(This item originally appeared at Forbes.com on December 14, 2022.)

Even though most adults today have lived all their lives within the floating fiat monetary system that emerged, accidentally, in August 1971, many today still probably find it rather strange that we spend so much time talking about the Federal Reserve’s current, ever-changing policy of macroeconomic manipulation, and that we actually allow this committee of mediocrities so much influence on our lives and well-being.

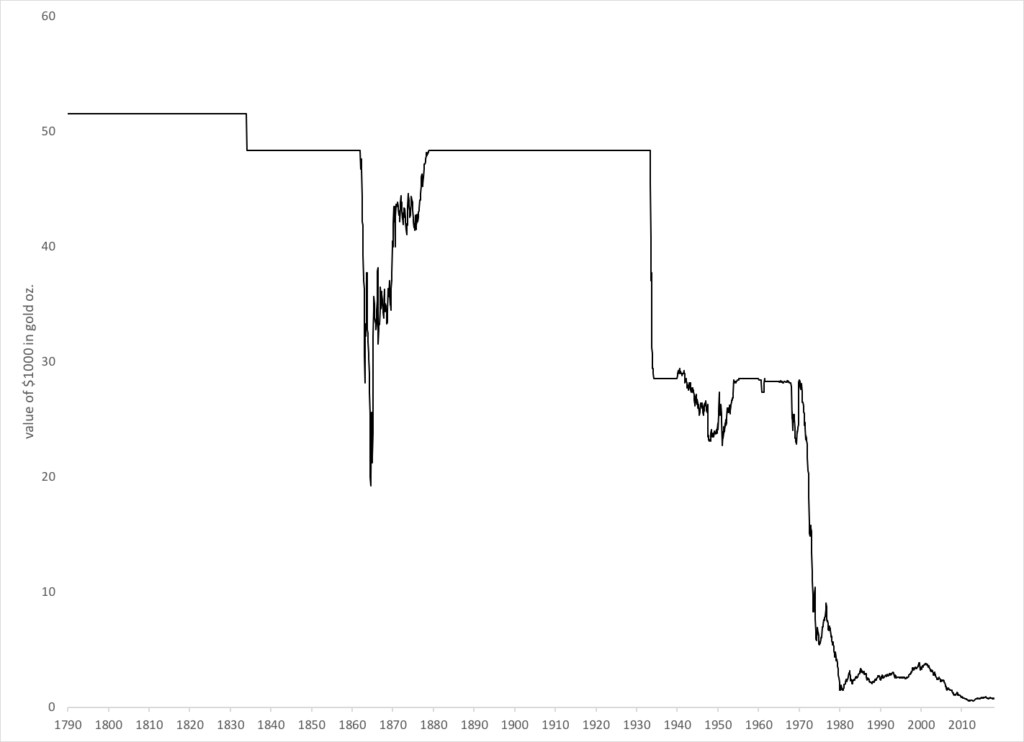

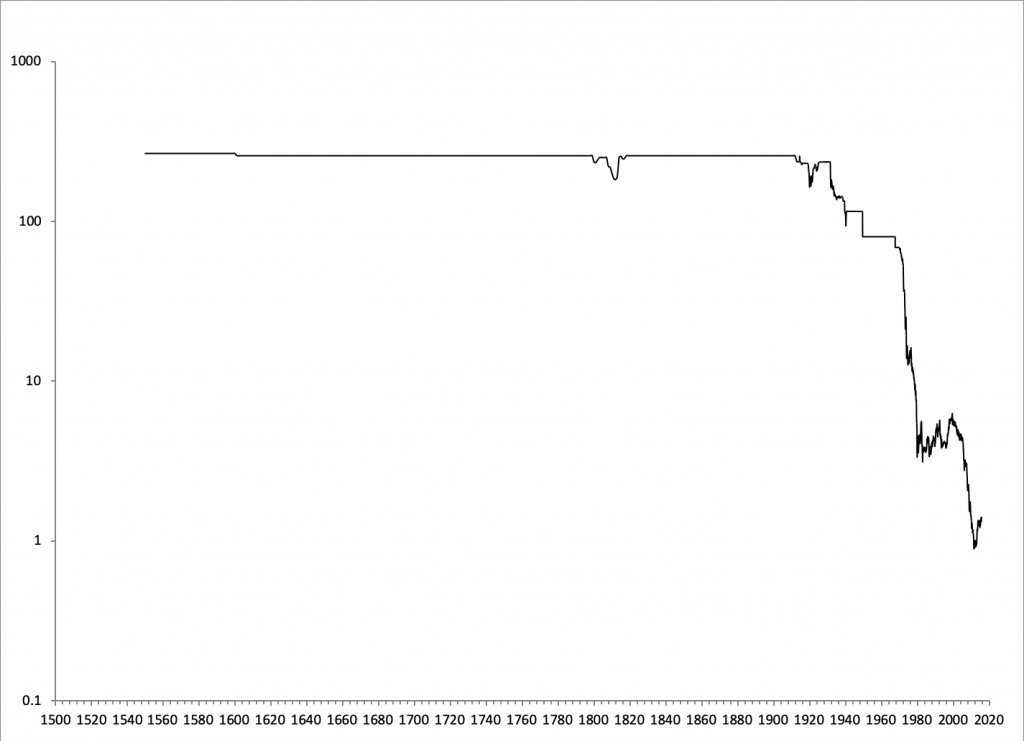

This is not how we did things for most of US history. Before 1971, we had a very simple policy: The value of the dollar would be linked to gold, specifically at $35/oz., the gold parity that Franklin Roosevelt defined in 1933-34. Before 1933, the dollar/gold parity was $20.67/oz. This had been our basic policy since 1789 (it is actually in the Constitution, in Article I Section 10), and it helped the United States become the wealthiest country the world had ever seen. Some people think that, even despite many technological advances, the US middle class has still never had it better than it did in the mid-1960s, when the dollar was “as good as gold.”

It wasn’t just the United States. Germany, Japan, Britain, France, Mexico — and even the Soviet Union and communist China — also linked their currencies to gold, in the 1960s. As long as the United States (and all the other countries) stuck to this principle, there never was a problem with “inflation.”

Today, it takes about $1800 dollars to buy an ounce of gold, not $35, as was the case during the Kennedy Administration. The US dollar today is worth about 1/50th of its prior value, compared to gold. (I call it “the two cent dollar.”) Just as it takes more dollars to buy an ounce of gold, it now takes more dollars to buy everything else too. This is the monetary sort of “inflation,” which has become chronic.

However, during all this time, from 1971 to the present, nobody was ever in favor of currency depreciation and “inflation.” During the 1970s, the 1980s, the 1990s, and continuing to today, everybody said the opposite. There seemed to be a lot of consensus about that. It just happened anyway.

What happened was: The Federal Reserve became politicized. People noticed that central banks could meaningfully affect the economy. This seemed like a wonderful solution. It didn’t seem to have any cost. It could bypass the slow, laborious and contentious legislative process. It could act quickly, in response to economic developments. It could get you elected, or re-elected. Richard Nixon, in his close presidential race with John F. Kennedy in 1960, blamed his loss in part on the Federal Reserve’s high interest rate policy, and a recession in 1960. With an election coming up in 1972, Nixon did not intend to repeat his error. Declaring that he was “now a Keynesian in macroeconomics,” Nixon leaned heavily on the Federal Reserve to resolve the 1969-1970 recession with “easy money.”

Congress’ new interest in macroeconomic manipulation was codified in the Employment Act of 1946. It said that it was the “continuing policy and responsibility” of the Federal Government to “coordinate and utilize all its plans, functions, and resources . . . to promote maximum employment, production, and purchasing power.” Basically, this is: “Growth” (or unemployment), and “Inflation” (or purchasing power), known as the Dual Mandate. Wikipedia notes that there is actually a third element in the Federal Reserve’s mandate, which is: To maintain low interest rates. (The Federal Reserve was very busy with managing interest rates directly in 1946, under instruction from the Treasury.)

Although the Employment Act of 1946 was directed at the Federal Government as a whole (including, for example, Keynesian “stimulus” spending), it was also adopted by the Federal Reserve. This came into direct conflict with the Federal Reserve’s policy of maintaining the value of the dollar at $35/oz. of gold, which resulted in the final blowup in 1971.

The Federal Reserve Act was amended in 1977 to impose the Dual Mandate upon the central bank directly. It required the Federal Open Market Committee (FOMC) to: “promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

In 1978, the Full Employment and Balanced Growth Act was passed, also known as the Humphrey-Hawkins Full Employment Act. This required the Federal Reserve to deliver a Monetary Policy Report to Congress twice a year.

Thus, we today have the Federal Reserve “Dual Mandate.” It is explicitly a program of macroeconomic manipulation. Its goals seem benign — a healthy economy, low “inflation,” and low interest rates. But the result has been: a program of constant macroeconomic distortion, ultimately resulting in a currency whose value is, it seems, only about a fiftieth of what it was when we started this nonsense.

It would seem that the “Dual Mandate” is a terrible way to manage a currency. It has led to a huge amount of ongoing “monetary inflation” (declining currency value), while not obviously improving economic outcomes. We still haven’t had a decade as good as that of the 1960s, when the dollar’s value was still stabilized by linking it to gold. Even the best decade since 1971 — the 1990s — was, according to leading Keynesians of the time, pretty weak tea compared to the 1960s.

Rather, I see the Dual Mandate as a pretty good description of the political pressures on politicians, which are then translated into pressures on the Federal Reserve. In an intensely politicized process of monetary policy, when we sweep away all the economic jargon, we see that the Federal Reserve careens between a “fix the economy” focus, and a “fix inflation” focus.

Bad Economics. But, Good Politics.

The outcome of this has been — more inflation, and a worse economy.

That’s why gold has always been the best basis of a currency. You just keep the value of the currency stable vs. gold. That’s the whole thing. (You can have small adjustments within this context, as the Bank of England had in the latter 19th century.) It doesn’t change. It is not political.

A currency then becomes an unchanging, neutral constant of commerce, like a meter or a kilogram. The meter doesn’t change in length. The dollar doesn’t change in value. This makes business a lot easier. We don’t have to adjust constantly to the Federal Reserve’s latest whims, and the distortions they cause. We just do business.

This is actually the way most countries today operate. They had independent floating currencies in the past, influenced by their local politics. It didn’t go very well for them either. They abandoned this, and adopted a simple external standard of value — typically, the USD or euro — thus depoliticizing their domestic monetary policy. This includes all the countries of Europe. Just look at the currencies of Italy, Greece, Spain or Portugal before the euro. Pretty ugly. The emerging market currencies were even worse.

Today, the IMF explicitly bans member countries from linking their currencies to gold. But, today some countries (Russia and China prominent among them) are thinking that maybe they can do without the IMF, and its various demands. Gold was money in Russia for many centuries, and it worked there too. China was on the gold standard during the Han Dynasty (202 B.C. to 220 A.D.), and also in 1970. Depoliticizing money will mean abandoning the Dual Mandate. Good riddance.