We have been talking about The Midas Paradox (2015), by Scott Sumner.

July 23, 2017: The Midas Paradox (2015), by Scott Sumner.

As you probably guessed from the three-word title, the book can be summarized in two words, which are: “blame gold.”

This, as we have seen, is actually a relatively new notion, even if it enjoys some popularity today. The general consensus, which later (after 1950) became the Keynesian consensus, did not blame gold, or indeed, monetary policy in general, for the Great Depression. They often recommended a devaluation, or some sort of “easy money” policy perhaps involving “lower interest rates,” as a solution for the problems of the day, but did not see the problems arising from monetary issues themselves. Rather, it was a “decline in aggregate demand,” a non-explanation for sure, but one that was inherently non-monetary in nature. For a single product — let’s say it is pickup trucks — a decline in “demand” (fewer purchases) would lead to falling nominal prices for pickup trucks, which would then result in declining production of pickup trucks. All of this happens with money of an assumed stable value. This was later extended to economies as a whole: a decline in “aggregate demand” (for all products) leads to falling nominal prices, which then results in declining production (“aggregate supply”, or Gross Domestic Product), again all within a context of stable money value.

The idea that the Great Depression had significant monetary causes became popular in the 1960s. The “Austrian” version, described by Murray Rothbard in America’s Great Depression (1963) although it reflected the opinion of Austrians during the 1930s, suggested an “inflationary bubble” caused by some sort of Federal Reserve misbehavior, which then collapsed into catastrophe. The “Monetarist” version, described by Milton Friedman and Anna Schwartz in A Monetary History of the United States, 1867-1960 (1963), suggested a “deflationary collapse” also caused by some sort of Federal Reserve misbehavior. Both assume that the U.S. dollar was essentially a floating fiat currency, in which the Federal Reserve had great discretionary powers; powers used to inflate a “bubble” of the most destructive consequences in the 1920s, or powers to cause the most horrible “deflation” in the 1930s, in both cases largely absent of other causes. Neither of these views “blame gold,” since gold doesn’t play any meaningful role in either narrative. They both tend to ignore the fact that the gold standard existed at all. Mostly, they are about credit, not money. The Keynesians today assert that the “golden fetters” of the gold standard in fact prevented central banks from taking much meaningful discretionary action, either “inflationary” in the 1920s or “deflationary” in the 1930s. (This is correct.)

I see the popularity of explanations involving monetary causes to be a natural outcome of the “Prices, Interest, Money Box” that economists got themselves into beginning in the 1870s, and in which they are still largely stuck today. The “decline in aggregate demand” description is dangerously close — I would even say, functionally identical — to “it just happened.” There is no cause-and-effect, it is just some sort of mysterious nothing out of nowhere. If a “cause” is identified, it is usually some sort of heebie-jeebies related to the large decline in stock prices in 1929. Stocks go down — we get the heebie-jeebies — the world economy craters, a Lost Decade ensues, and World War II follows along afterward. Right. Not surprisingly, this became very irritating, not to mention, a great opportunity for careerist academics: certainly there was an identifiable cause of the Great Depression.

But, if you are limited to Prices, Interest, and Money, it becomes hard to say what that cause, or causes, were. There were some issues with “sticky prices,” including wage controls and also some price fixing. But most “prices” did indeed go down, including wages (a 17% decline between 1930 and 1933), without seeming to relieve the Depression’s intensity. It is hard to affix primary blame for such a dramatic event on the minor price-related policies that can be identified. Interest rates were largely market-determined, and fell to very low levels. Among possible candidates for causes of Great Depression-scale magnitude, this left only Money on this limited list of options. Rothbard and Friedman represented popular attempts to make Money fill that guilty role — the role which, prior to 1960, it was usually thought to have been innocent of.

Over time, I think that people sort of understood that you couldn’t just ignore the gold standard, and assume that the Federal Reserve (and other central banks) were operating what amounted to a highly discretionary floating fiat currency. Even if you did assume that, the actual behavior of central banks (their balance sheets) does not really support either Rothbard or Friedman’s claims. Thus, during the 1980s, if you wanted to Blame Money — which is really the only thing you can blame when you are in the Prices, Interest, Money Box — you would have to blame the gold standard.

This took two forms. One was that there was some sort of convolution, some sort of tricky something-or-other (“imbalance,” “asymmetry,” “transmission mechanism”), some kind of violation of the “rules of the game,” by which central banks were either violating gold-standard operating principles, or perhaps, that those principles themselves had some sort of inherent error. Mostly, they try to Blame France. This arose because people did not really understand how gold standard systems operate — it is basically an automatic system similar to a currency board, which I go into in great detail in Gold: the Monetary Polaris, and also in Gold: the Final Standard. Not understanding it, and befuddled by a variety of fallacious and confusing notions regarding some sort of “rules of the game” or “price-specie flow mechanism,” and desiring to somehow Blame Money (within the Prices, Interest, Money box) and finding themselves thus required to Blame the Gold Standard, they could make it into a boogeyman to serve all purposes. But, the fundamental principle of the gold standard was certainly that the currency’s value should be linked to gold, at a fixed parity rate. Central banks did this, quite effectively, even in a difficult crisis environment. If they were doing something wrong, shouldn’t it have resulted in a deviation in their currency’s values from gold parities — especially since they were under considerable stress and difficulty? Or, if they were actually doing something wrong, it must not have mattered very much, because gold parities were maintained. Although people still do not understand these principles very well, I think that over time they came to understand that it is hard to blame some kind of mismanagement of the gold standard for the Great Depression when this supposed mismanagement did not even result in a deviation of currencies from gold parity values. When there was actual mismanagement — basically leading to the British devaluation in 1931, as we documented in detail — they all stand up and cheer.

May 22, 2016: The Devaluation of the British pound, September 21, 1931

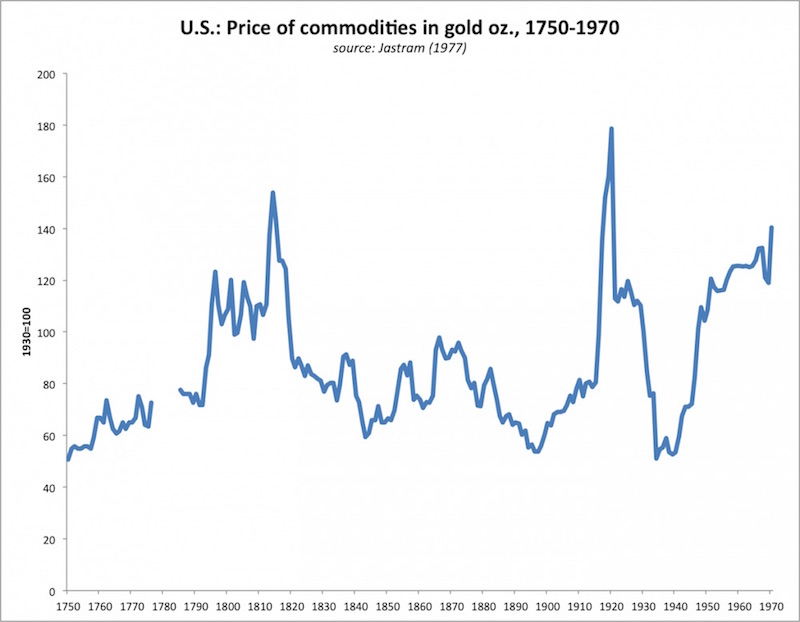

This leads us to what I have been saying from the beginning is the only real line of argument one can take in these matters — that gold’s value deviated by some amount large enough, and quickly enough, to cause a major economic upset. Since the general tenor of the time was “deflationary,” this implies that gold’s value would have had to rise. This rise could not be some little wiggle like 10%. In our floating fiat era, we have currencies going up and down 10% against each other (or against gold, or against commodities) all the time, and although the effects of this are sometimes noticeable, this does not cause Great Depressions. I posited that you would have to have a rise in gold’s value on the order of 100% — that is, a doubling. Maybe more than a doubling, since even when currencies have doubled in value in a short period of time, such as the rise of the Japanese yen from 260/dollar to 120/dollar between 1985 and 1988, this has not caused anything resembling a Great Depression.

The problem with this claim is that there is no history of it ever happening in 500 years of data of commodities vs. gold. There are only two big declines in commodity values vs. gold during that time, which might (or might not) be an indication of a major rise in gold’s value. (The decline in commodity prices vs. gold since 1970 constitutes a third such episode, although not particularly relevant since no currencies were linked to gold.) The first was in the 1880-1895 period. However, this was also a time of aggressive expansion of commodity supply, and I think it probably represented a commodity glut rather than a rise in gold’s value. Others have said the same. Also, it was a time of great economic expansion — including great expansion of commodity production, which wasn’t too good if you were a commodity producer trying to sell your wares on a glutted market. There were also some “demand” issues, particularly around 1890-1896. This was the time of the Barings crisis (1890), and also two Panics (1893 and 1896) in the U.S. related to the threat of the devaluation of the dollar due to “free coinage of silver” arguments. Once this risk was off the table with McKinley’s win in 1896, the economy soared.

The second event was in the 1930s. The conclusion reached by most economists over the decades was that this was also a market “glut”, this time caused by a collapse in commodity demand, rather than an expansion in supply — in other words, a “decline in aggregate demand.” The collapse in commodity demand was caused by the collapse of the economy as a whole, again with money assumed to be of roughly stable value.

I don’t want to rehash all the issues we talked about last year, which are also in Gold: the Final Standard. Do your homework. But, the purpose of this little summary is to identify where The Midas Paradox stands in the scheme of things. It is basically the claim that gold’s value rose, by a catastrophic degree.

Now, let me identify what we are trying to determine. We have a significant decline in commodity prices, accompanied by a significant decline in economic activity in general. This might come about either from nonmonetary issues — a “decline in aggregate demand” with a currency of more-or-less stable value, which is roughly the consensus over the decades, I would say even from the Austrian or Monetarist camps that focused more on “credit expansion/credit contraction” than monetary value — or it might come about by a rise in the value of gold, which is Scott Sumner’s tricky new idea, and which has no other precedent in the long history of the gold standard since 1500. There might even be both factors, a possibility we should consider, just as the 1880-1895 decline in commodity prices is often thought of as perhaps involving both factors (for example by Bordo et. al. (2009) “Good Versus Bad Deflation: Lessons from the Gold Standard Era.”) This is a nice cover-your-behind way of looking at things, because we really can’t be certain one way or the other, but since I can’t find any reason for some rise in the value of gold during that time (central bank demand was rather modest, and did not cause any similar effects in the decades that followed), I conclude that it was mostly (entirely) a matter of commodity supply glut.

The notion of a catastrophic rise in gold’s value began to emerge in the 1980s, the “Mundell-Johnson hypothesis.” It was expressed in greatest detail in Clark Johnson’s 1998 book Gold, France and the Great Depression, 1919-1932. We looked at it here:

September 11, 2016: The “Giant Rise in the Value of Gold” Theory of the 1930s

September 18, 2016: The “Giant Rise in the Value of Gold” Theory of the 1930s 2: Never Happened Before

September 25, 2016: The “Giant Rise in the Value of Gold” Theory of the 1930s 3: Supply and Demand

November 6, 2016: Robert Mundell’s Interpretation of the Interwar Period

November 13, 2016: Robert Mundell’s Interpretation of the Interwar Period 2: The “Mundell-Johnson Hypothesis”

Related topics were addressed here:

July 24, 2016: Blame France

July 31, 2016: Blame France 2: Balance Sheet Peeping

August 7, 2016: Blame France 3: Dump a Pile of Argle-Bargle On Their Heads

Clark Johnson revived the ideas of Gustav Cassel (1866-1945), who argued, in the pre-1914 era, that the gradual accumulation of gold bullion by central banks, to serve as a reserve asset, would gradually drive up the value of gold, causing monetary deflation among gold-standard countries. This argument was largely in reaction to the decline in commodity prices 1880-1896. This was still the early days of central banks, however; this analysis did not have the advantage of a century of hindsight as we do today. In a meeting in Genoa in 1922, Cassel asked that central banks avoid aggressive bullion accumulation during the post-WWI world gold standard reconstruction, relying instead on foreign reserve assets.

When the Great Depression began at the end of 1929, and led to falling prices in 1930-1931, Cassel applied his long-held “central bank accumulation” warnings, and saw the decline as potentially a result of a rise in the value of gold due to this accumulation. He didn’t really “predict the Great Depression,” but instead reiterated concerns that he had held for the previous thirty years or so.

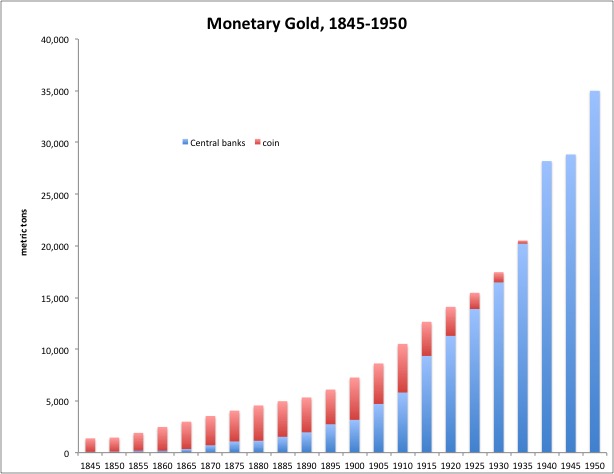

The problems with these theories, as they apply to the Great Depression, is that there is not much evidence that over a hundred years of central bank accumulation of gold (1850-1960) ever consistently raised the value of gold. In the mid-1920s, after seventy years of continuous steady accumulation, commodity prices were unusually high vs. gold. In the 1950s, again after literally a hundred years of accumulation, to levels far higher than the 1890s or 1930s, commodity prices were again high vs. gold. The pace of accumulation was surprisingly steady during all this time.

Central bank holdings of gold increased very smoothly from 1913 to 1940, with nary a ripple around the Great Depression period. This gradual trend continued over a hundred years, with little evidence that it caused any problems. Just look: do you see any reason here why a decade of economic success, during the 1920s, would suddenly turn to disaster? Nothing, right? That’s why these “blame central bank gold buying” theories were NOT popular for the half-century following the Great Depression. It was only — arguably — in the 1980s, when people’s understanding of gold standard systems had deteriorated so far, when people who had actually lived with gold standard systems in the 1920s were all dead, when people could say any stupid thing and other people would believe them, knowing no better — that these ideas became more popular.

With the hindsight of history, I think we can see that Cassel’s concerns were unfounded.

Johnson hinted and implied that there was some kind of great disgorgement of gold by central banks during WWI, and some kind of big repurchase in the 1920s as gold standard systems were reinstituted. This did not happen. Consequently, Johnson claimed that the rising-gold-value-related “deflation” of the Great Depression was caused by something that happened around the 1920-1927 period.

In any case, Cassel’s “gradual accumulation of bullion” idea seemed to fit the gradual decline in commodity prices 1880-1895, but it did not fit very well with the far more sudden drop in 1930-1933, accompanied by economic implosion. This led Sumner to invent some new views regarding “gold demand,” as we will see soon, which are more short-term in nature. Breaking with the Johnson/Cassel framework, Sumner did not see any particular monetary issues before 1929.

Sumner said that the basic ideas of The Midas Paradox date mostly from the late 1980s and 1990s, which is right in line with the intellectual fashions of the time. There was a burst of Great Depression-related research around that time among academics, which seems to have cooled off after 2000 or so.

I thought for sure we would be able to actually begin talking about the contents of The Midas Paradox this week, but we have come far enough already without starting any new topics today. If you haven’t had your fill yet, do some background reading on the many previous posts regarding the Interwar Period in 2016 and 2017, and read the relevant chapters in Gold: the Final Standard. Let’s take it up again next week.