Gold Holdings of Central Banks and Governments, 1913-1941

August 10, 2014

We’re continuing our look at monetary conditions in the 1913-1941 period.

August 3, 2014: The Reichsbank, 1924-1941

July 27, 2014: The Bank of France, 1914-1941

July 20, 2014: The Bank of England, 1914-1941

January 26, 2014: The Federal Reserve in the 1930s #2: Interest Rates

January 19, 2014: The Federal Reserve in the 1930s

July 18, 2014: Foreign Exchange Rates 1913-1941 #8: A Brief Summary

December 23, 2012: The Federal Reserve in the 1920s 4: The Historical Record

December 16, 2012: The Federal Reserve in the 1920s 3: Balance Sheet and Base Money

November 25, 2012: The Federal Reserve in the 1920s 2: Interest Rates

November 18, 2012: The Federal Reserve in the 1920s

The source of our data is the Federal Reserve Banking and Monetary Statistics, 1914-1941.

http://fraser.stlouisfed.org/publication/?pid=38

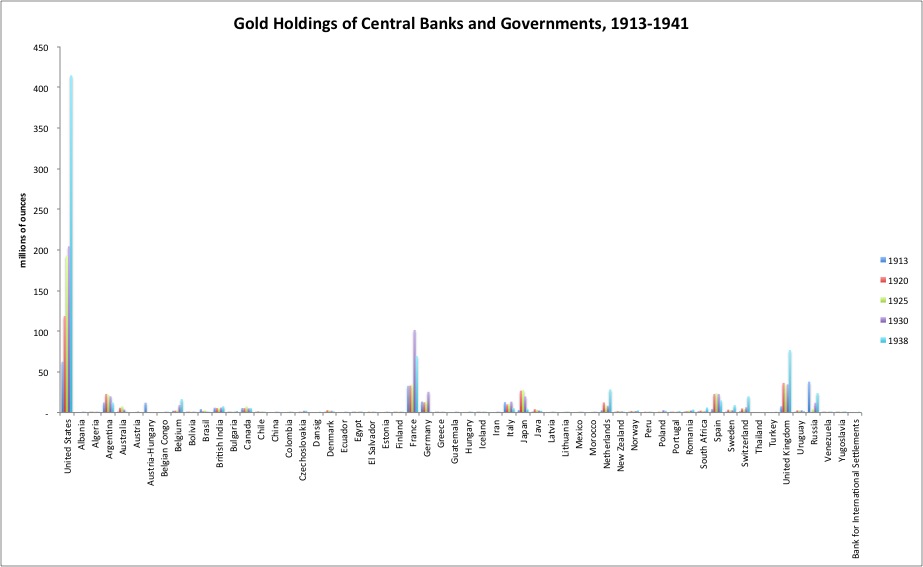

We’re going to start with some basic data. Alas, more analysis will have to follow later. Here is a chart of all the countries listed in the Banking and Monetary Statistics tables. We can see immediately that there are only a few countries with significant amounts of gold bullion. Remember, this is government and central bank holdings combined. I decided to focus on just a few, which I call the “majors”: U.S., France, Germany, Italy, Japan, Netherlands, Spain, Switzerland, and U.K. Russia was a biggie before 1913, but lost most of its gold during WWI and the Communist Revolution. The Soviet Union later rebuilt its gold bullion holdings to some degree, but I decided that wasn’t necessarily too relevant given that it was a Soviet system. Also, the Russia numbers are a little intermittent and unreliable. Argentina also held substantial gold bullion holdings, but I figured that Argentina was a somewhat peripheral country in any case. Despite holding less bullion than some others, I put Switzerland in the majors, in recognition of its special role during this period.

I should mention that these gold bullion figures don’t necessarily have the significance that many attribute to them. In practice, it doesn’t really matter that much whether a country has a lot or a little bullion, or whether that amount changes. What matters is the value of the currency, and whether functional mechanisms are in place to maintain a gold parity value. We’ve already looked at several major central banks up close, and also many histories of currency value.

This exercise is ultimately to demonstrate that, in fact, gold holdings are somewhat irrelevant. So, don’t go trying to project importance to them that they don’t have.

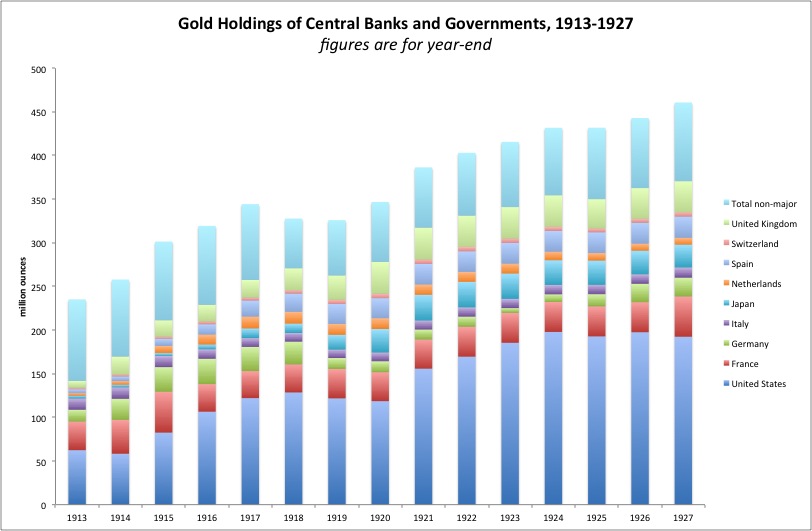

Our data source has annual data from 1913 to 1927, as of the year-end. One thing we see here is that central bank/government holdings, in aggregate, didn’t really change all that much during WWI, or the supposed “gold exchange standard” era of the 1920s. There’s a smooth rise throughout there, which is in line with mining production and the gradual rise of central bank/government holdings from about 1850 to a peak around 1950.

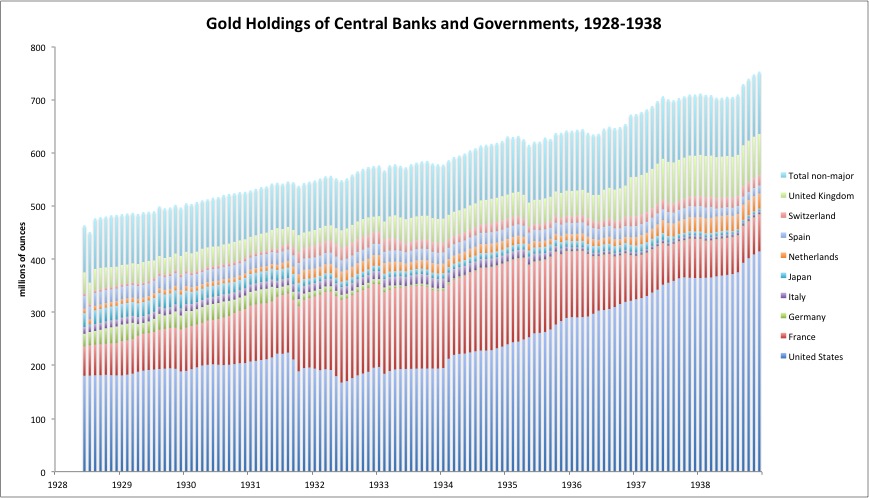

From mid-1928, we get monthly data, which is rather nice as this is the beginning of the Great Depression era, with all of the currency turmoil that we have been carefully documenting here. Again, despite all the excitement, there isn’t much change in the overall smooth trend of accumulation of gold bullion by central banks and governments. We’ve already looked at the increase in reserve holdings by France, which made perfect sense as their reserve holdings of government bonds were unfortunately being devalued at that time.

The data continues to 1941. However, after 1938, the onset of World War II, patchy data, and various reclassification schemes, make the data somewhat problematic. Besides, the concerns of war by that time are far more interesting. We’ve already seen some of the effects in our currency histories. So, we are stopping at the end of 1938 here.

That’s all for now. We’ll have more on this topic later.