What is “Hyperinflation”?

October 13, 2013

What is “hyperinflation”?

The word is tossed around, and many have an opinion about it, without having any real clear idea of what it means.

We all probably have some mental picture of the “billion dollar banknote” or “price of coffee rises as you drink it” kind of hyperinflation, as happened in Germany especially in 1923.

But, this is somewhat rare. Not as rare as you might think, but it constitutes only a small portion of those events which I think are legitimately labeled “hyperinflation.”

This table lists fifty-three of the most intense hyperinflations in recent history:

The Hanke-Krus Hyperinflation Table

The least intense hyperinflation listed on this table is a 55.5% increase in “prices” in a month in Kazakhstan in 1993, which works out to a doubling of prices every 47.8 days. However, this table leaves out many hundreds of events which are legitimately called “hyperinflation” in my opinion, and in the opinion of those who lived through them, and historians.

You see what I mean when I say that it is “not as rare as you might think.”

Here’s Wikipedia on various hyperinflations:

Wikipedia on hyperinflations

Extreme hyperinflations like these tend to grab people’s attention. However, I would suggest that they are actually less relevant than some milder cases. Let’s say you start with the price of a cup of coffee at $1. After a few years, the price of the cup of coffee is $100. I say that most of whatever is going to happen has already happened by that point. The “purchasing power” of $1 has already declined by 99%. There actually isn’t much difference between a cup of coffee that goes from $1 to $100, and from when it then goes to $1000, or $1 million, $1 billion or $1 trillion. It’s just the last bit from 99% to 99.999999% loss of “purchasing power.” I call it the “final clownshow.” Many countries never get there.

There is no particular dividing line between “inflation,” as the U.S. experienced in the 1970s, and “hyperinflation.” It is somewhat arbitrary. However, there is a point at which certain things begin to change, which I think is a legitimate point at which to add the “hyper-” prefix.

I’m using the word “inflation” here too as it is popularly conceived. These terms don’t have clear definitions. Although I can apply clear definitions to them, and have in the past (in my book Gold: the Once and Future Money), nobody else shares my definitions. I now think it is best to avoid them altogether, or, to use them as others might understand them, in a vague and casual way.

The International Accounting Standards Board, which is the general rule-maker for accounting worldwide, has a specific definition of “hyperinflation.” IAS 29 says that hyperinflationary accounting standards apply when “the cumulative inflation rate over three years is approaching, or exceeds, 100%.” By “inflation rate” they basically mean the official Consumer Price Index. FASB, the standards-making body for U.S. accounting, has the same definition as the IAS.

Wikipedia on Inflation Accounting

Thus, for them, “hyperinflation” is a rise in the CPI of 100% or more over a period of three years. It works out to 26% per year compounded, or 2.0% per month.

Two percent a month. Which probably doesn’t seem very “hyper-.” It certainly doesn’t make the price of your coffee go up in the thirty minutes it takes to drink it.

But, the IASB is not just throwing out these definitions on a whim. This is based on real-life experience, of many corporations that have had to deal with accounting in situations of hyperinflation. For example, in the 1980s, essentially all of Latin America — pretty much everything south of Texas — experienced hyperinflation. The Latin American subsidiaries of Coca-Cola, for example, had to ask for guidelines on how to do their accounting in this environment. So, this admittedly arbitrary definition is nevertheless based on an enormous amount of real-life experience.

When you get annual CPI rises on the order of 26% per year, over a period of three years — the minimal requirements of “hyperinflation” according to IAS 29 — certain essential elements of the modern market economy start to break. For example, accounting breaks. Here’s Wikipedia on some of the problems I’m talking about:

Historical cost basis in financial statements

Fair value accounting (also called replacement cost accounting or current cost accounting) was widely used in the 19th and early 20th centuries, but historical cost accounting became more widespread after values overstated during the 1920s were reversed during the Great Depression of the 1930s. Most principles of historical cost accounting were developed after the Wall Street Crash of 1929, including the presumption of a stable currency.[3]

Measuring unit principle

Under a historical cost-based system of accounting, inflation leads to two basic problems. First, many of the historical numbers appearing on financial statements are not economically relevant because prices have changed since they were incurred. Second, since the numbers on financial statements represent dollars expended at different points of time and, in turn, embody different amounts of purchasing power, they are simply not additive. Hence, adding cash of $10,000 held on December 31, 2002, with $10,000 representing the cost of land acquired in 1955 (when the price level was significantly lower) is a dubious operation because of the significantly different amount of purchasing power represented by the two numbers.[4]

By adding dollar amounts that represent different amounts of purchasing power, the resulting sum is misleading, as one would be adding 10,000 dollars to 10,000 Euros to get a total of 20,000. Likewise subtracting dollar amounts that represent different amounts of purchasing power may result in an apparent capital gain which is actually a capital loss. If a building purchased in 1970 for $20,000 is sold in 2006 for $200,000 when its replacement cost is $300,000, the apparent gain of $180,000 is illusory.

Misleading reporting under historical cost accounting

“In most countries, primary financial statements are prepared on the historical cost basis of accounting without regard either to changes in the general level of prices or to increases in specific prices of assets held, except to the extent that property, plant and equipment and investments may be revalued.”[5]

Ignoring general price level changes in financial reporting creates distortions in financial statements such as[6] reported profits may exceed the earnings that could be distributed to shareholders without impairing the company’s ongoing operations the asset values for inventory, equipment and plant do not reflect their economic value to the business future earnings are not easily projected from historical earnings the impact of price changes on monetary assets and liabilities is not clear future capital needs are difficult to forecast and may lead to increased leverage, which increases the business’s risk when real economic performance is distorted, these distortions lead to social and political consequenses that damage businesses (examples: poor tax policies and public misconceptions regarding corporate behavior)

Another thing that often breaks is the financial system. This is generally not a matter of bank insolvency or default, but rather one of lenders and borrowers being able to work together. At an annual CPI of 26%, you might expect that lenders won’t lend except at an interest rate of more than 26%, and on very short terms of under a year, because nobody knows what might happen next. What tended to happen in Latin America in the 1980s is that domestic-currency lending dried up altogether. Typical interest rates actually soared well above the CPI rate, to 100% or more, for small-scale borrowers, like small local businesses. Naturally, volumes shrank to a pittance. It basically became a form of loan-sharking, taking advantage of a desperate few. On the larger scale, the economy was capital-starved. What lending existed was done in foreign currencies, although even that was usually among larger and well-established corporate borrowers primarily. The local, small scale economy basically was finance-free.

Other things break, like any sort of long-term contracts or agreements. Wage agreements and contracts for services have to be renegotiated several times a year. Public and private pensions, annuities, life insurance, and of course any kind of long-term bonds or lending becomes worth a lot less, or even worthless. The tax system might break, either taxing at much too high a rate (for example, on corporations who seem to have enormous “profits” because their cost-of-goods-sold is based on FIFO accounting, or capital gains based on years-ago purchase prices), or too low (for example, on regular income, which is paid on April 15 for the entire previous year, in a dramatically devalued currency with very little current value).

Actually, the IASB described hyperinflation in these terms:

The International Accounting Standards Board does not establish an absolute rate at which hyperinflation is deemed to arise. Instead, it lists factors that indicate the existence of hyperinflation:

The general population prefers to keep its wealth in non-monetary assets or in a relatively stable foreign currency. Amounts of local currency held are immediately invested to maintain purchasing power;

The general population regards monetary amounts not in terms of the local currency but in terms of a relatively stable foreign currency. Prices may be quoted in that currency;

Sales and purchases on credit take place at prices that compensate for the expected loss of purchasing power during the credit period, even if the period is short;

Interest rates, wages, and prices are linked to a price index; and

The cumulative inflation rate over three years approaches, or exceeds, 100%.

In other words, things start to break. Not only the things listed here start to break. These are just a few of a great many elements of the money economy that stop functioning properly when the money goes bad.

One reason I called the 1970s experience in the United States “inflation” rather than “hyperinflation” is that these things didn’t break. Interest rates rose to mid-teens levels, but the financial system didn’t dry up and blow away as it did in Latin America. The U.S. income tax system, which was not automatically indexed to inflation in those days, was on its way to choking off the economy altogether as the middle class rose into tax brackets intended for the very wealthy. But, it didn’t quite get there. Things almost broke, in the 1979-1980 time, but that’s when Paul Volcker panicked and did whatever he had to do to avoid that outcome.

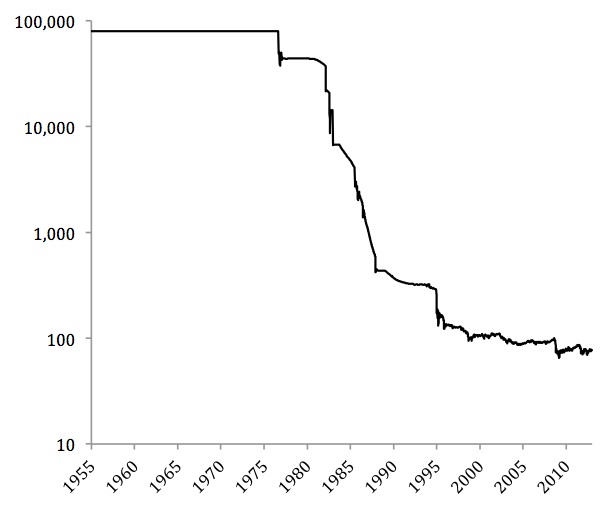

Here’s what hyperinflation looked like in Mexico during the 1980s:

Value of 1000 Mexican pesos (1 million pre-1993 pesos) in U.S. dollars, 1955-2012

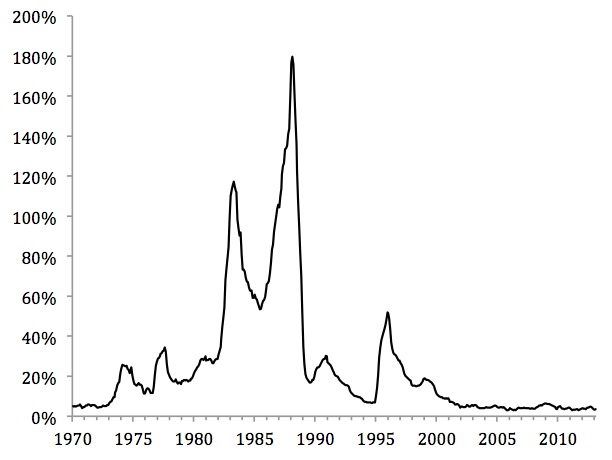

Between 1982 and 1988, the value of the peso went from 26/dollar to 2,300/dollar; in other words, a decline in the exchange value of the peso by about 100:1 during those six years. (In 1993, they knocked three zeros off the peso.) The official Mexican CPI looked like this:

Mexico: Official CPI, YoY% Change, 1970-2012

The official CPI rose by an annual rate of between 55% and 180% during that time period, typical throughout Latin America during this era. This fits the IASB definition of “hyperinflation,” and indeed that’s what Mexicans called it at the time. However, even the peak 180%/year rise works out to 8.9% per month, which maybe doesn’t strike people as very “hyper.” Nevertheless, if the value of your pensions, savings, bonds, etc. fell by a factor of 100:1 over six years, you would be a little peeved. If your $100 pension was then worth only $1, it wouldn’t really matter that much if it then went from $1 to $0.10 or $0.01, and at what rate of speed that might happen. That’s why I say most of the action happens in the first 100:1, and the rest is just the “clownshow at the end.” In the case of Mexico, it never got there. In 1988, the value of the peso was stabilized against the dollar and the hyperinflation ended, although the peso did have another incident in 1995.

The worst thing about “the clownshow at the end” is not really the “rate of inflation,” which is not actually so relevant. It is really the time lost. By this point, the economy is reduced to subsistence. Things are very difficult. People are just trying to get enough to eat. This can go on for a few months, or it can go on for several years. It’s the time — the time spent in this period of despair and bare subsistence — that is the real “cost” of hyperinflation at that point.

These kinds of IASB-defined hyperinflations don’t even show up in the Hanke-Krus table or Wikipedia’s list of hyperinflation events, although they are certainly hyper-destructive. There are also many examples of currencies, like the Turkish lira, which decline by a 30%-50% rate every year, fitting the IASB definition of hyperinflation, for perhaps decades at a stretch.

There’s more. Japan had a hyperinflation in the 1945-1950 period, when the value of the yen went from about 4/dollar to 350/dollar. This again was about a 100:1 devaluation, much like that of Mexico, in about the same time period. It doesn’t show up in these lists. There are also some other events. The French Franc was worth 40/dollar in 1939, and 350/dollar in 1949. This was not quite hyper, but it was still a 10:1 devaluation over a period of ten years. At 26% per year, it is right on the borderline of the IASB definition of “hyperinflation.” (Actually, most of this appears to have been after 1945, because during the German occupation, the value of the franc was fixed at 20/mark, and the mark was worth, in prewar terms, about 2 marks/dollar. This would compress the French hyperinflation into the 1945-1950 period, or 10:1 in only five years, or 58% per year.) France also had about a 5:1 devaluation during and soon after WWI, not quite hyper but quite significant nonetheless.

The Italian lira was 20/dollar in 1941, and 625/dollar in 1950, a 30:1 devaluation in eight years (53% per year). (The U.S. dollar was worth $35/oz. of gold in both 1939 and 1950, roughly speaking.) Italians had other things to worry about besides the value of their money; it wasn’t the only thing that was destroyed in the war years. But, nevertheless, it was a hyperinflation event that generally isn’t remembered by historians. Germany also had another hyperinflation after WWII, again in the 1945-1950 period.

What I find is that, basically, all the countries in the world have experienced some sort of hyperinflation in the last 100 years. All of them! The exceptions are basically the anglo-speaking countries: Britain, the U.S., Canada, Australia and New Zealand. That’s one reason that understanding and experience of hyperinflation is rather poor in the English-speaking world, but rather familiar in the Spanish-speaking world. We think it doesn’t happen often because the anglo-speaking countries — just five out of the 150 or so countries in the world — haven’t had it in the last 200 years. (Actually, there was hyperinflation in the Confederacy during the Civil War.) But, in the rest of the world, it has been drearily familiar.

The reason that there hasn’t been hyperinflation in the anglophone world is because of the tradition of Hard Money embraced by the British and the American colonies that became the United States. This is why Britain, and then the United States, became the leaders of the world monetary systems of those times, with the premier international “reserve” currencies. But, as we can see, this tradition has been getting rather soft recently. The anglophone world is starting to look a lot like … the rest of the world in these matters. Maybe the U.S., Britain etc. are even leading things in this regard, while the Chinese and others say “stop!” Even Brazil, a serial hyperinflationist, is saying stop (with Chinese prompting).