The Federal Reserve in the 1920s 4: The Historical Record

December 23, 2012

We’ve been looking at what the Federal Reserve was up to in the 1920s.

December 16, 2012: The Federal Reserve in the 1920s: Balance Sheet and Base Money

November 25, 2012: The Federal Reserve in the 1920s 2: Interest Rates

November 18, 2012: The Federal Reserve in the 1920s

This has been quite productive, not only as an examination of the Federal Reserve itself, but also as an example of how most central banks (and note-issuing commercial banks) worked in the 1900-1914 period. They had a rather complex combination of direct lending, open-market purchases of debt securities, and gold bullion redemption/monetization. I discussed the topic of operating mechanisms earlier this year:

January 29, 2012: Gold Standard Technical Operating Discussions 3: Automaticity Vs. Discretion

January 15, 2012: Gold Standard Technical Operating Discussions 2: More Variations

January 8, 2012: Some Gold Standand Technical Operating Discussions

To understand these rather complicated arrangements, it is best to break it down into a series of simpler processes. In practice, these were all mixed together. It was not necessarily the best way to do things, but rather, grew out of the Bank of England’s history as a currency issuer, “lender of last resort,” central payments clearinghouse, and also profit-making commercial bank, rolled into one institution.

This week, let’s look at some histories of the Federal Reserve, and see if they have anything to add to our understanding. I purposefully looked at the direct data first, and invited you to come to some conclusions based on that data. There is a very bad habit of just relying on the “expert.” Often, the “expert” interpretation is wrong. I would say that it is almost always wrong. If Milton Friedman knew what he was talking about, he wouldn’t have been Monetarist.

We also looked previously at a pretty good history of the time period from a worldwide perspective.

May 13, 2012: The “Gold Exchange Standard”

Although Eichengreen has a very heavy Keynesian bias, nevertheless I think his overall characterization of the world gold standard of the 1920s is basically correct. Currency managers basically operated their gold standard systems in accordance with proper operating principles, and roughly in the fashion it was done pre-1914. However, the time period also had increasing interest in various forms of Mercantilist (Keynesian) “money manipulation” as a means to manage economies. This didn’t affect the actual operation of gold standard systems that much at the time — roughly 1926 to 1931, it was very brief — but it did introduce a political uncertainty. People were nervous that currency managers would be influenced enough by these ideas that they would abandon gold standard principles. This is exactly what did happen, particularly in 1931.

As discussed previously, our interest begins around 1923 and goes until the end of 1929. In 1920-1921 (and a little into 1922), the Fed was engaged in some issues regarding the resumption of the gold standard after considerable monkey business during World War I and soon after.

March 25, 2012: The U.S. Dollar During WWI and the Recession of 1920

Friedman begins his discussion of the 1923-1929 period on roughly page 251 of his Monetary History of the United States, 1867-1960.

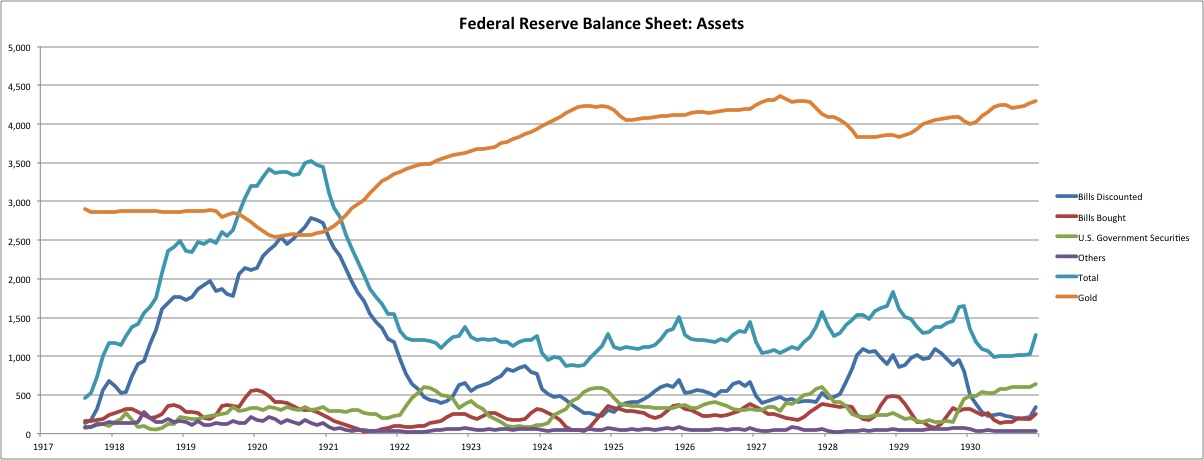

There is a lot of discussion about the “scissors effect,” between direct lending, open market operations, and gold bullion. If one would increase, the others would tend to decrease. This is just the normal operation of a gold standard system. The total amount of base money reflects the demand for base money, at the parity price. If more base money is supplied somehow, these mechanisms would reduce base money by some other means, such that it again reflects demand, which basically means that it is unchanged. If the Fed buys debt in the open market, and pays for this with freshly-created base money, the excess base money would then leave somehow, with either reductions in direct lending or outflows of gold bullion (redemption).

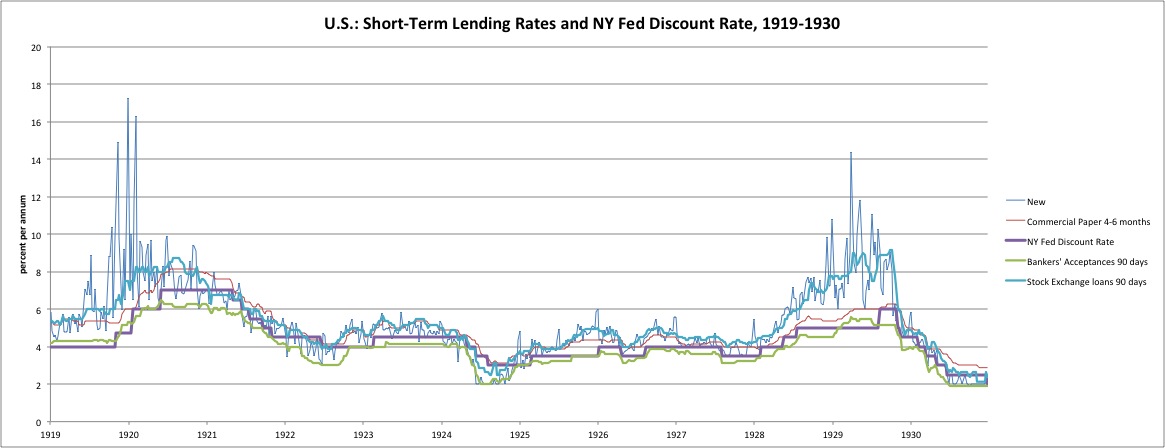

In Friedman, there is a lot of discussion about stock speculation. In the 1927-1929 period, market overnight interest rates rose considerably. This was because the principal borrowers of that time were stock brokerages. They were borrowing for margin lending. There weren’t any regulations on margin in those days, and it was common to use appallingly high leverage of 3x, 5x, or even 10x. This, of course, required a lot of borrowing.

As market interest rates rose, the Fed’s lending rate (discount rate) sank below the market, which meant that more brokers would go to the Fed for money. The discount rate was always supposed to be generally above the market rate, as a “penalty rate” for short-term liquidity needs. However, the Fed apparently hemmed and hawed a bit in discussions on whether to raise the discount rate to an appropriate level. Eventually, they did of course, as you can see. However, they didn’t want to get blamed for a recession due to “tight money.” This is the kind of Mercantilist/Keynesian thinking that was spreading during the time.

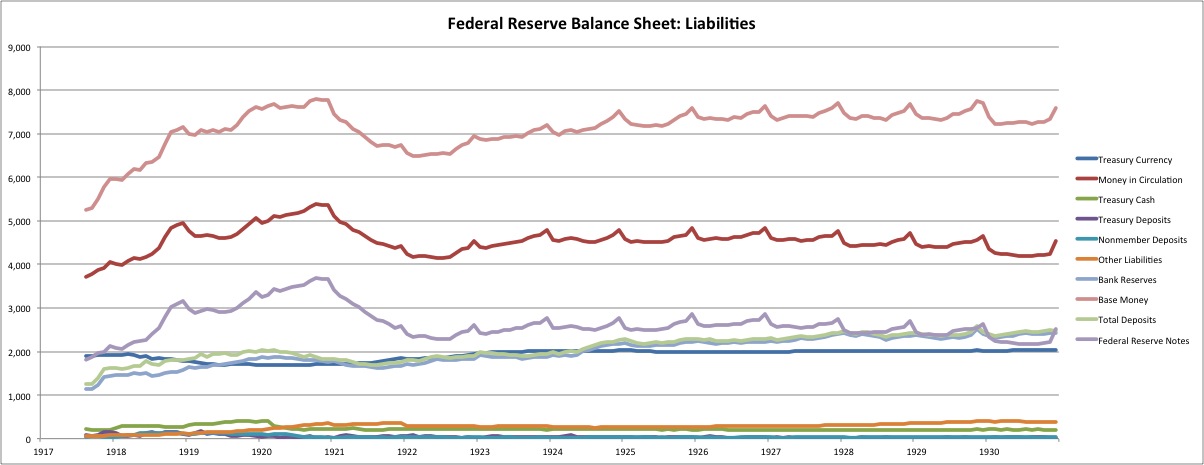

This expansion in discount-window lending had no real effect on base money, because it was immediately counteracted with gold redemption and also reductions in other debt held. Base money was very stable at the time.

On page 282, Friedman accuses the Fed of “sterilizing” gold inflows and outflows. This is basically incorrect. The gold redemptions were offsetting expansions in “Fed credit.” In other words, it was not sterilized at all — the effect of the gold redemption was to decrease the monetary base, cancelling the unneeded expansion from credit activities. It was the fact that gold flows were not sterilized that produced the “scissors effect” and the consequence that base money remained largely unchanged (following the smooth curve characteristic of the time). Friedman seems a little confused here, but it is a minor matter overall. As you can see, none of these wiggles and waggles were very large in size, certainly not compared to what was going on in the 1919-1922 period.

Friedman accuses the Fed of “exerting a steady deflationary pressure on the economy” as a result of its somewhat less-lenient policy in 1929 (less discount lending at below-market rates). There was no such deflationary pressure, because the dollar did not vary from its gold parity. If the dollar rose above its parity value — indicating demand for base money that was not being fulfulled — then one of two things would happen: gold would flow into the Fed in return for new base money (monetization), or the Fed would observe that the dollar’s value was above its parity on the bullion or foreign exchange markets, and react with open-market purchases of bonds, which would also increase the monetary base. These mechanisms certainly did work, as you can see from the steady bullion inflows in 1922-1924 and consequent rise in the monetary base. In fact, this is exactly what was happening in 1928-1930, as shown by the increase in gold bullion, which counteracted the decline in Fed Credit from its unnaturally-inflated 1928 level. Base money was basically stable.

In other words, if the reduction in Fed Credit was not counteracted by gold inflows, then the monetary base would have indeed fallen by a significant amount. This would have led to a rise in the dollar’s exchange value vs. gold and other gold-linked currencies — precisely what happened in 1919-1922, when raising the dollar’s value from its postwar devalued state back to the prewar parity was the Fed’s goal. It would have been “deflationary.” However, the gold inflows (monetization) cancelled that out, maintaining base money at a stable level and also maintaining the dollar’s value at a stable level.

Friedman bases some of his following conclusions on the supposed “sterilization” of gold in the 1920s and afterwards. As noted, this was basically incorrect. Like I said, if Friedman understood this stuff, he wouldn’t have been a Monetarist.

Now, let’s look at Allan Meltzer’s A History of the Federal Reserve, Volume 1: 1913-1951.

Meltzer’s discussion is, I would say, rather more confused that Friedman’s. More conceptual error. He also talks a lot about “sterilization” again. I found nothing of particular new interest in Meltzer, although he does have quite a bit of worthwhile detail about some of the discussions of the time regarding the 1928 lending surge.

Richard Timberlake’s Monetary Policy in the United States, an Intellectual and Institutional History, is one of the best volumes of monetary history I know of. Timberlake is a classical economist, and sees things through that framework. This is helpful, because it was the framework that the currency managers themselves used, until 1971. Thus, there is a lot less misinterpretation of what was happening during those years.

As his book covers a long time period, Timberlake’s discussion of the Fed in the 1920s is brief. He notes that the Fed, in practice, was continually active in the lending market (discount lending) and also continually active in open-market sales and purchases of debt securities, on top of the gold redemption/monetization factor. This was rather contrary to the ideas that surrounded the Fed’s charter, and the role it was initially intended to take (his discussion of that topic is exemplary). However, as I have noted, what the Fed was doing was not really anything new; it was the way the Bank of England and other central banks around the world operated. It is perfectly functional, although arguably over-complicated, way of operating a gold-standard system, as is evidenced by the fact that the Bank of England did so, with these techniques, for 217 years (1697-1914). It was also a consequences of the Fed’s involvement in money-printing during World War I, which made the Federal Reserve Note much more dominant in the currency system that it would have otherwise been, thus giving the Fed a larger role.

All in all, I find nothing in these three books (four if you count Eichengreen) that contradicts the simple conclusions that we arrived at from just looking at the data. Indeed, I wouldn’t say they add much either, as the discussions they describe are basically what one would expect to see in the conditions represented by our market and balance sheet information. (It’s nice to confirm that though.) There is quite a bit of error in the books (excepting Timberlake), which we can identify because we first looked at the real data.

I hope this will serve as an example of how to look at some of these historical issues. What you DON’T DO is just read some books, and try to come to some average of received opinion. Most of the opinion is flawed, and this process will inevitably produce just another flawed opinion. You will have no basis with which to identify the errors, which are plentiful. It would be nice if someone wrote a decent history of these time periods, without the kind of misunderstanding and empty accusations that characterizes Friedman and Meltzer. It would make a nice foundation for an academic career. There are so many great opportunities such as these, which you can learn about just by reading my website for free. I can’t do all this stuff myself, so there is plenty for others to do. It’s not really that difficult. The standard of economic discussion during the 20th century (and early 21st century) is so low, you can exceed it with hardly any effort at all.