Today, we will re-summarize our work on the Interwar Period.

October 2, 2016: The Interwar Period (contains many links)

October 6, 2016: Team Gold Needs To Get Over the Great Depression

October 16, 2016: Nonmonetary Perspectives on the Great Depression

October 23, 2016: Nonmonetary Perspectives on the Great Depression 2: Steindl, Schwartz and Eichengreen

October 30, 2016: Nonmonetary Perspectives on the Great Depression 3: Nonmonetary Causes

November 6, 2016: Robert Mundell’s Interpretation of the Interwar Period

November 13, 2016: Robert Mundell’s Interpretation of the Interwar Period 2: the “Mundell-Johnson Hypothesis”

July 10, 2016: The Tyranny of Prices, Interest and Money

November 27, 2016: The Tyranny of Prices, Interest and Money 2: The Old Historicism

February 19, 2017: “Prices” And Value

February 23, 2017: James Grant Explains How A Crash in 1921 “Cured Itself” — With The Help of Good Policy

May 14, 2017: More on the Depression of 1921

May 21, 2017: The Fed’s 1932 Bond-Buying Experiment

May 29, 2017: The Fed’s 1932 Bond-Buying Experiment 2: Automatic Adjustments Via Gold Conversion

June 18, 2017: The “Gold Sterilization” of 1937

June 26, 2017: The “Gold Sterilization” of 1937 2: Fumbling and Bumbling

July 9, 2017: The “Gold Sterilization” of 1937 3: The View From 2011

July 23, 2017: The Midas Paradox (2015), by Scott Sumner

July 31, 2017: The Midas Paradox #2: Blame Gold

August 3, 2017: The Midas Paradox #3: It’s So Because I Say It Is

August 11, 2017: The Midas Paradox #4: Much Ado About Nothing

August 18, 2017: The Midas Paradox #5: It’s Getting Uncomfortable In The Prices, Interest, Money Box

There are a lot of wildly different “interpretations” of the Interwar Period — these “interpretations” for the most part untroubled by the lack of any theoretical or factual support. From my perspective, there was not a lot to “debate,” because most everything crumbled to dust as soon as you began the most rudimentary investigation. I don’t claim to have the full picture of what was going on in those days. I haven’t really researched the Great Depression period in the kind of detail that I would like to. Nobody else seems to have done this either. But, I think we can pretty much dismiss the idea that there was some major monetary component, at least until the devaluations of 1931. I think there was a substantial credit component, and that this is deserving of much more study than it has received. For now, I am happy to assume that the credit contraction (shrinking bank lending) was more of an “effect” than a “cause,” but it is a topic for further investigation.

In the end, I came to the same conclusion as most people of the time, and the most common consensus for thirty years afterwards, until the 1960s. Even today, the standard Keynesian model, which does not recognize a “monetary cause” even as it recommended a monetary response, remains a major “interpretation.”

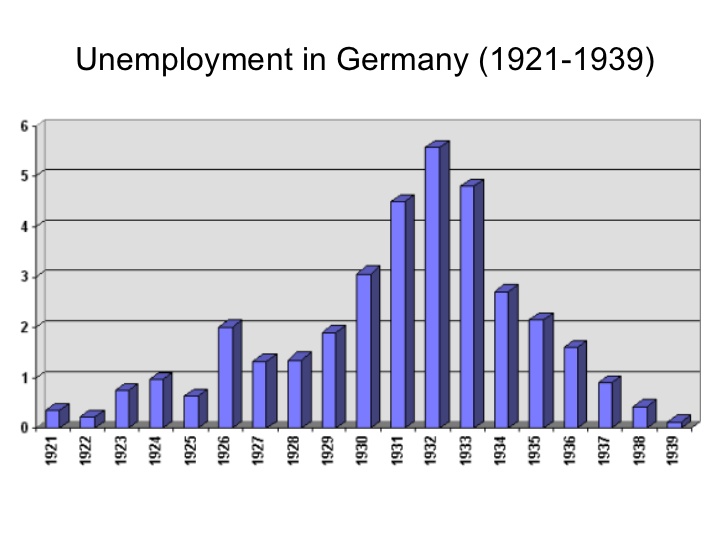

It’s worth noting that one of the most successful economies after 1933 was the one that didn’t devalue — Germany.

This is in millions of people, not percent.

Here’s the U.S.:

I have a feeling we aren’t done with the Interwar Period. But the main importance is not really what happened eighty years ago, but how it affects the understanding of economics today. I wanted to take some time — a lot of time, it turns out — to clear out this basement and drag all the old furniture onto the lawn. Quite a lot of contemporary economic thinking is based on these “interpretations.” I think some hard sunlight will help kill the mold and fungus that has built up over the decades.