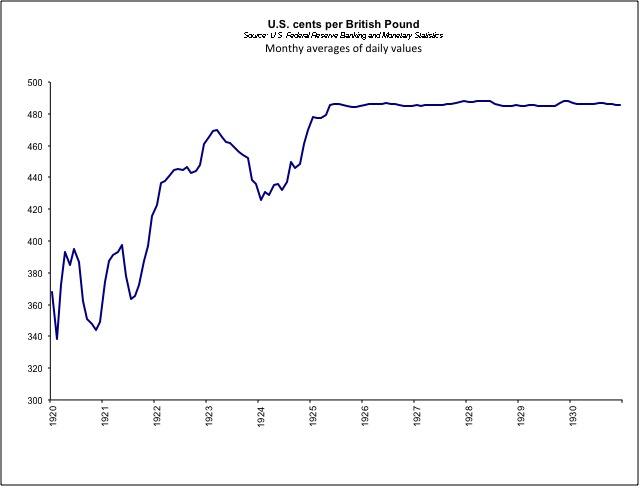

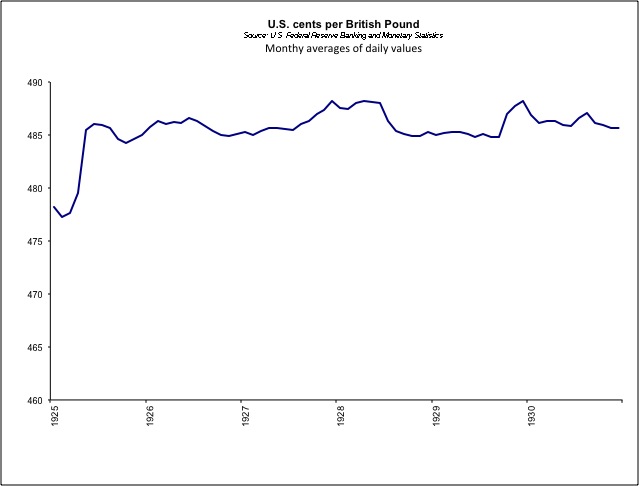

Here’s what the U.S. dollar/British pound foreign exchange rate looked like at the time:

Here we see the increase in the value of the British pound, after WWI, to return it to its prewar parity. This was accomplished in 1925. Then, there’s a flat line. When the dollar is on a gold standard, and the pound is on a gold standard, then they naturally have a fixed exchange rate.

However, there is a tiny wiggle in the line after 1925. Those are the “bullion points” in action. Here’s a closeup:

The wiggle is a few U.S. cents per pound. A 1% move here is about 4.85 cents. So, these moves of 2-3 cents either way were less than 1%. You can see the decline in the value of the dollar vs. the pound, as the Fed expanded “Fed Credit” beginning in mid-1927. The move was about 3 cents tops. Less than 1% — before gold redeemability acted to cancel out any more expansion.

Do you see what I mean when I say that these things that Rothbard talks about didn’t matter, and couldn’t have possibly mattered? They obviously didn’t matter — to overall base money supply, or the value of the currency, whether the U.S. dollar, British pound, or any other currency.

And … that’s it. These tiny wiggles were of no significance to anyone except a few forex traders and central bankers themselves. They had no meaningful effect on any economy, not even a small effect, and certainly not any Great-Depression-causing effect. They had no more effect than a 1% move in the dollar vs. the euro might have today. I find it amusing that people who have spent their whole lives in floating-currency chaos want to jump up and down and make a big deal out of the wiggle in the chart above.

Now, some interesting conclusions can be drawn from all this:

First of all, I know what you are thinking. There is some kind of great disconnect between Rothbard’s heated rhetoric, and the statistics you can see here with your own eyes. You want some way to reconcile them. There must be some part of the story that you aren’t seeing. Well, let me tell you: there isn’t. The statistics you see with your eyes were the reality of the day.

Now, the next thing you notice is: why hasn’t anyone talked about this before? Good question. These things just get handed down from generation to generation, without anyone asking the most obvious questions. You wouldn’t think that would happen, but it’s what actually happens.

And now, you notice another thing. There really was a central-banker meeting in New York in July 1927, and apparently things were said, and things were done — things that, in themselves, also make no sense, in light of what we’ve seen.

My interpretation is: by the 1920s, people (including central bankers) really were itching to “manage the economy” along somewhat proto-Keynesian lines. Central bankers liked to indulge in a sort of pageantry as if they were actually doing something meaningful, rather than acting as neutral maintainers of the gold standard parity. That is a boring job. You just maintain the parity via various techniques (which I describe in detail in Gold: the Monetary Polaris), which isn’t all that hard to do, and then head to the bankers’ club at 2pm. It was a lot like maintaining a currency board today. There is no decision-making involved. The world’s most boring job. Even in the pre-1914 era, although fiddling with the economy wasn’t so much of a goal, central banking had become somewhat absurdly overcomplicated given the inherent simplicity of its task. Maybe, without making it overcomplicated, they couldn’t even find enough to amuse themselves until 2pm. Certainly not enough to justify some sexy secretaries.

During the 1920s, people understood the form of the gold standard system, but they had already begun to lose their grasp of its underlying principles. The idea that money was to be stable, neutral and unchanging — and that great economic benefits flow from this — was fading from their vision. They wanted to fiddle with the economy, with interest rates, with commercial banking, with everything they could get their hands on, without really understanding that this was all unnecessary, ineffective, conterproductive, and contrary to the basic premises of gold-based money.

In short, it was somewhat like the Bretton Woods years, 1944-1971, but not so bad yet. In the 1920s, people still understood most of the techniques to maintain their gold parities — that, one way or another, base money should be contracted to support a currency’s value, or expanded if the value is too high. Even this was slipping, as we can see regarding all the discussions about “the pound’s value was too weak” etc. etc., which was the simplest thing in the world to solve, long before it even became a topic of discussion. Nevertheless, enough of the old knowledge held that things still ran pretty smoothly. Even though Benjamin Strong seemed to want to fiddle with things, the end result, after being cancelled out by gold redeemability, is that he could have just as well stayed home and played dominoes.

By the 1960s, even the gold advocates like Murray Rothbard didn’t understand these basic concepts — the concepts that I talk about in detail in Gold: the Once and Future Money and Gold: the Monetar Polaris. And, once the gold advocates themselves are lost at sea, you haven’t a chance. It’s over.

To give an idea of what I’m talking about, I’ll quote a bit from the final chapter, the “Conclusion,” of Barry Eichengreen’s influential 1995 book, Golden Fetters: the Gold Standard and the Great Depression, 1919-1939. Much of the book is flawed, but Eichengreen did spend a lot of time looking into historical details, and that informed his perspective:

The interwar gold standard’s problem become comprehensible when the circumstances in which it operated are contrasted with those that prevailed before World War I. Before the war, the operation of the international monetary system rested on the credibility of the commitment to gold convertibility and on international cooperation. That credibility was predicated on the insulation enjoyed by central bankers and other government officials from pressures to adapt policy to potentially incompatible ends. Such insulation reflected the fact that the connection between monetary policy and unemployment were only vaguely understood. …

World War I transformed those circumstances. The credibility of the commitment to gold was undermined by the erosion of central bankers’ insulation from political pressures. In response to Europe’s postwar experience with inflation and stabilization, explicit analyses of the links from restrictive monetary policy to unemployment were articulated and widely circulated. Although the details of those analyses differed across countries, they served to heighten awareness, wherever they appeared, of the impact of monetary policy on domestic ecnomic conditions. …

A shadow was cast over the credibility of the commitment to gold. No longer did private capital exhibit the same tendency to flow in stabilizing directions as it had before World War I. The markets, rather than minimizing the need for government intervention, subject the authorities’ stated commitment to early and repeated test.

pp. 390-391

So, you can get an idea of why all these central bankers were scurrying back and forth having meetings. It was a sort of playacting of today’s floating-fiat central bankers. But, I don’t see anything that really came of it. The results of this scurrying about were extremely minor, as we have seen. The broader picture was that currencies’ values were linked to gold, and that central banks did not deviate meaningfully from all that that implies.