(This item originally appeared at Forbes.com on June 10, 2026.)

Remember the Federal Reserve’s “2% Inflation Target”? It has been 63 consecutive months since that target has been met. In May, the official Consumer Price Index (which has been continually modified since the 1980s to make it look better) was 4.2% higher than a year earlier.

But even if the Federal Reserve was able (har!) to meet this target, it smells suspiciously like a plan to gradually devalue the currency over time. This makes political sense – a cheaper currency benefits debtors, at least for as long as interest rates don’t reflect expectations of continual currency debasement. Since the government is the biggest debtor, and since a lot of voters are also big debtors, there is a kind of constant political wind toward cheapening the currency.

This CPI target is somewhat informal. It has been mentioned many times, but does not form an institutionalized part of the Federal Reserve’s procedure. Other than this element, which added a sense of legitimacy before it became an embarrassment, the Federal Reserve pretty much just makes it up as they go along.

This gives rise to a catalog of various “rules-based systems,” promoted by various organizations (notably the Cato Institute) who think they can do better. But can they? I don’t think so.

What is the purpose of floating fiat currencies? Why do they exist? As I describe in my eight-part YouTube series on monetary topics, the basic motivation is macroeconomic manipulation, often devolving into government finance. Borrowing the terminology of Federal Reserve Bank of Richmond economist Thomas Humphrey, I called this the “Mercantilist” approach to money, or the Soft Money Paradigm. There is a lot of similarity with today’s proposals (including those of the Cato Institute) and the Mercantilist economists of the eighteenth century. They will deny this, of course, because it is embarrassing. But, the similarity is there, as Humphrey describes.

Much of what passes for novelty and originality in monetary theory and policy is ancient teaching dressed up in modern guises. To be sure, the increasing application of mathematical modeling has given these concepts greater rigor and precision. Likewise, better data and more powerful empirical techniques have improved our statistical estimates of the relevant quantitative magnitudes. Still, the basic ideas themselves often remain much the same.

Basically, the Mercantilists of the 18th century, and those of today, mostly labeled as some flavor of Monetarist or Keynesian, make macroeconomic manipulation their first and highest goal. This is accomplished with some kind of manipulable floating fiat currency, probably accompanied by some kind of intentional manipulation of money supply and interest rates. Today, this might take the form of “nominal GDP targeting,” which itself contains elements of “inflation” and “real economic growth,” which is basically the same as today’s Federal Reserve “dual mandate.”

Against this is the Classical Paradigm, which aims for a “neutral” currency that is basically an unchanging constant of commerce, a fixed “measuring rod” or “numeraire.” In practical terms, this means a currency of fixed value. There is a precise definition of the value of the currency.

More than half of all countries in the world today have some form of a Classical Fixed Value System. It is very common, because it works.

Mostly, these currencies are formally fixed to either the dollar or the euro, which are themselves floating currencies. But, for these countries, the result has been far more stability and reliability than having their own independently-managed floating fiat currency. The countries of Europe had so little success with independent floating fiat currencies that they were completely abandoned in 1999, in favor of a unified euro based on the German mark. Other countries’ experiences have been generally worse than that, with outright hyperinflation in dozens of countries since 1950.

The United States, and also all the other major countries in the world, also had a Fixed Value System – not a system of macroeconomic manipulation with floating currencies. The value of their currencies was fixed to gold. In the United States, the value of the dollar was fixed at 1505 milligrams of gold (notated as “$20.67/ounce”) until 1933, and then at 889mg (“$35/oz.”) after 1933, until 1971. This is no different, in principle, than the recent currency board between the Bulgarian lev and the euro, at 0.51129 euros per lev.

Whenever you hear some kind of proposal to replace the Federal Reserve’s recent seat-of-the-pants failure, whether a “rules based system” or whatever kind of system, just ask yourself: What Is The Value of the Currency?

Probably, they have no answer. It is a floating fiat currency. It has no fixed value.

Floating fiat currencies go up and down unpredictably in the short term. Who the heck knows. If you think you know what the value will be in a few weeks, you should become a currency trader.

But, we know what the value of these floating fiat currencies will do over a longer period of time. Their values will decline. A lot.

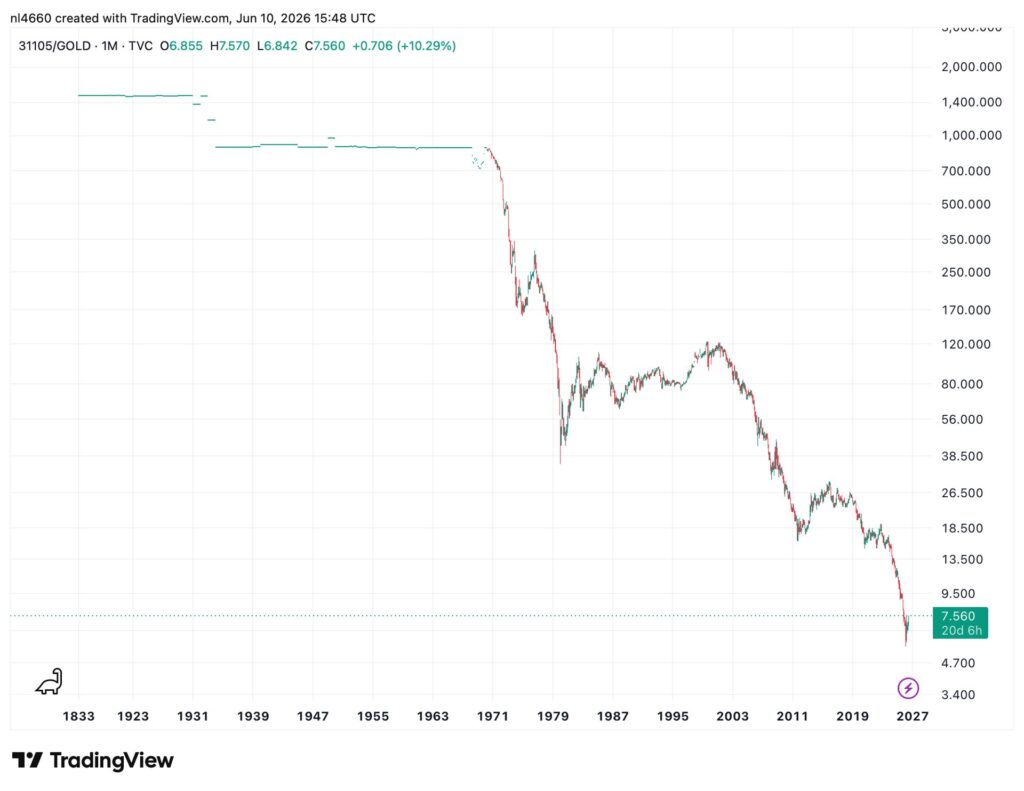

The dollar that was once worth 889 milligrams of gold, when your grandfather was in college in the 1960s, is today worth about 7 milligrams. Yeah, that’s a big decline.

In the time since then and now, the Federal Reserve, and all other major central banks, have sworn up and down that they were “fighting inflation,” as if it was something external that they had to fight, instead of merely the results of their own mismanagement. For the most part, the people at the Federal Reserve have been genuinely of very high caliber – the Best and the Brightest. But, they failed, just as all of the successors will fail, because failure is certain. Floating fiat currencies always decline in value over time.

Look at the chart. Think about all the verbiage from all the Fed governors since 1960. Look at the chart again. Now guess what is going to happen if we have the same kind of Fed governors spouting the same kind of verbiage for another 30 years.

The only real alternative to this charade is some kind of Fixed Value system – and the best Fixed Value system, in all of human history and continuing today, is a Fixed Value with Gold. Of course this is not perfect (such a thing does not exist in human affairs), but we know, from centuries of experience, that it is close enough that there is really not much to complain about.

All of the other proposals for the Federal Reserve to do this, that and the other, within a Mercantilist framework of floating fiat currencies – you are going to hear a lot of them soon — are just different flavors of failure.