(This item originally appeared at Forbes.com on December 6, 2019.)

“Please God, make me good … but not yet!” said Augustine of Hippo (354-430), on his way to eventually becoming a saint of the Catholic Church. He was trying to overcome the temptation of “concubinage,” or women of easy virtue, which were common in the breakdown of Roman society in the late fourth century. Augustine was eventually successful, and helped establish Christian morality as it existed for the next 1500 years.

It is becoming increasingly apparent that the “PhD Standard” has not, and will never, provide a stable, reliable, and uniform monetary system, upon which rational economic calculation and rising prosperity can be based. Instead, the PhD types seem to be getting ready to double down on the sort of silliness that hasn’t worked very well thus far, and might lead to eventual disaster.

These academics and central bankers with PhDs remain very eager to convince anyone who will listen why they really, really should be allowed to manage our monetary systems. Mostly, this is because their very, very good ideas will help to fix the problems left by the last generation of PhD-bearing money manipulators. These range from CPI targeting fans to the advocates of “Modern Monetary Theory.”

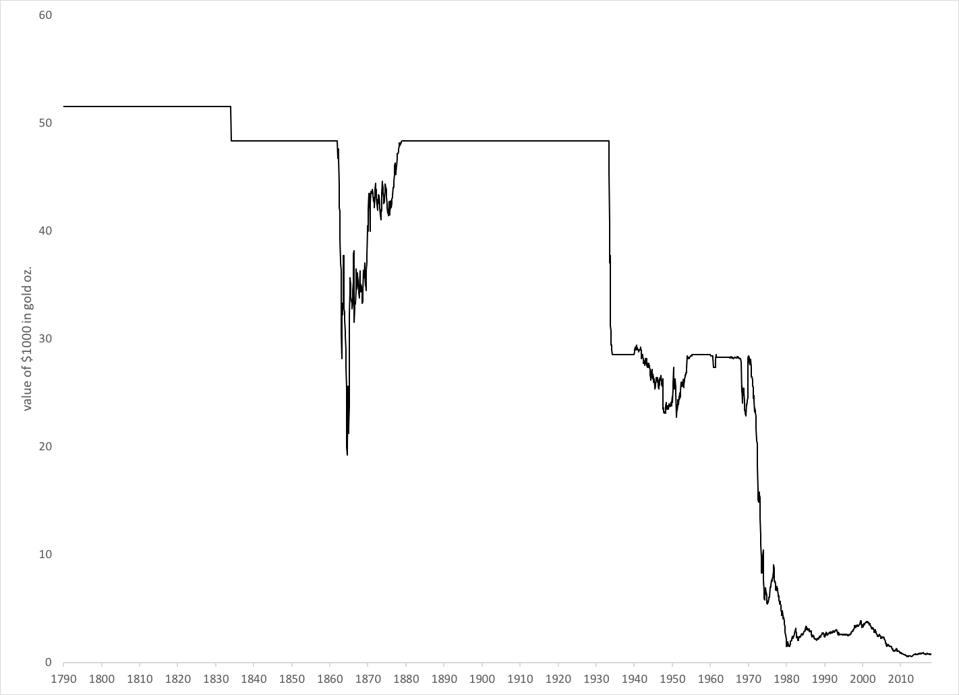

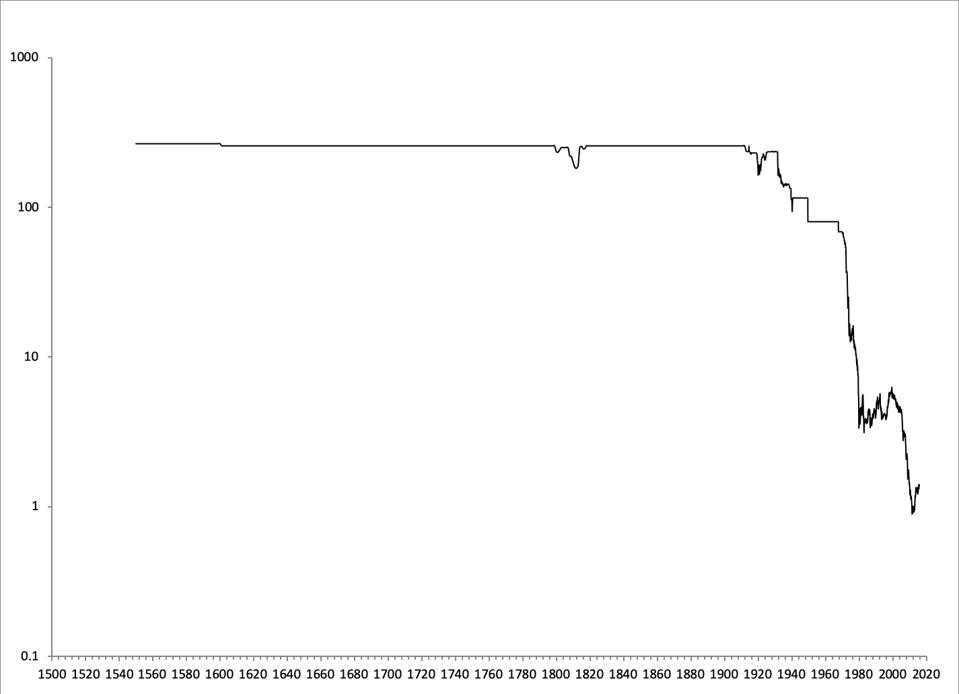

But, there is another group of leaders — I call them “the grownups” — that seems to be looking at these claims with increasing skepticism. These are generalist leaders, such as presidents and prime ministers, the leadership of China, the higher-minded elements of the “Deep State” within the CIA, NSA or Kremlin, and military men who regard economic performance as an important part of national security. These people can see the obvious: The world gold standard system worked very well, over a period of centuries prior to its dissolution in 1971, and we don’t seem to have developed any viable alternatives since then. It seems like today’s national leaders are gradually reaching a consensus about how the world’s monetary system should be structured. They are getting ready to return to a gold standard system.

But, not yet.

Jim Reid, “Global Head of Thematic Research” at DeutscheBank, recently suggested that fiat currencies might disappear before 2030. Reid said that gold — the “Once and Future Money” — is a likely successor. As a high-profile representative of current Davos-set thinking, he is worth quoting at length:

We have lived in an era of fiat money since the early 1970s. Since then virtually all money in existence has only had a value based on trust and, in particular, trust in governments’ ability to maintain its value. Prior to this period, most of the money in existence through history was backed by a commodity – usually a precious metal like gold or silver. When money broke loose from such an arrangement inflation tended to increase (often dramatically), and when money returned to it inflation was becalmed. We think fiat money systems should be inherently unstable and prone to high inflation all other things being equal. Politically it is always too tempting to create money when nothing is backing it. … The forces that have held the current fiat system together now look fragile and they could unravel in the 2020s. If so, that will start to lead to a backlash against fiat money and demand for alternative currencies, such as gold or crypto could soar.

Malaysia’s prime minister Mohammad Mahathir recently restated his long-held desire for an international currency system based on gold. Mahathir has served as a representative of both the smaller Asian countries, and also the Islamic world. Some people think that Muammar Qaddafi of Libya was deposed in part because he was aiming to establish a pan-African and pan-Islamic gold-based currency.

China and Russia have been making gold-friendly statements for years, backing this up with an apparent agenda to increase their gold bullion reserves.

President Trump has consistently favored gold standard fans. He has nominated three — Stephen Moore, Herman Cain and Judy Shelton — to the Federal Reserve. His economic advisor Lawrence Kudlow, vice-president Mike Pence, and Trump-appointed World Bank president David Malpass, have also indicated their friendliness toward the idea.

Jim Rickards, also a member of the Davos set, suggested in Aftermath (2019) that a “Mar-A-Lago Agreement” may be in our future, similar to the Bretton Woods Agreement that re-established the world gold standard in 1944. Actually, a better location would be Trump’s Doral Resort in Florida, recently proposed as a site for a G7 international monetary meeting in 2020.

People have tasted the consequences of monetary immorality. They are getting ready to be good again.

But, there is a problem. To establish a worldwide gold standard system today would mean that all existing debts and commitments — government bonds, Social Security, Medicare, public and private pensions, State debts and commitments — would have to be paid back in hard money, or renegotiated.

This can be done. The British government had debts estimated at 178% of GDP at the end of the Napoleonic Wars in 1815. Debt service costs absorbed 53% of central government tax revenue. It would have been an easy matter to attempt to get out of these by devaluing the British pound, which had been a floating currency for eighteen years by that point. Many promoted exactly this solution. But, instead the pound was returned to gold, taxes were reduced, spending was slashed, Britain became the most successful developed country of the nineteenth century, and, due mostly to rising GDP, the debt/GDP ratio eventually fell below 30%. (I describe this in more detail in The Magic Formula.)

Today, we do not seem to have that degree of fortitude. The political battles — to reform healthcare, the welfare system, Social Security, the bad habit of chronic deficits, the underfunded pensions, the bankrupt States, the student loans, the tax system — seem insurmountable. Congress, squandering years with Russiagate and impeachment, does not seem able to accomplish anything at all. The urge to maintain the status quo is intense. Britain did not have any kind of welfare system in the early nineteenth century, with all the complications and expectations that involves. I sense (along with Jim Reid) that with our growing political consensus around a long-term gold standard solution, we are also coming to a consensus about a short-term period of housecleaning — a cutting of the Gordian knot, a cleaning of Augean stables — in which all these issues are, in effect, made irrelevant by the printing press. Isn’t that exactly what the “modern monetary theory” people are promising? Basically, this is the period that, in Rickards’ book, comes before the meeting in Florida.

If that’s the way we’re going to do it, then so be it. Let’s try to keep things from getting too out of hand. Life in Argentina is still tolerable today; life in Venezuela is not. And then, afterwards, after the lessons have been learned and the decrepit old institutions are no more, let’s re-establish the world gold standard system.