We’re continuing our discussion of France in the 1920s and 1930s, and the France-blamers.

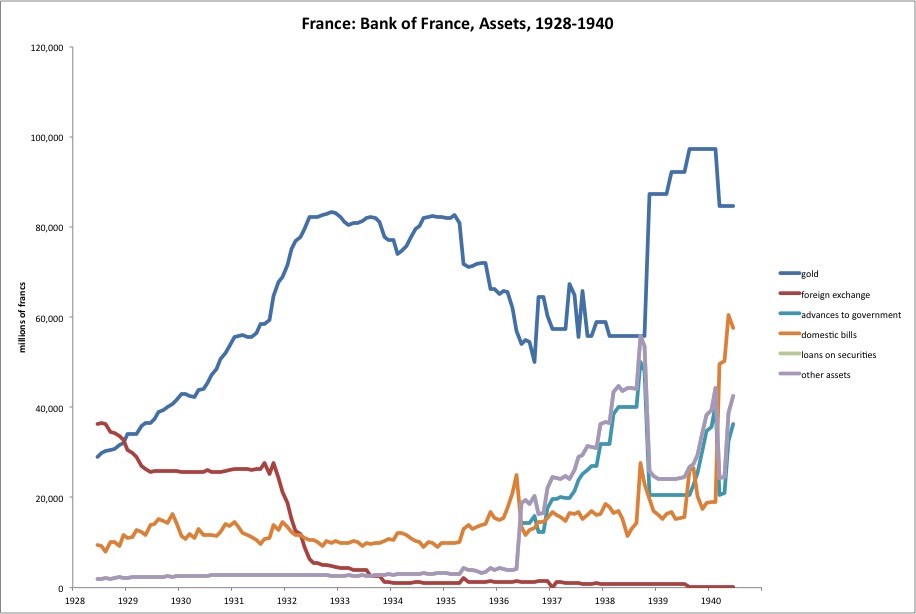

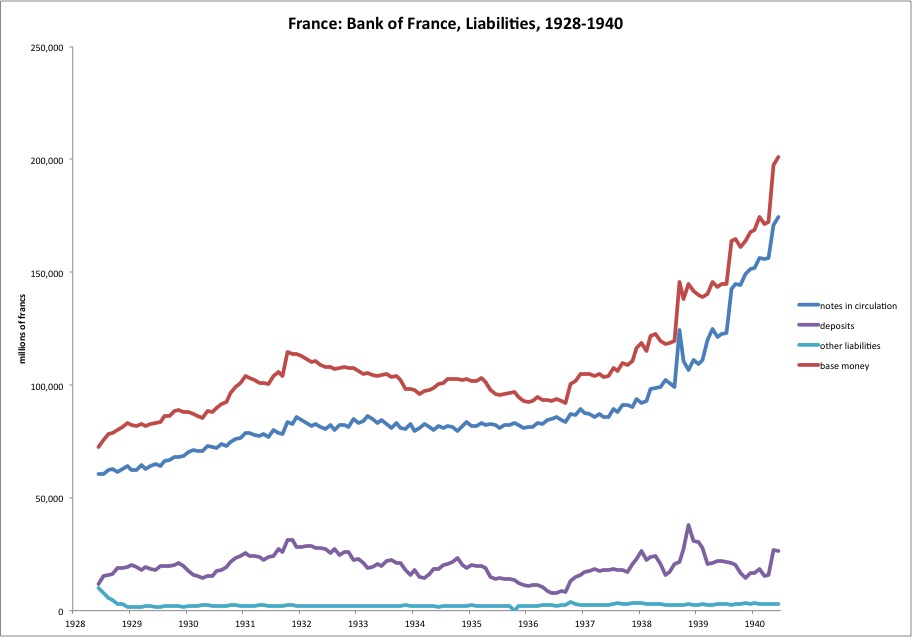

As a reminder, here’s what the Bank of France’s balance sheet looked like at the time:

When convertibility for the franc was restored in 1928, the Bank of France held a lot of foreign exchange reserves, here represented in red. They decided that they would rather return to their pre-1914 status, a time when they held a lot of gold bullion, and no foreign exchange reserves. So, in 1928-29, they began the process of selling off their forex reserves and replacing it with bullion. No big deal. They sold off the rest of the reserves after the British devaluation of 1931. (Not before — actually, in the leadup to the devaluation, the Bank of France was lending bullion to the Bank of England.)

In addition, gold reserves were rising due to conversion inflows. Base money was expanding concurrently.

This inflow/expansion is exactly what you would expect to see. France at the time had a very healthy economy, fueled by tax cuts in the 1920s. The currency was newly linked to gold, even with direct gold conversion restored, and thus became much more attractive than it was prior to 1926, when it was a floating fiat currency in freefall. Due to the decline in the value of the franc compared to its prewar gold parity, nominal prices would tend to rise, which would tend to drive further demand for francs.

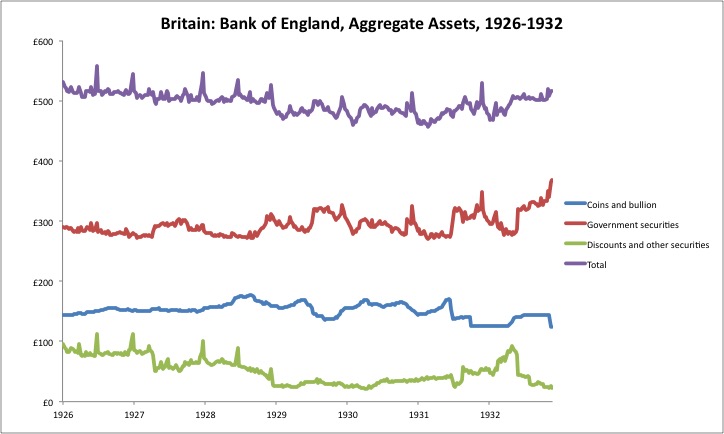

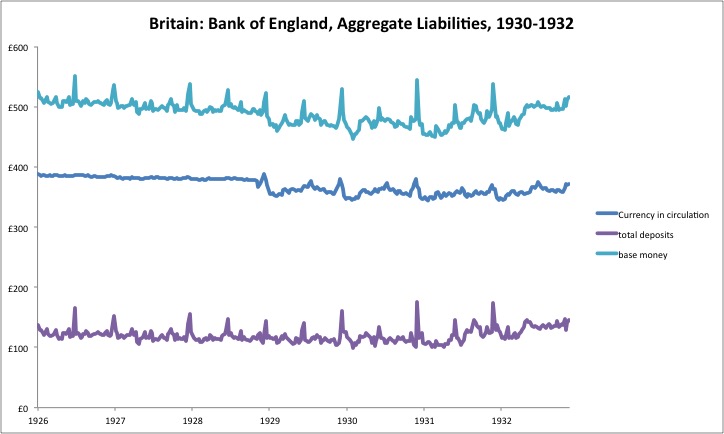

Now, let’s look at the Bank of England at the same time.

Here is the Bank of England’s balance sheet, shortly after the resupmtion of gold convertibility in 1925. Not much going on here. Everything is very, very stable. Too stable, actually — especially around the devaluation in 1931. The Bank of England made no meaningful defense of the pound in mid-1931, as we looked at earlier. Base money should have contracted by at least as much as the bullion outflows. Bullion outflows were actually at least 50 million pounds greater than shown here, because the BoE borrowed at least that much bullion during the crisis, from the Federal Reserve and Bank of France. In other words, there should have been a contraction of about 100 million pounds — about 20% of the 500 million total — due to bullion outflows. That didn’t happen.

May 22, 2016: The Devaluation of the British Pound, September 21, 1931

But, in the 1928-1929 period, we can see that not much was going on. There was a decline in bullion between mid-1928 and the end of 1929. However, most of this comes after the Bank of France is done with its conversion. The decline in bullion after mid-1928 looks to me like it had nothing to do with the Bank of France, and everything to do with the increase in government securities via discretionary open-market operations. In any case, it doesn’t matter much since the wiggles are minor, and by early 1930, bullion reserves are again at the high side of their range.

Base money drops a little here in 1928-1929, related to a reduction in currency in circulation, oddly enough. The funny wiggle in currency in circulation in mid-1928 seems to have something to do with an issue of banknotes by the government as a means of funding for World War I. This government (not BoE) banknote issue was consolidated onto the BoE balance sheet toward the end of 1928, which was probably accompanied by some sort of change in the status of banknotes, for example the ability to convert this government note issue to bullion with the BoE. The decline in base money doesn’t really mean anything — it was the automatic outcome of the mechanisms maintaining the gold parity value. If there was “not enough money,” the value of the pound would tend to rise, and base money would expand via bullion inflows, if not by some other factor.

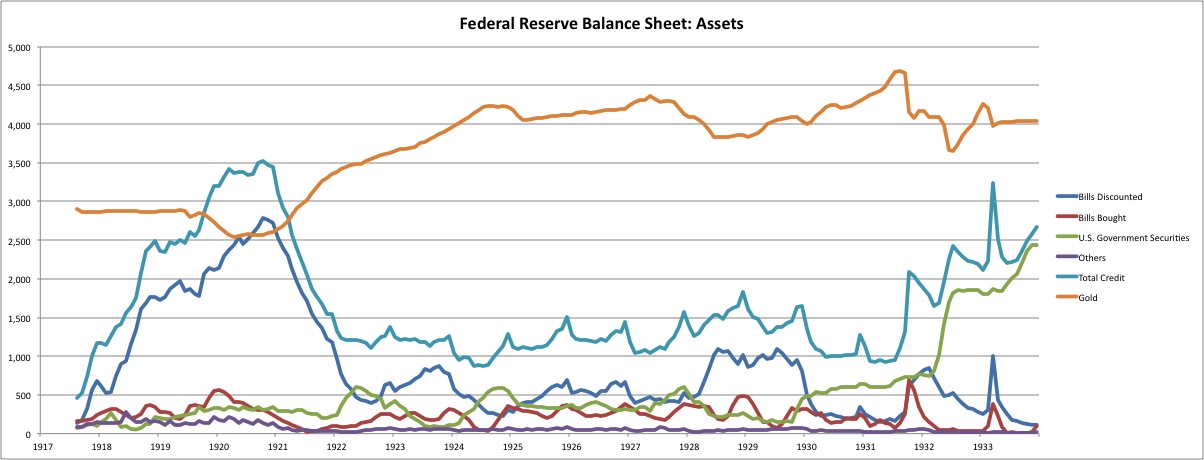

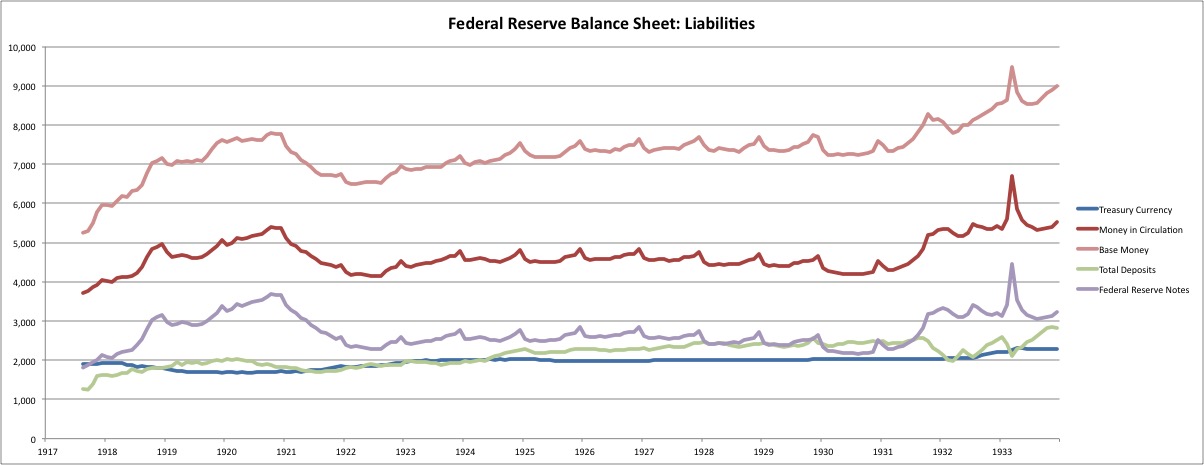

Now the Federal Reserve:

Bullion reserves at the Federal Reserve rise from mid-1928 to mid-1929. This has to do with the contraction in overall “Fed credit” (the combination of discounting and securities labeled “total credit”). The decline in bullion after September 1931 reflected both a decline in base money to support the dollar’s value, and also the dramatic expansion of “total credit” after September 1931 — including the bill-buying experiment of 1932, which we talked about here:

June 12, 2016: Milton Friedman Blames the Federal Reserve

Base money in the 1928-1930 period is very, very stable. Certainly no evidence of any disruption by anything done by France in 1928-1929 here.

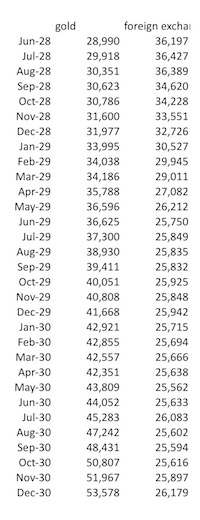

Here’s a look at that 1928-1929 reserve swap at the Bank of France — forex for bullion. (Figures in millions of francs.)

As you can see, forex drops by about 11 billion francs between June 1928 and June 1929. Gold reserves rise by almost the exact same 11 billion francs. Increases in gold reserves after that have nothing to do with the reserve swap, but rather represent conversion inflows.

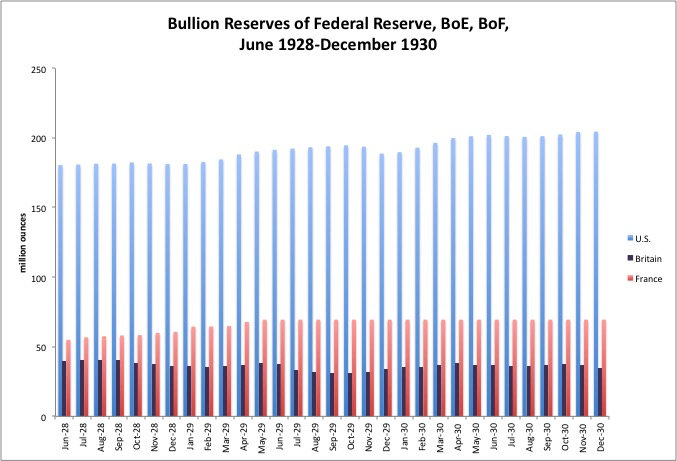

This is a bit of a funny chart. I wanted to isolate the Bank of France’s bullion swap of June 1928-June 1929. So, France’s bullion reserves rise until June 1929, then are a flat line. The actual reserves were still rising, but here I’m showing just the effects of the asset swap. France’s bullion reserves rise from 55.0 million ounces to 69.5 million ounces during this period — a rise of 14.5 million ounces. Britain’s fall from 39.9m oz. to 37.5m oz., a decline of 2.4m oz. They then fall further, after June 1929, to 30.8m oz. in October 1929. U.S. reserves rise from 180.6m oz. to 191.4m oz., an increase of 11.2 m oz.

We can see that the gold reserves increase in France did not come about by any meaningful reduction in the gold reserves of the U.S. or Britain. Where, then, did it come from? Ultimately, the same place that central banks had been drawing their increasing gold reserves for the eighty years previous — from the private market, including (but not limited to) miners. The notion that an increase in bullion at one central bank must come from a decrease elsewhere is completely wrong.

After all this talk of the minutiae of central bank balance sheets, it is probably natural to assume that they were somehow important. Mostly, however, they were not. The value of currencies were reliably linked to their gold parities. Overall base money was basically a reflection of the automatic adjustment process necessary to achieve that goal. Thus, if base money rises, or falls, or whatever — that was simply what needed to occur to maintain the gold parity. Whatever changes in base money happened to take place had no particular economic effects. A rise in base money was not “stimulative” or “inflationary”, and a decline was not “recessionary” or “deflationary.” Rather, the changes in base money reflect what was necessary to maintain the value of currencies at their gold parities — in other words, to keep them from being “stimulative,” “inflationary,” “recessionary,” or “deflationary,” as would result from a change in currency value. Likewise, changes in gold bullion reserves had no particular significance. It doesn’t really matter whether a central bank had more or less gold. The value of the currency — and the base money supply implied by that — remained the same. It seems that a lot of people have difficulties with these concepts. There seems to be an ingrained urge to take whatever minuscule wiggle happened to occur, and to somehow hang causality for giant economic events upon it. Resist this urge. It is not based on anything.

This discussion has become a bit more detailed than I expected. I think we will finally be ready to look at some of the Blame France-ers’ France-blaming in our next installment.